-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

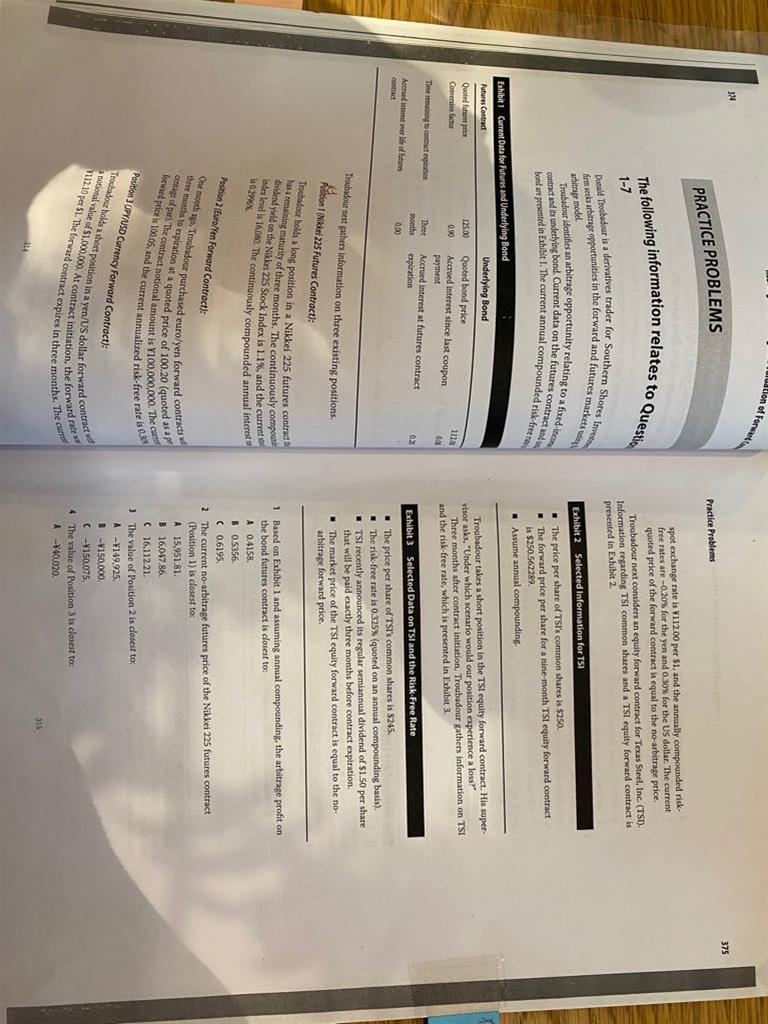

