-

CFA三级

包含CFA三级传统在线课程相关提问答疑;

真题FIXED INCOME 2016Q1 D问, Trade1:我可以写callable bond的duration小。buy non-callbale,sell callable 可以increase duration吗? 我没提convexity可以吗

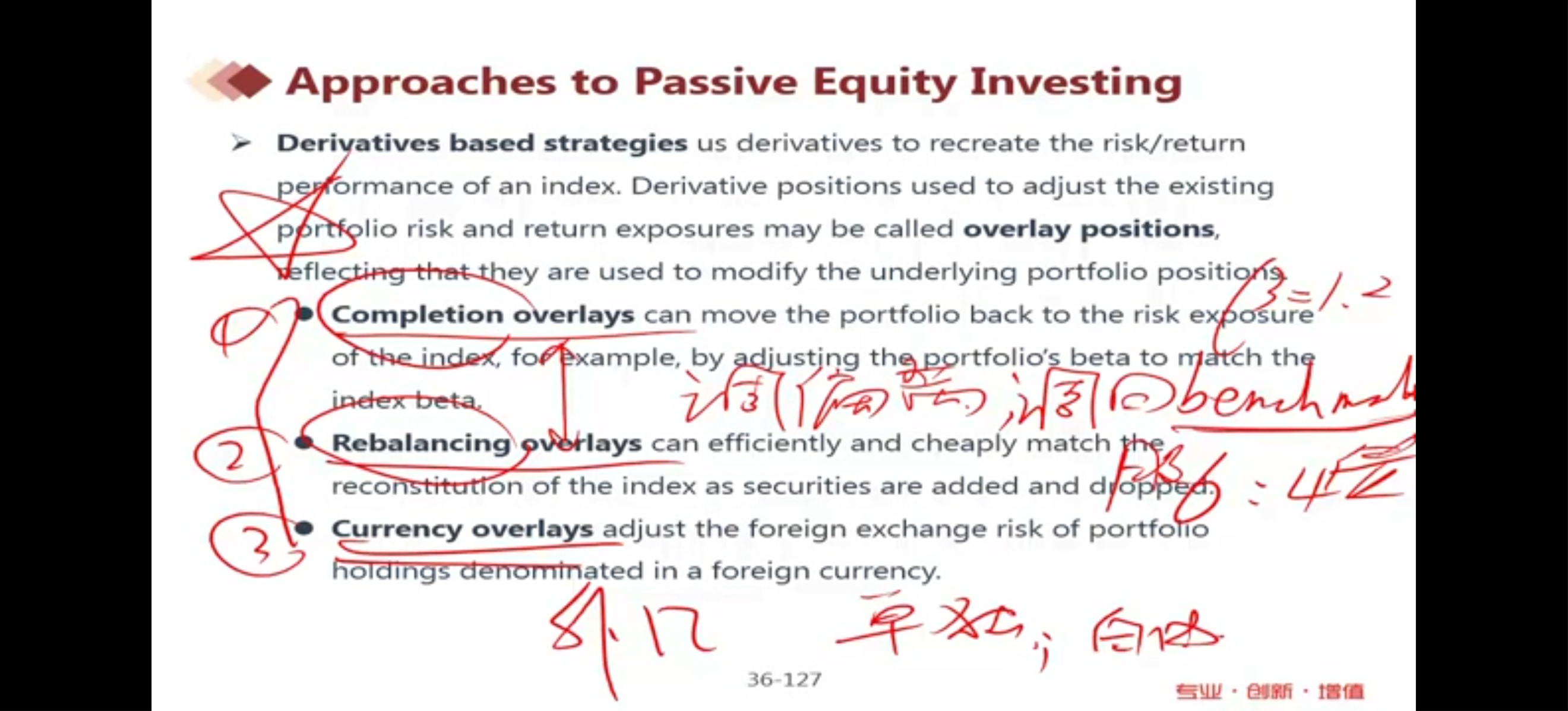

已回答老师,equity以下这两点我很混淆:对于full replication来说,a large number of constituents会增大index的tracking error. 但是对于active share来说,the portfolio with the fewer securities and therefore higher degree of concentration in positions will have a higher level of Active Share,同时也会增大active risk。我觉得这两点很矛盾。 Full replication :An index that contains a large number of constituents will tend to create higher tracking error than one with fewer constituents. The manager will naturally first purchase the largest, most liquid, lowest cost stocks. But as more stocks are added and the portfolio approaches full replication, the added stocks will be less liquid, increasing the effect of transaction costs on tracking error. 1) Comparison of active share If two portfolios with the same benchmark invest only in benchmark securities, the portfolio with the fewer securities and therefore higher degree of concentration in positions will have a higher level of Active Share.

已回答老师,我之前问过一个问题,2016 q2笔答题这道题:all else holding equal 就convexity来说,fixed rate bond的convexity和floating rate bond的convexity哪一个更大?回答是.固定利率债券的convexity更大。第一,我想追问一下为什么?第二是,我之前在基础课或是讲义上(具体不记得了)记得上课讲过floating rate bond的convexity是大于fixed rate bond的convexity的,所以现在很混淆,想澄清一下。

