-

CFA一级

包含CFA一级传统在线课程、通关课程及试题相关提问答疑;

老师请问,杜邦五分法里面的tax burden 和 interest burden是哪个类型的指标啊?liquidity, solvency,activity 还是profitability?

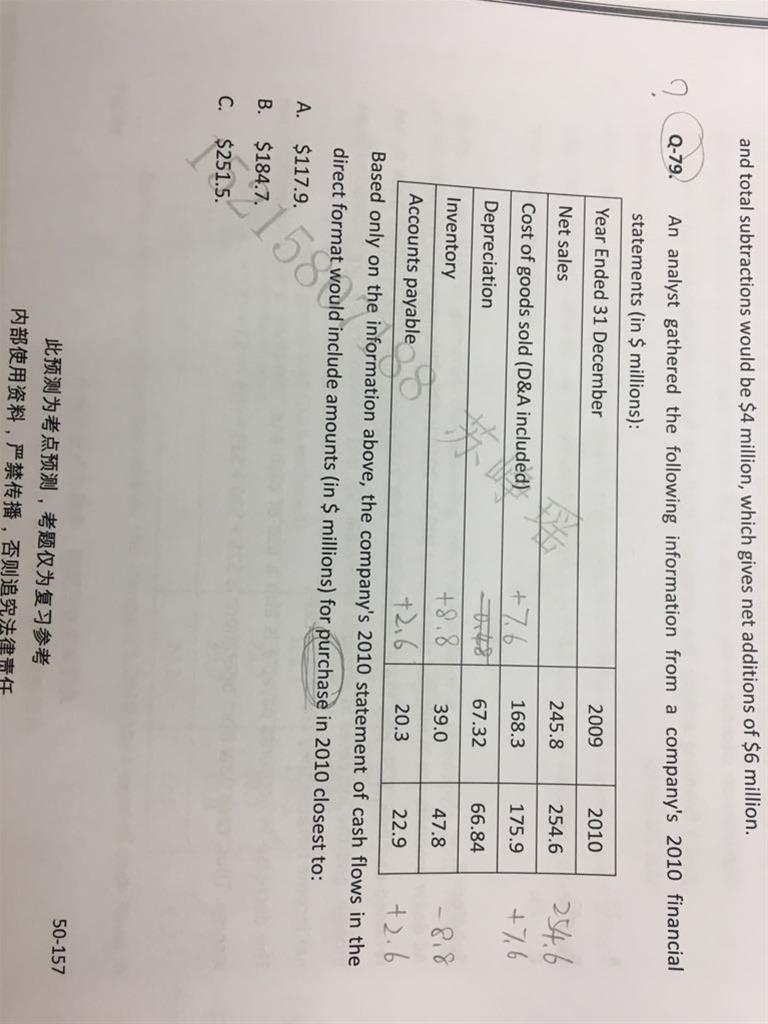

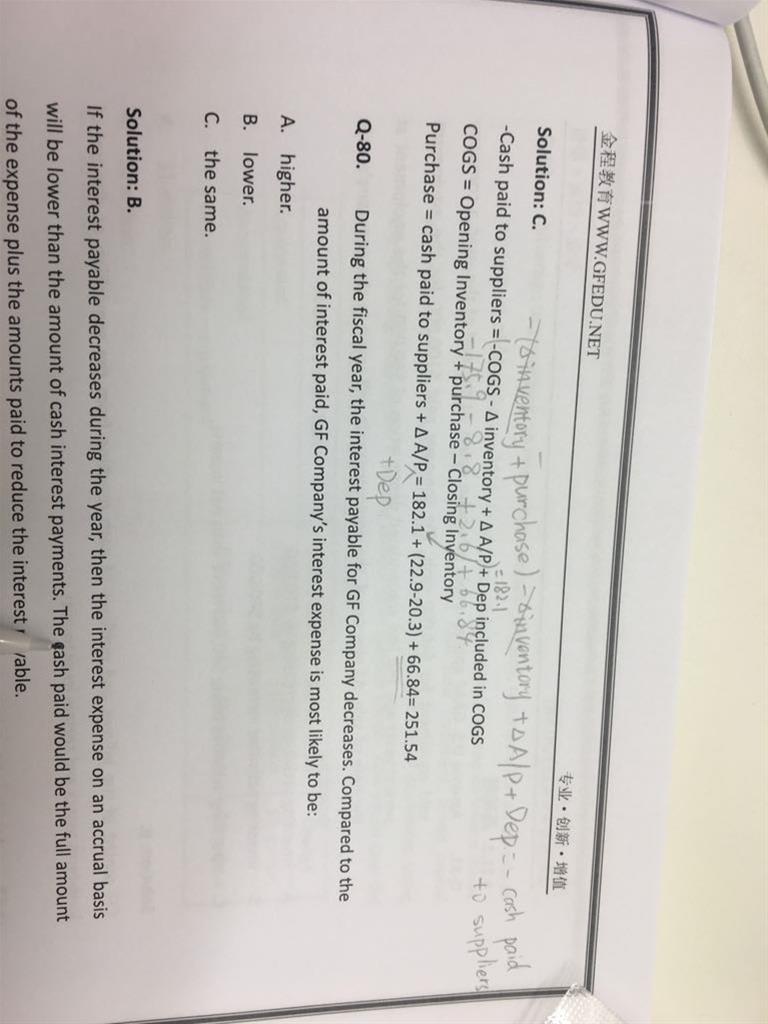

已回答老师、这题的解析有点问题。 图二中、根据第一个公式算出来的cash paid to suppliers不等于182.1,1⃣️式中的值和3⃣️式代入的cash paid to suppliers 差了一个Dep included in COGS66.84. 