-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

C is incorrect because derivatives are not needed to copy strategies that can be implemented with the underlying on a standalone basis. Rather, derivatives can be used to create strategies that cannot be implemented with the underlying alone. Simultaneously taking long positions in multiple highly liquid fixed-income securities is a strategy that can be implemented with the underlying securities on a standalone basis.这个解释没看懂,尤其是 on a standalone basis.是啥意思呢

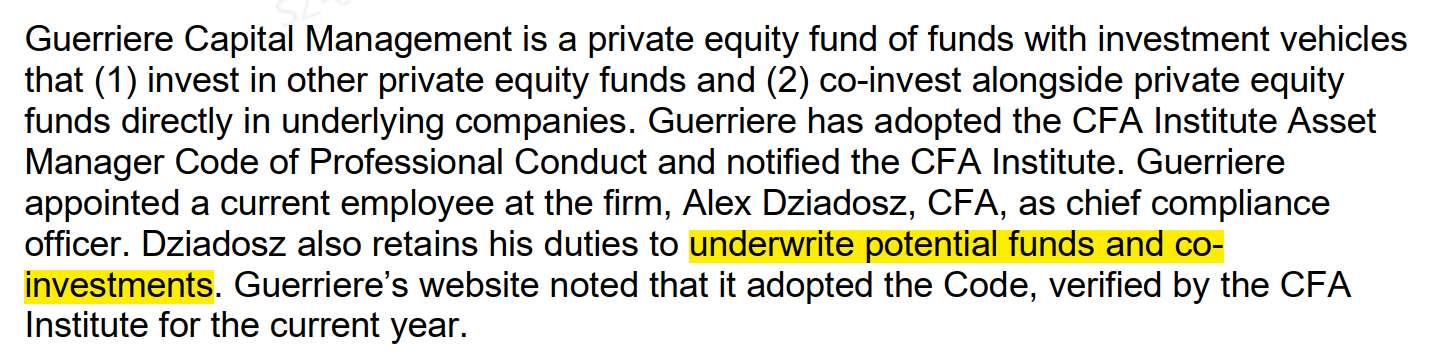

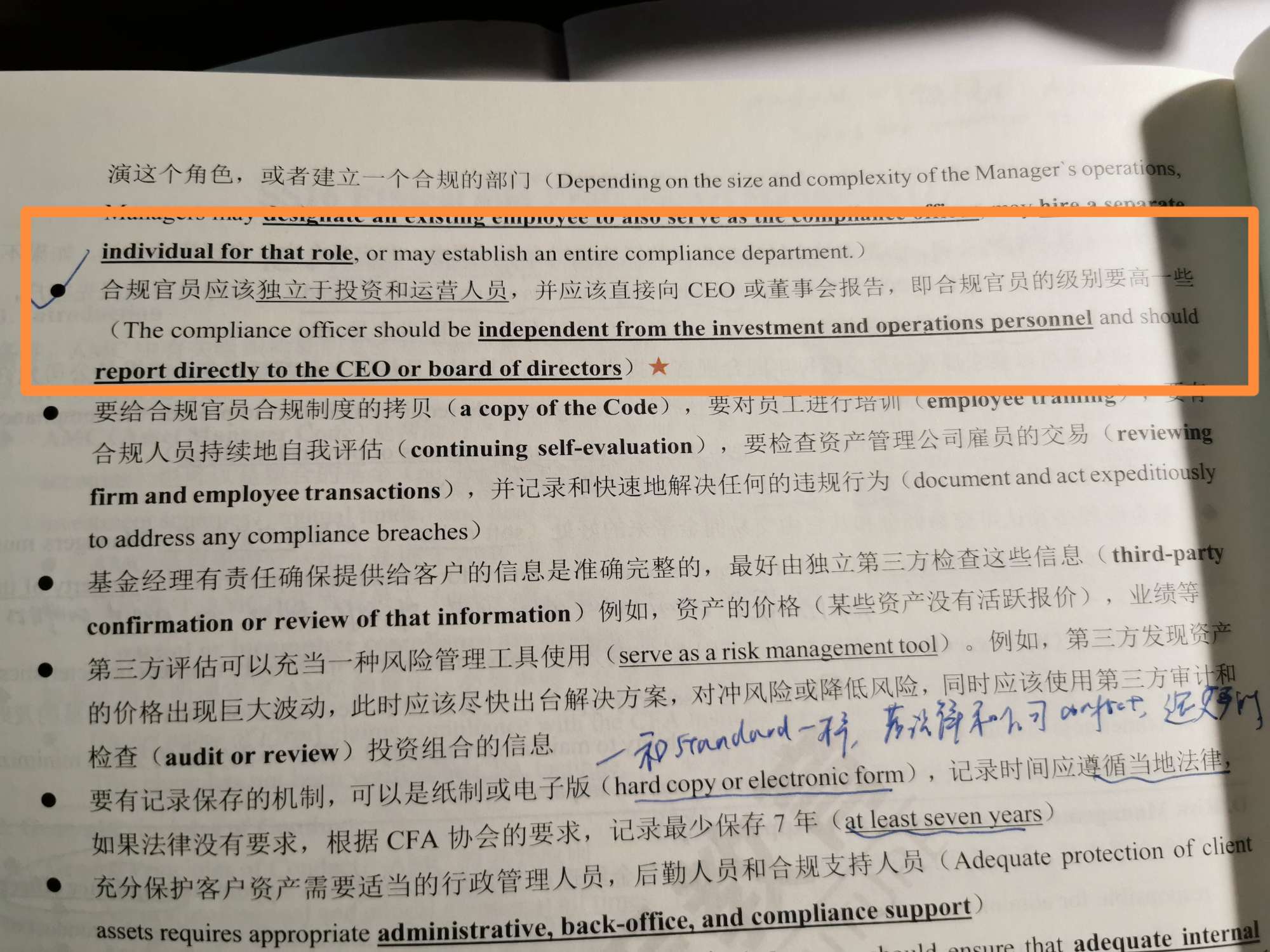

查看试题 已回答老师,官网mock题第19题,这个被任命为合规官员的人不是还同时从事了co-investment, 冲刺笔记上写说合规官员应该独立予投资和运营人员,那这个不应该就是voilate,应该选C吗?

