-

CFA二级

包含CFA二级传统在线课程、通关课程及试题相关提问答疑;

纪老师衍生讲义136页例题,第一个问题,用call option 去构造动态平衡组合在现实中如何实现,卖出了call option 得到了期权费,之后的价格收益就和组合无关了,只有义务,在价格下降中承担风险

老师您好,在note中有一段描述loss reserve的,原文是“downward revisions indicate that the company was conservative in estimating their losses... Upward revisions indicate aggressive profit booking...“ 我自己从loss and loss adjustment expense ratio公式中的理解和这句话刚好相反,我认为loss reserves downward revisions是下调loss reserves从而降低了ratio,使得收益情况看上去更优,这才是一个更激进的做法。 请老师指点。谢谢!

已回答精品问答

- 倒数第二题,老师讲到,分析师预测的spot rate2年小于forward curve, 因此资产价格应该是被低估。但是在串讲课的时候,老师讲过5.1知识点,如图,如果吧spot rate2年带入讲义的S2,长期利率,forward curve带入f(1,1),那么当边际量f(1,1)小于平均量S2时,平均量应该下降,资产价格应该上升,为高估丫

- Q6,为啥要少抽失败的,少抽不就不能真实反应情况了吗?

- BG检验就是T检验吗?如果理解错误的话 T检验是什么?

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

- Growth due to capital deepening 是αΔK/K还是ΔK/K

- 这题为什么是选C?

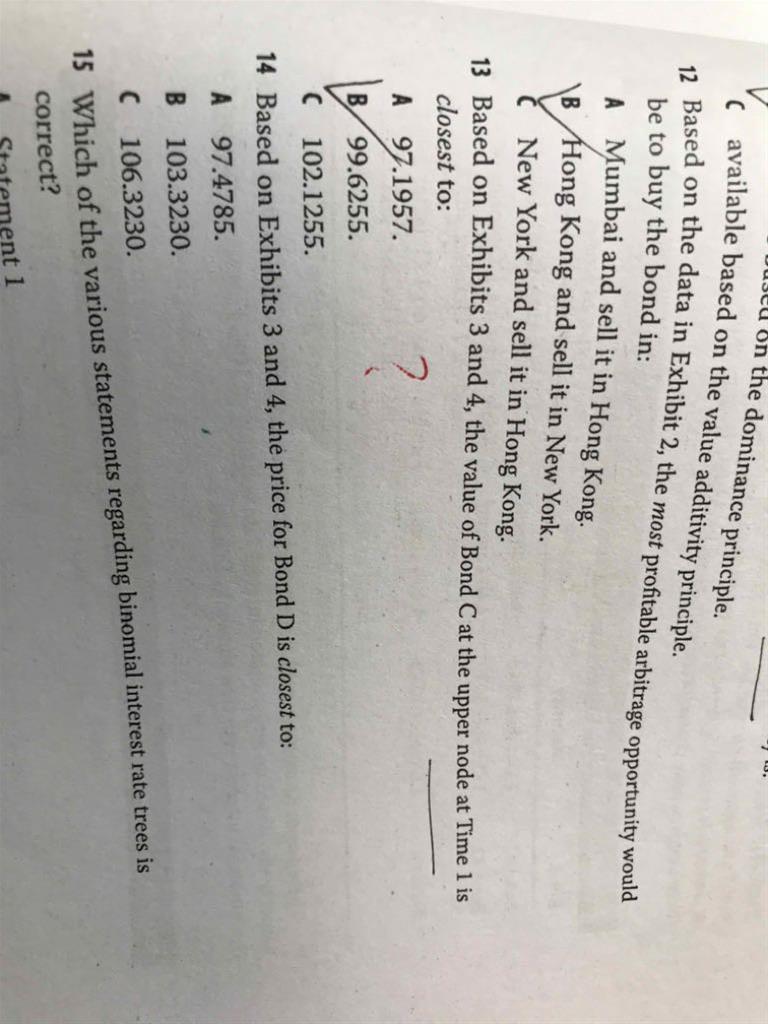

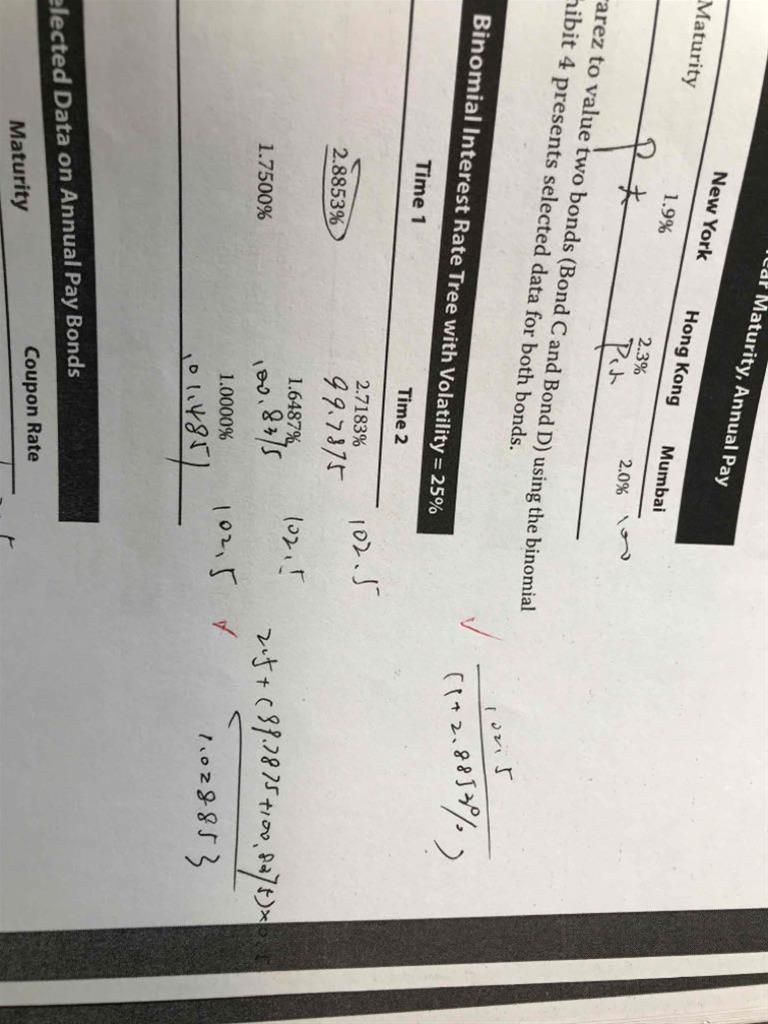

- 请老师讲解一下这个题目

- 老师,第二题可以在解释一下原理吗?