还有、第三个公式如果按1⃣️式和2⃣️式的推导应该得出 purchase =cash paid to suppliers +deta A/P+Dep…

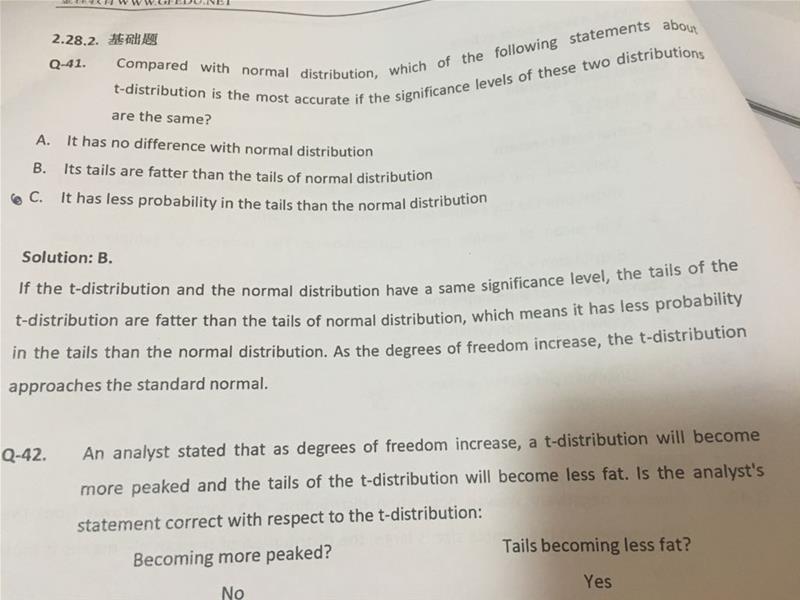

我的Q41题 C感觉有疑问。答案 which means it has less ...不就是C么?答案写的有误吧 C是错的 如何是fatten tail ,两边都是拒绝的region,所以越不peak,L越小,fatten越大 more 概率in tail,则CI越大,可否这样理解呢? 在tail 上的probability 请问应该怎么理解?

