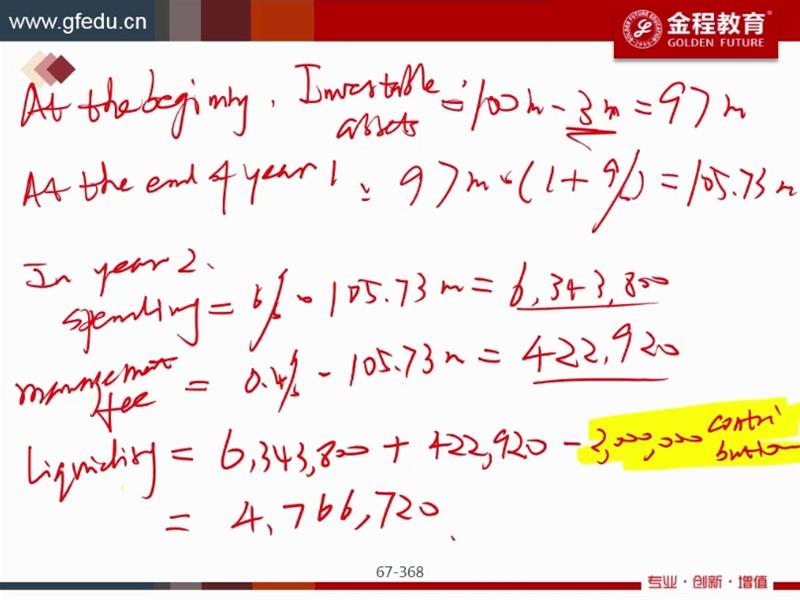

-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

专场人数:0提问数量:0

老师您好 这道题目中"The firm is expected to continue to grow in the foreseeable future" 为什么是理解为以后不可回转从而将DTL视为Equity呢?[我理解DTL不可回转计提Equity 但不理解为什么公司持续经营就意味着DTL无法回转]

查看试题 已回答

精品问答

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

- Risk Budget and risk parity 第二道思考题,里面的Variance是不是完全是个冗余信息,给来误导的呀?

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- Growth due to capital deepening 是αΔK/K还是ΔK/K

- 为什么TC 的切点对应是AVC的最低点?

- 老师,给最新的信息更高权重为什么不是availability bias呢?

- 她对个人笔记本电脑(personal laptop)进行了完整备份(full backup),并确保备份前已删除所有公司文件(all company files removed)。 目的:确保新备份中不包含任何前公司数据,避免合规风险。 遗留问题: 硬盘上的旧备份(previous backups)仍包含公司文件。 她不想因删除旧备份而丢失个人文件的备份历史(backup history for personal files)。 针对上述分析我有个疑惑,这个人不是已经在自己笔记本上备份了drive上的个人信息吗,怎么又Not wanting to lose the backup history for her personal files呢?他不是已经把自己的私人信息备份了吗!?

- 这里第二题的意思是三种方法都适用吗?没太理解,能否在讲解下