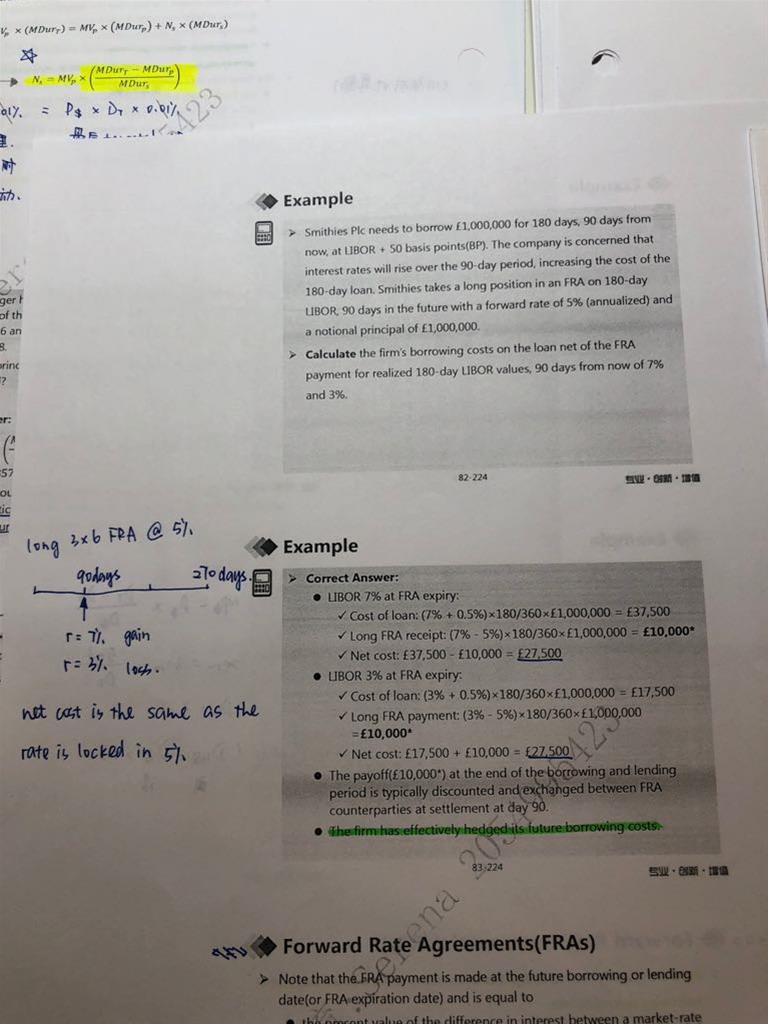

-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

你好,reading23课后第9题的C选项,他建议的策略就是momentum,虽然是factor based,但是最终也是需要去买相应的股票,而不是解答中的因为他是factor base所以错。它是错在overweight近期跌的股票,如果他要是overweight近期经历过涨的股票,那么我认为就是对的,符合momentum的过去涨未来涨的逻辑?

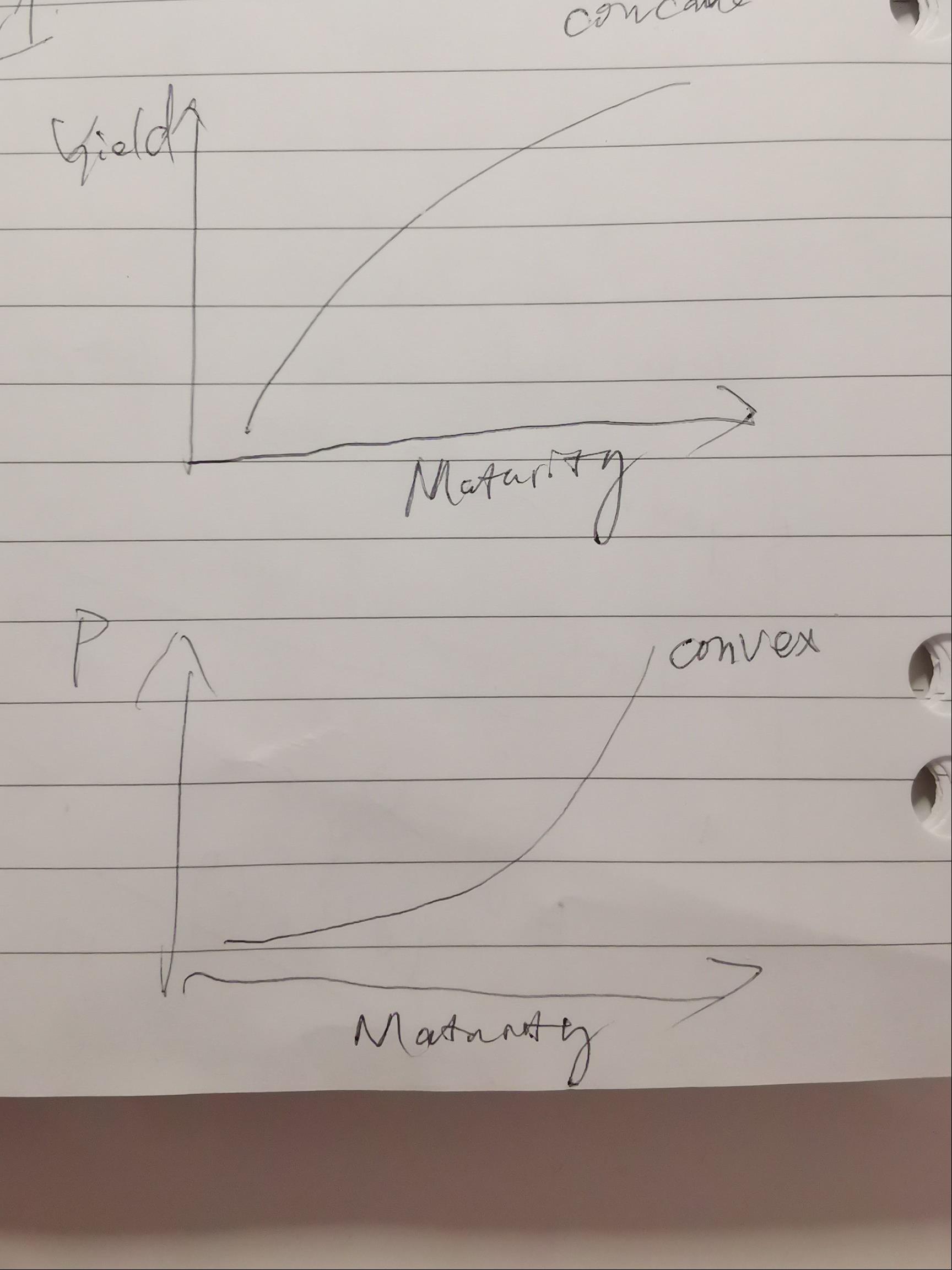

bond的yield的图是concave的吧?bond price的图是convex的?所以long 短端和长端的bond 也就是long他们的price 就是long barbell short bullet 增加convexity 这句话对吗?

百题Case 2第六题 题干中提及global real estate values are showing signs of overvaluation in some markets.那么就应该要减少real estate头寸,答案B中有reduce real estate是对的,为什么least likely be implemented ?

已回答

精品问答

- Q6,为啥要少抽失败的,少抽不就不能真实反应情况了吗?

- BG检验就是T检验吗?如果理解错误的话 T检验是什么?

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- Risk Budget and risk parity 第二道思考题,里面的Variance是不是完全是个冗余信息,给来误导的呀?

- liability relatibe asset allocation这三种方式的区别是什么呀 怎么区分

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- 为什么长期垄断竞争中 D和ATC相切