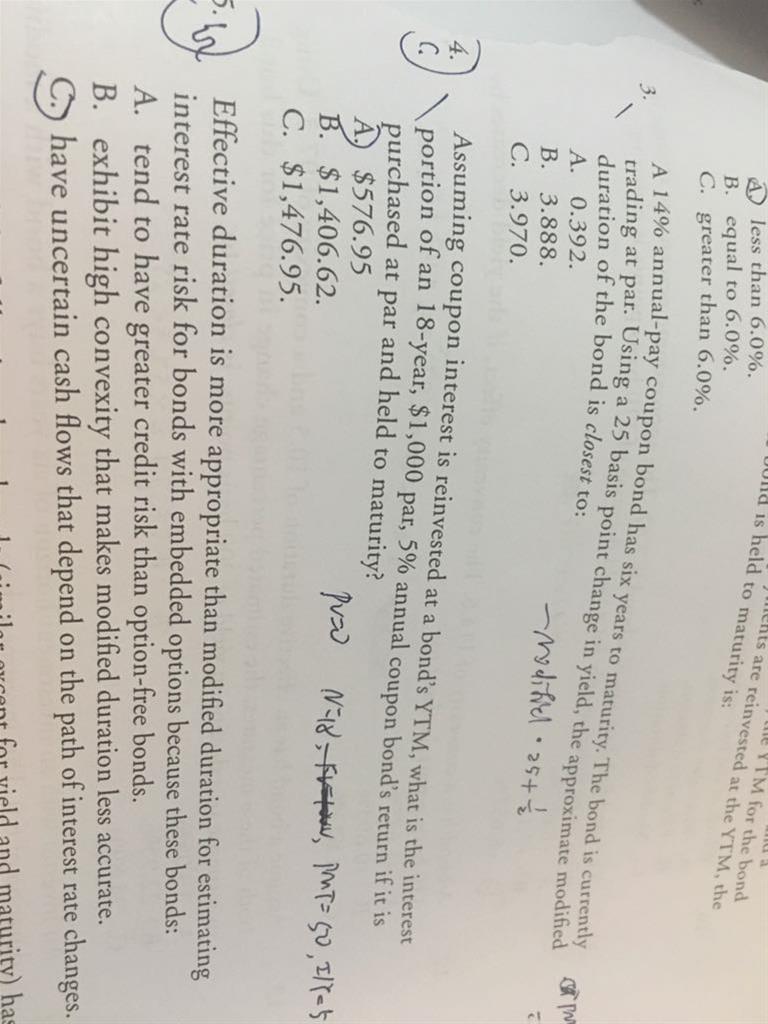

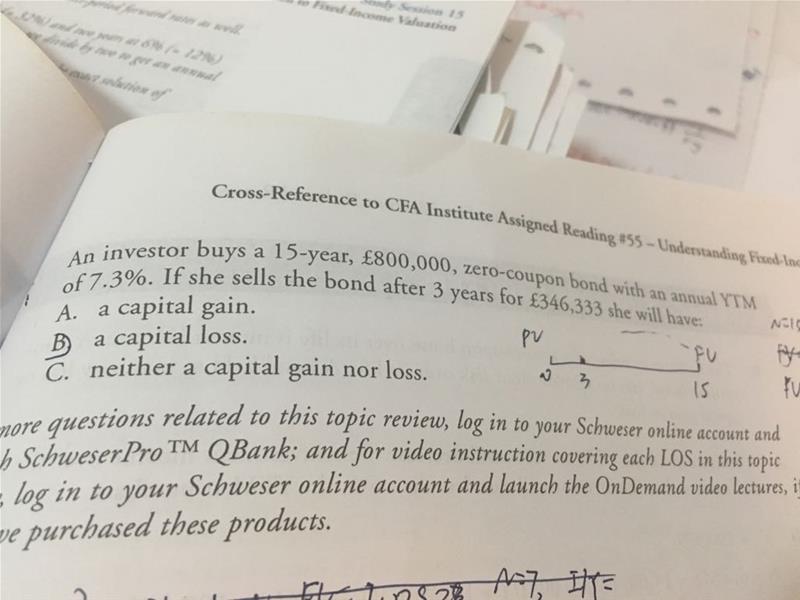

关于fix income的计算,现在有些值在题目里如果给出 PV和FV分不太清楚,网课也说了,FV就是终值 一般是par value, 根据做题发现 PV 一般题目出现current price才有值 其他情况都是0,这样说对么? 下面的第一幅图 第四题 我的问题是 为何这里FV不是1000 而是1406 第二幅图 第16题 我明白应该画图 使用cash flow折一下 但是抛开这道题 请问800000 是FV么?现在看到一个题 我会很机械的把FV定为1000/100,PV为0,除非有明确的current price/price at 98 of par value,我才认为PV不等于0.:所以可否帮助下 一个题怎么分清FV 还是PV呢?

在corporate finance和FSA里 分解看到 net sale ,Revenue . sales,cost of sales,sales revenue, credit sale, 记得老师说过 credit sales是最严格的, 但在计算ratio需要用sales的时候 credit sale不给 就可以用revenue,请问上述这些revenue,在一级里可以默认是等价的么?因为题目做完发现 sale/revenue的名字可以变化 我担心以后分不清

已回答At the beginning of 20X6, Cougar Corporation enters a finance lease requiring five annual payments of $10,000 each beginning on the first day of the lease. Assuming the lease interest rate is 8%, the amount of interest expense recognized by Cougar in 20X6 is closest to: A $2,650. B $3,194. C $3,450 为何我用金融计算器算出来的PV是33927.1,interest expense*0.8正好等于3194?