老师,reading28 第41题,这道题考察什么知识点,为什么two-standard-deviation increase in the steepness factor直接就是-0.3015%×2呢,为什么是负数呢,是因为是标准差的increase吗 ?表中level、steepness、curvature的正负号表示什么

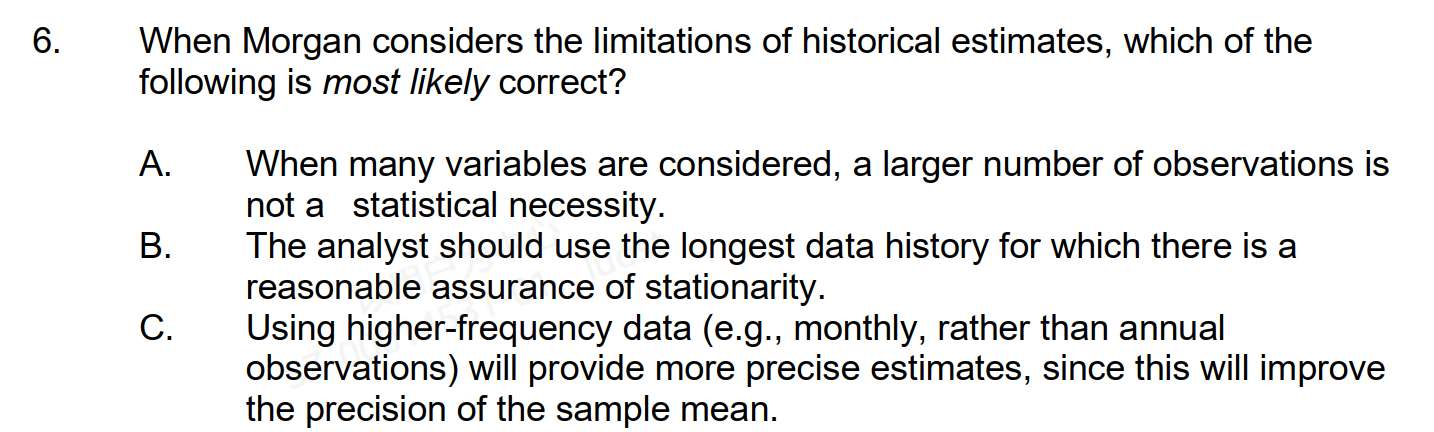

老师,CME的官网模考题,这一题说要用longest data history data,太长时间数据不是更容易涵盖multiple regime, 进而导致nonstationarity吗?为什么反倒说是assurance of stationarity

精品问答

- Q6,为啥要少抽失败的,少抽不就不能真实反应情况了吗?

- BG检验就是T检验吗?如果理解错误的话 T检验是什么?

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- Risk Budget and risk parity 第二道思考题,里面的Variance是不是完全是个冗余信息,给来误导的呀?

- liability relatibe asset allocation这三种方式的区别是什么呀 怎么区分

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- 为什么长期垄断竞争中 D和ATC相切