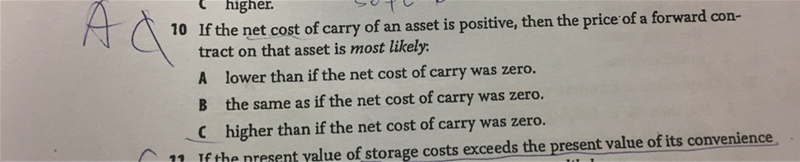

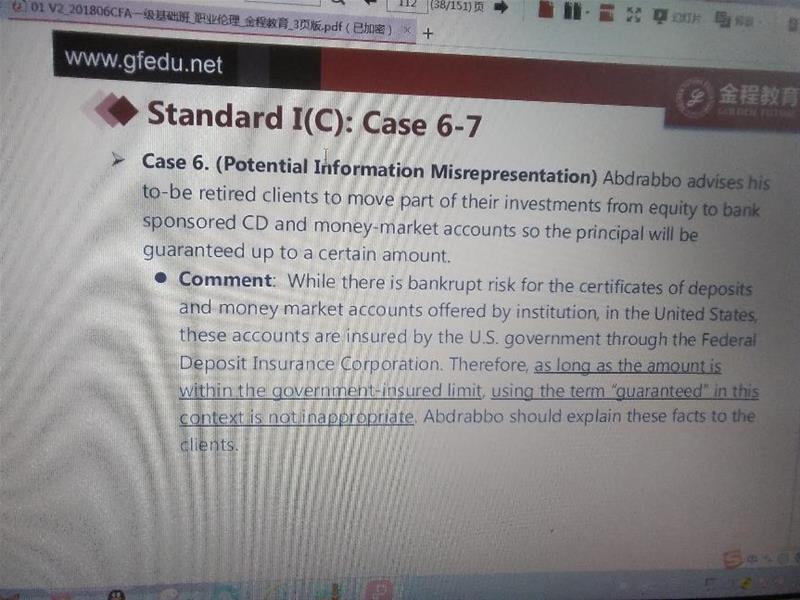

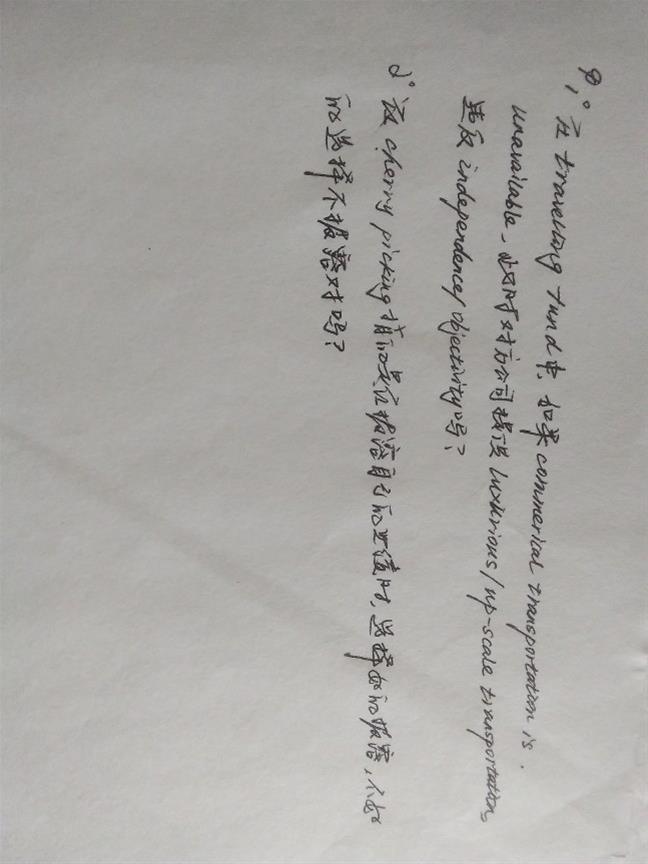

-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

老师,课上例题如果是求HPR的话over three year 就不用再开根号了因为一段时间的HPR这不需要年化,这里求的over four year的 几何平均值,但也是这四年的一个时间段的,这里按照答案要年化。这个怎么区分什么时候需要年华呢?

查看试题 已解决

老师您好! reading24课后题中的第20题,为什么不选portfolio 1 ? 因为steepen,可以选择一个bullet呀? portfolio 1 的1、3、30年均比current portfolio降低,5、10年的均增加,不是一个很好的bullet吗? 谢谢!

This condor is structured so that it benefits from a decline in curvature, where the middle of the yield curve decreases in yield relative to the short and long ends of the yield curve. (Institute 226) Institute, CFA. 2019 CFA Program Curriculum Level III Volume 4. CFA Institute, 5/2018. VitalBook file. 老师您好! reading24课后题第19题中提到的这个condor,答案中提到的the middle of the yield curve decreases in yield relative to the short and long ends of the yield curve,这个变化过程,能否麻烦画两张图给看一下?辛苦啦!非常感谢!

Hirji also proposes the following duration-neutral trades for the French institutional client: Long/short trade on 1-year and 3-year Canadian government bonds Short/long trade on 10-year and long-term Canadian government bonds (Institute 214) Institute, CFA. 2019 CFA Program Curriculum Level III Volume 4. CFA Institute, 5/2018. VitalBook file. 老师您好!reading24课后题中这个condor要求duration-neutral,而不是教材中写的“money duration neutral”,后面的2s的allocation计算是依照money duration neutral计算的,不严谨?

已回答精品问答

- Q6,为啥要少抽失败的,少抽不就不能真实反应情况了吗?

- BG检验就是T检验吗?如果理解错误的话 T检验是什么?

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- Risk Budget and risk parity 第二道思考题,里面的Variance是不是完全是个冗余信息,给来误导的呀?

- liability relatibe asset allocation这三种方式的区别是什么呀 怎么区分

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- 为什么长期垄断竞争中 D和ATC相切