查看试题 已回答

精品问答

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

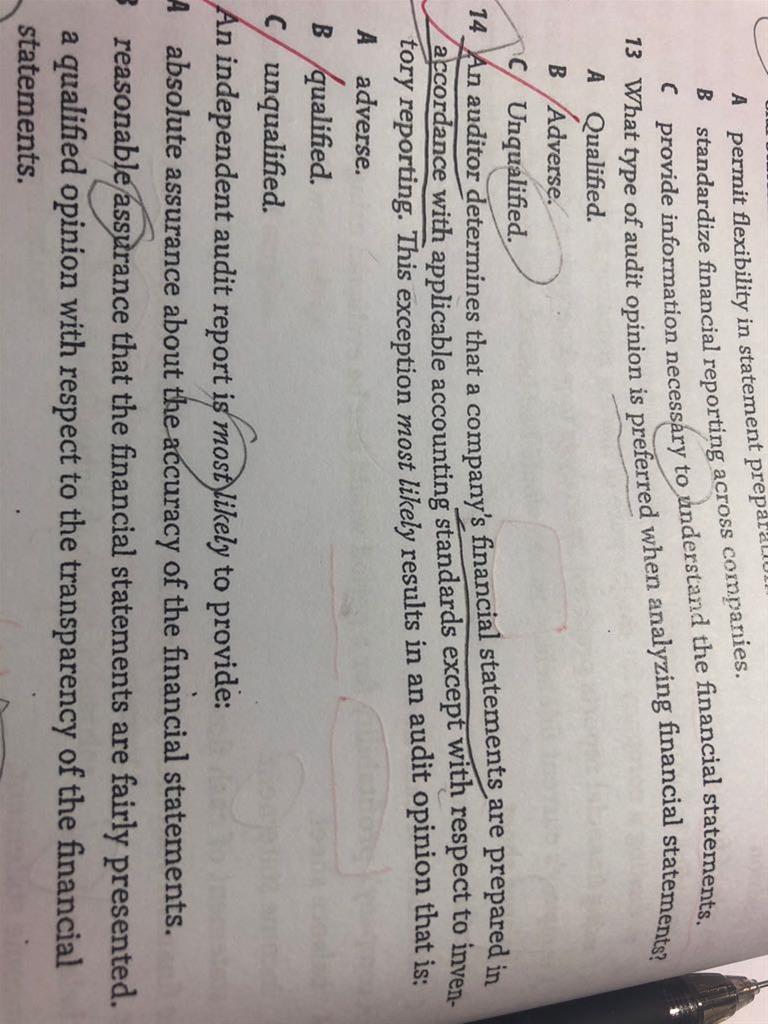

- 为什么长期垄断竞争中 D和ATC相切

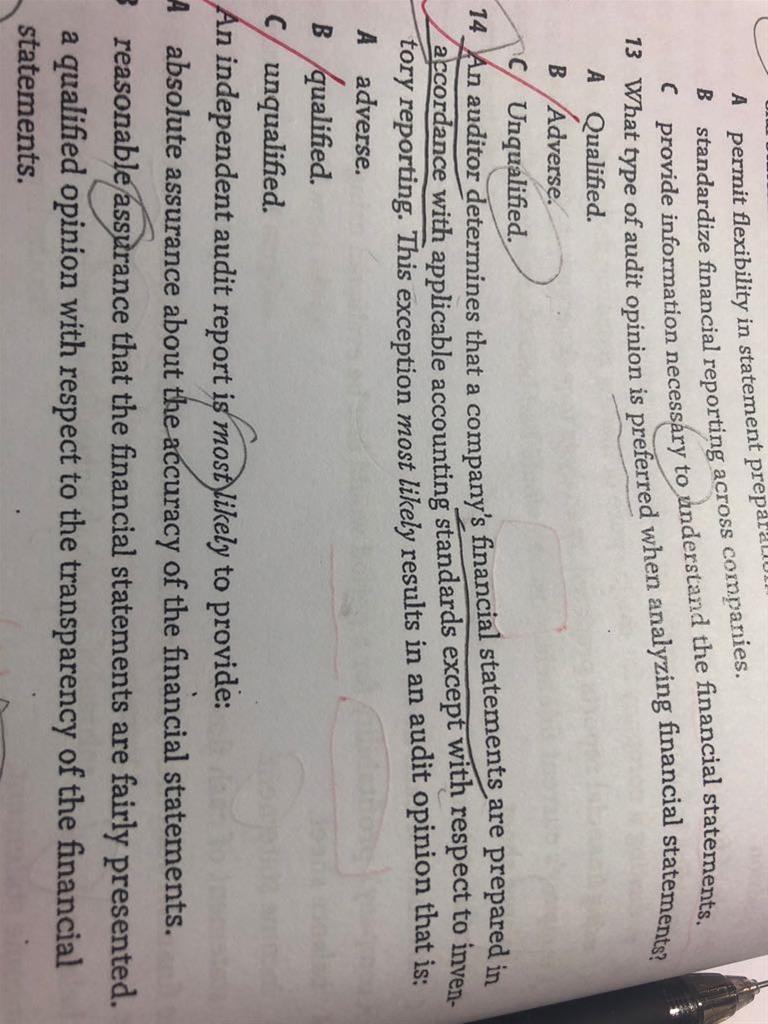

- m上升 EAR为什么上升 以及为什么又不变

- 为什么TC 的切点对应是AVC的最低点?

- 前面在讲Aggregate demand curve的时候说,价格上涨使消费下降,而这里又说价格下降消费变少,为什么存在矛盾?

- 为什么可以把TR TC同时体现在纵轴?

- 对于老师讲的这部分,1. 我理解FRA的Payoff始终等于利率期货的Payoff部分进行折现(除以1个大于1的数),也就是说,FRA的Payoff的变动幅度 应该 始终小于利率期货的变动幅度。2. 至于是涨多跌少,还是涨少跌多,其实MRR在分母上,可以根据1/x的曲线特点来理解,无非就是MRR上升时1/(1+MRR)的变动幅度 小于 MRR下降时1/(1+MRR)的变动幅度,所以如果MRR上升时,Payoff是上升的,那么就是涨少跌多,如果MRR上升时,Payoff是下降的,那就是涨多跌少。以上2点,我理解的对吗?