-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

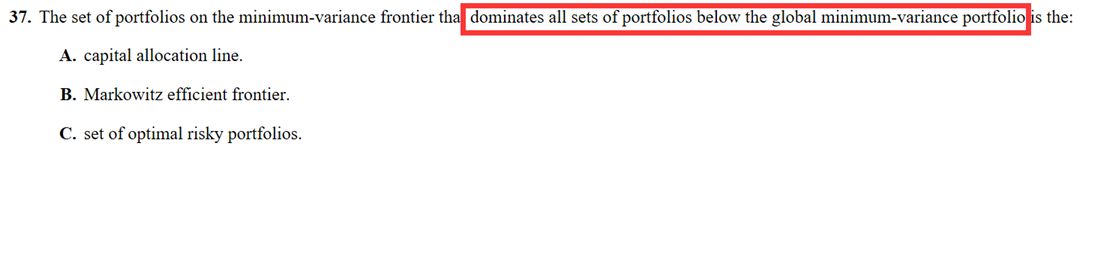

组合,reading41原版书课后题,第37题,截图是题干。这道题关于马科维茨有效前沿的解释中,为什么会有“主导全球最小方差组合下方的组合”这一项?关于EF的定义和解释中,好像没有提到这一条。并且,当我们讨论有效前沿的时候,都是讨论上半条,也就是在全球最小方差组合上方的那些组合。

you expect her to earn two-thirds of her tuition payment in scholarship mont,so youestimate that your payments will be 10000 a year for four years. to estimate whether you have set aside enough money,you ignore possible inflation in tuition payments and assume that you can earn 8 percent annually on your investments,how much should you set aside now to cover these payments

已回答you are considering investing in two different instruments.the first instrument will pay nothing for three years,but then it will pay $20000 per year for four years.the second instrument will pay $20000 for three years and #30000 in the fourthyear. all payments are made at year-end .if your required rate of return on these investments in 8 percent annually,what should you be willing to pay for?我的问题是为什么计算时不是折现到零时间点?

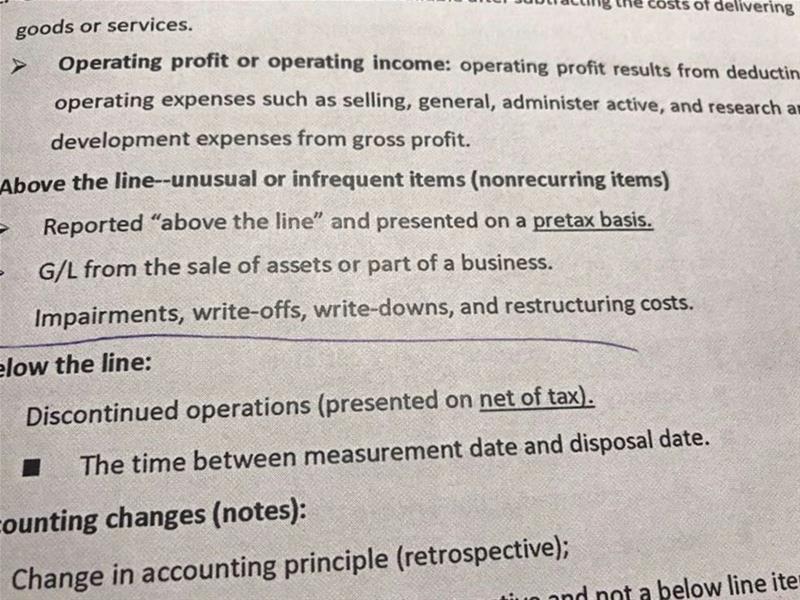

已回答请问 划线的这行,在IFERS下算入unusual items,是在operating profit后去减;在GAAP下,是属于operating items 是在gross profit后去减?是否正确?不对的话 请告知两个法则下 分别归属 谢谢。

精品问答

- Q6,为啥要少抽失败的,少抽不就不能真实反应情况了吗?

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

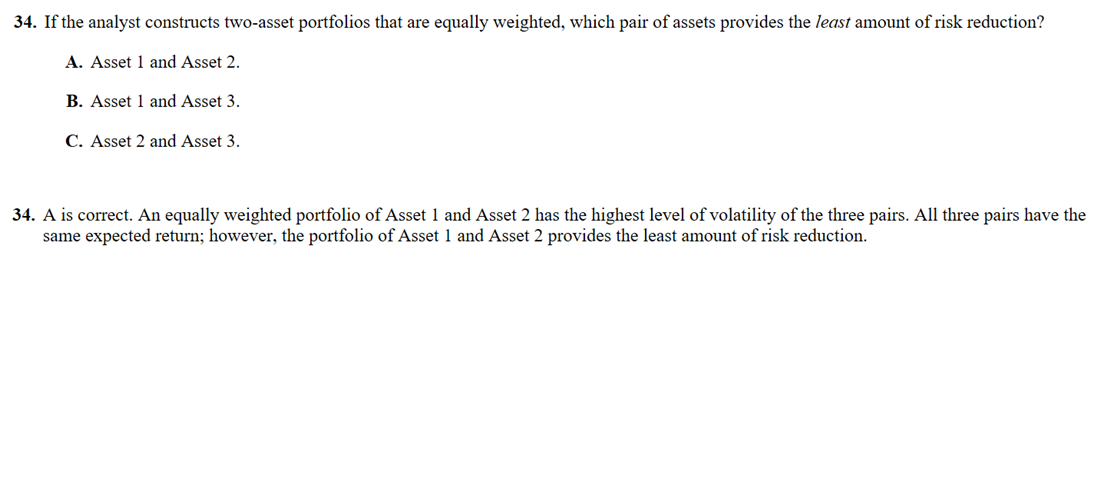

- Risk Budget and risk parity 第二道思考题,里面的Variance是不是完全是个冗余信息,给来误导的呀?

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- Growth due to capital deepening 是αΔK/K还是ΔK/K

- 为什么TC 的切点对应是AVC的最低点?

- 老师,给最新的信息更高权重为什么不是availability bias呢?

- 她对个人笔记本电脑(personal laptop)进行了完整备份(full backup),并确保备份前已删除所有公司文件(all company files removed)。 目的:确保新备份中不包含任何前公司数据,避免合规风险。 遗留问题: 硬盘上的旧备份(previous backups)仍包含公司文件。 她不想因删除旧备份而丢失个人文件的备份历史(backup history for personal files)。 针对上述分析我有个疑惑,这个人不是已经在自己笔记本上备份了drive上的个人信息吗,怎么又Not wanting to lose the backup history for her personal files呢?他不是已经把自己的私人信息备份了吗!?