-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

专场人数:0提问数量:0

经济百题Q81 C选项 意思是银行用来可贷款的储备金减少,没有钱可以借出去了,经济有事下行状态,这个时候采取QE,直接将货币注入市场上类似MBS这种,而不是通过银行再放贷给民众,是这个意思吗? A选项,QE不是帮忙解决流动性陷阱问题,而是因为货币政策容易出现流动性陷阱,所以采取QE的货币政策直接解决经济下行问题。 我这么理解AC选项对吗?

已回答

老师您好,关于上午真题Derivative部分2017年第十题(D)小问,答案中提到information ratio can be false positive when returns are below risk free rate, 但standard deviation不是应该一直都是正数么?(Rp-Rb)的standard deviation可以是负的吗? 谢谢!

已回答

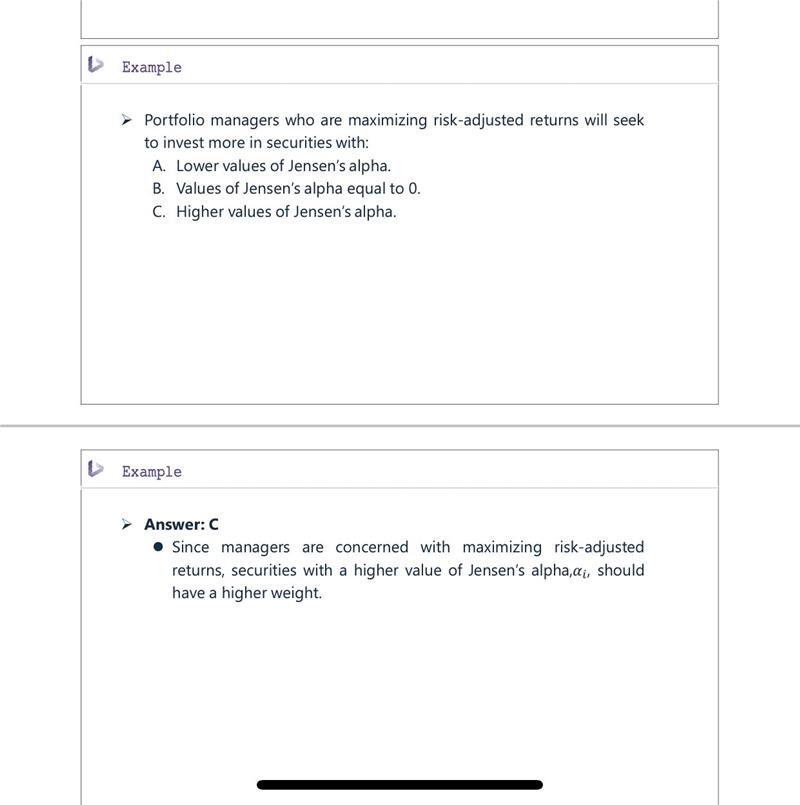

Jensen‘s alpha不是actual portfolio return跟risk-adjusted return之间的差么,那risk-adjusted return要越大的话不应该是alpha越小么

MPS , 等额偿付本金和利息 1.CMOs are created from pools of pass-through securities, 利息和本金有先后顺序 不知我的理解对不? 2.CMOs are securities issued against pass-through securities for which the cash flow have been reallocated to different tranches.这句话如何理解?谢谢!

已回答请问答案解析中A is incorrect because the forward price is set in the pricing of the contract such that the starting contract value is zero, unlike contingent claims, under which parties can select any starting value这句话的意思能解释一下吗,什么是starting contract value?以及为何option中参与方能够选择任何starting value

查看试题 已回答

精品问答

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- Risk Budget and risk parity 第二道思考题,里面的Variance是不是完全是个冗余信息,给来误导的呀?

- liability relatibe asset allocation这三种方式的区别是什么呀 怎么区分

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- 为什么长期垄断竞争中 D和ATC相切

- Growth due to capital deepening 是αΔK/K还是ΔK/K

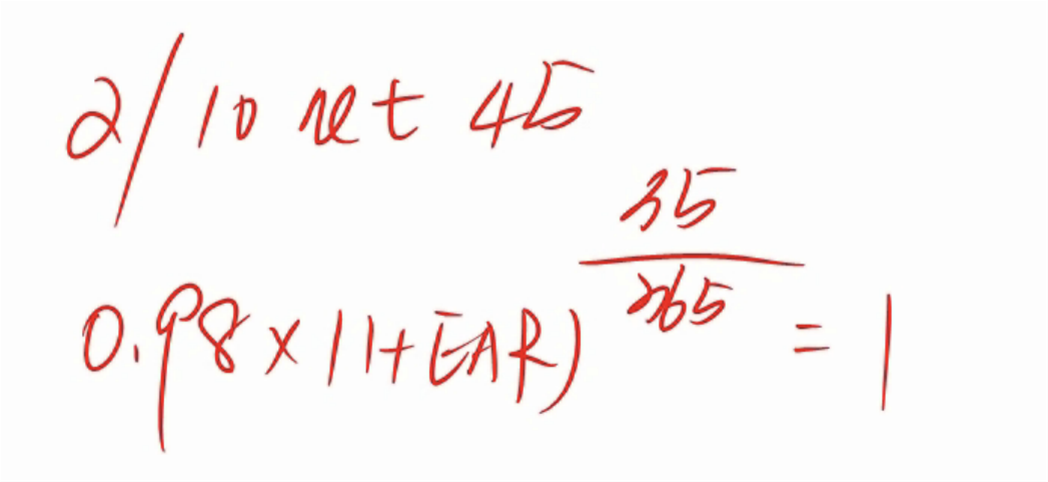

- m上升 EAR为什么上升 以及为什么又不变