已回答

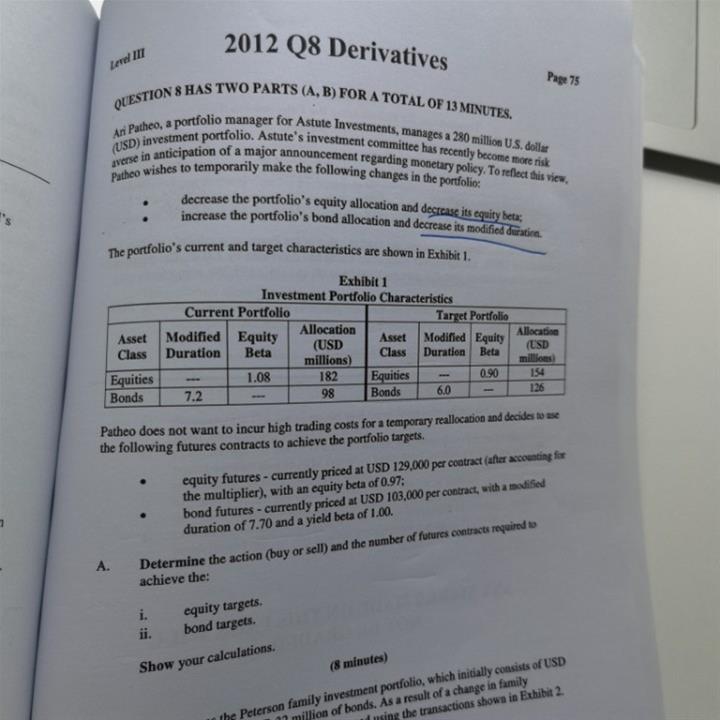

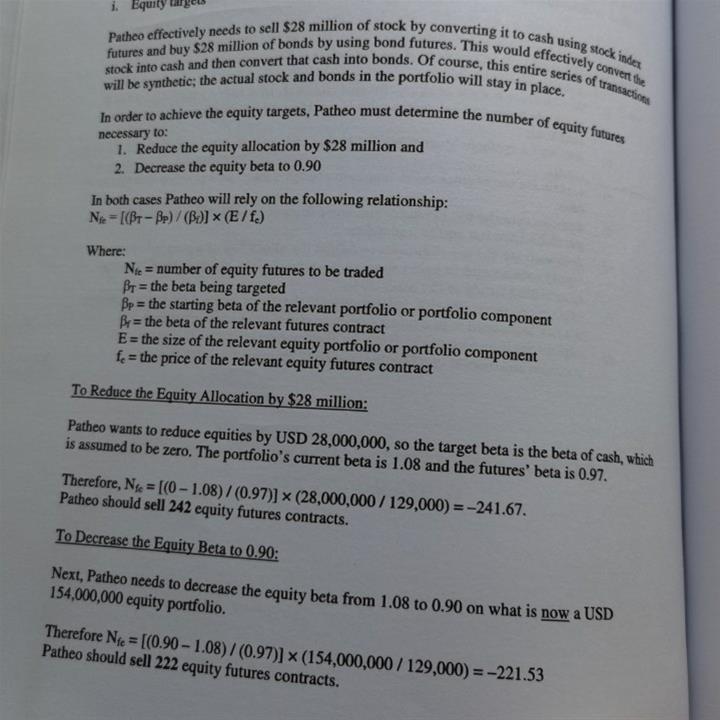

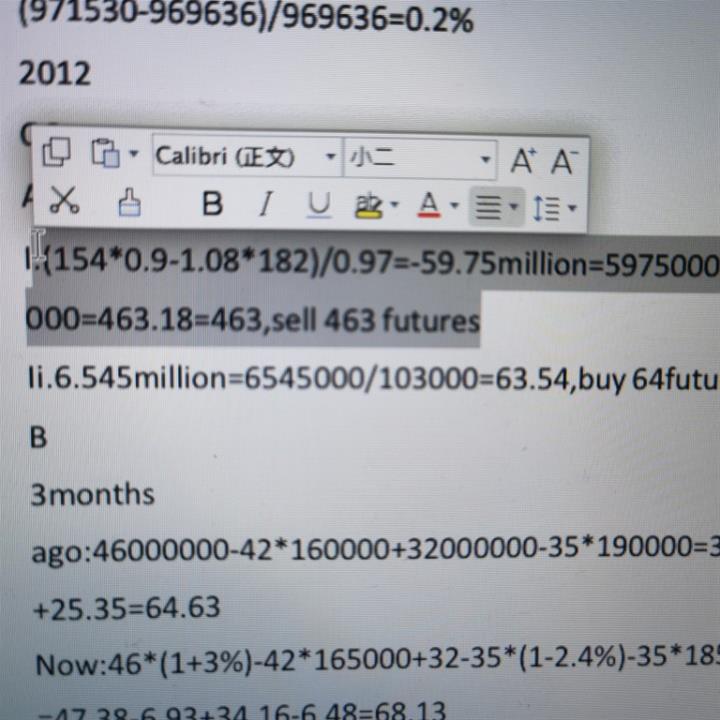

2012年真题的a'问,为什么要将28million拆出来计算,分别调整贝塔。如图三我的计算(.当前组合182乘以贝塔,加上期权乘以期权贝塔,等于目标组合价值154乘以目标组合的贝塔),可以合并为一步进行整体的计算吗?貌似也能算出正确答案

精品问答

- 想具体理解下打星号这个结论的推导过程 为什么收益率分布广了 cost低 为什么样本小 cost低 样本小不应该测不准吗?

- liability relatibe asset allocation这三种方式的区别是什么呀 怎么区分

- 第5题,从经济学公式X-M=(S-I)+(T-G)来看,如果经常账户赤字增加,不是意味着该国投资大于储蓄,或政府支出大于税收么,那么整体环境应该是好的,应该有利于资本的流入吧?为什么答案是反过来去赤字减少或盈余的国家呢?

- 这里第二题的意思是三种方法都适用吗?没太理解,能否在讲解下

- 到底该怎么判断一类和二类错误?做的题目解答标准不一致啊,我看到另一道题的版本是 - 一类错误是做了错的事,二类是没做对的事。现在这一题,对于不合格的经理不采取行动,不就是二类错误 - 没做对的事吗?

- 关于什么时候用IRR 、MOIC

- 1.这里右侧支付端这段,party A角度他有market value risk时谁有?上下部分矛盾了啊.2.左侧的图和配文是什么意思?原本是什么?又变成什么?3.注意里面:fixed端有

- 这两个的逻辑都很奇怪 sponsor薪资和业绩挂钩的话他会更用心选基金经理那么一类和二类错误都应该下降吧 monitor这个词是监控的意思 我觉得你很难监控一个没跟你签雇佣合同的基金经理的表现