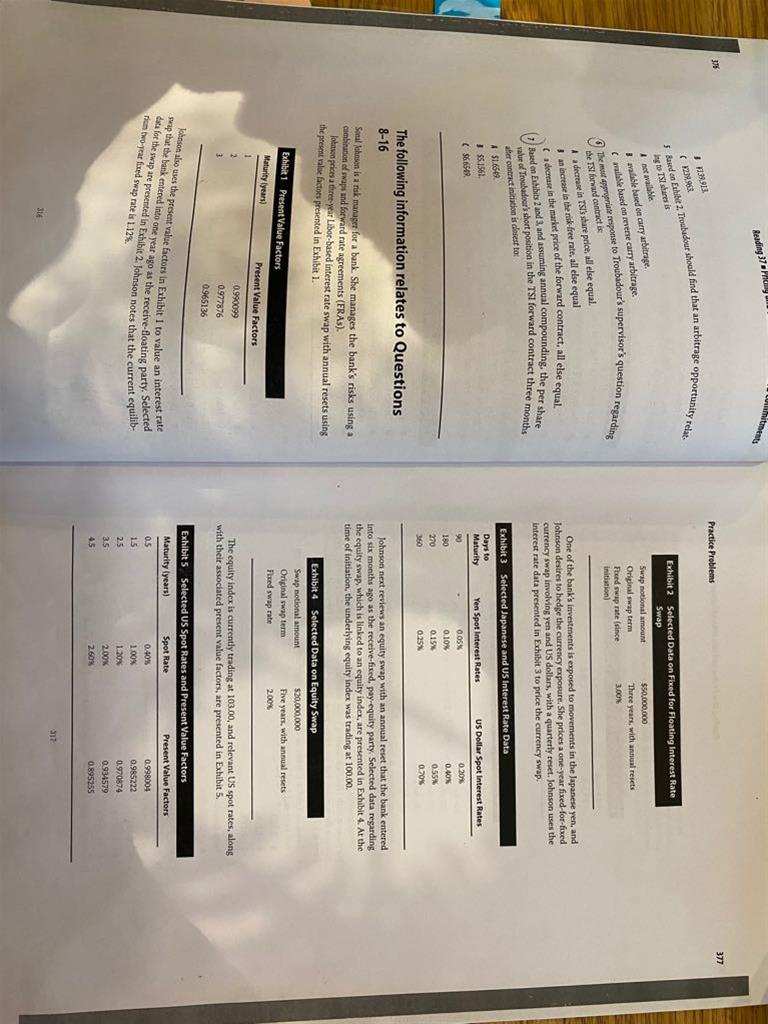

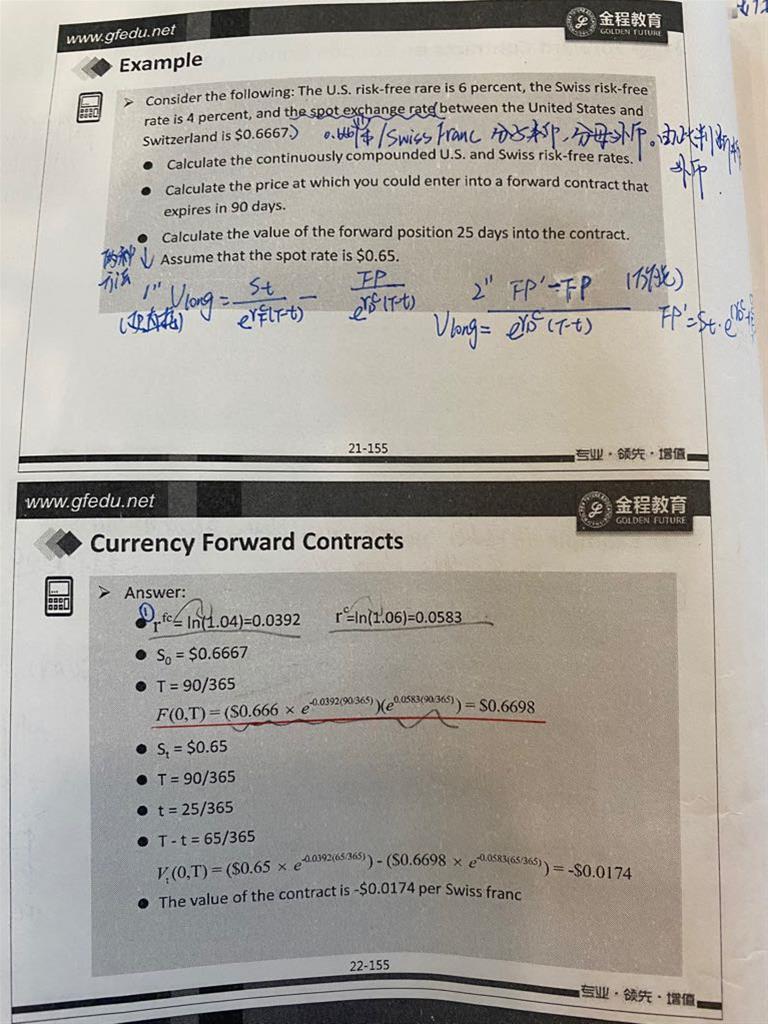

1. 第一图第1题问题让求套利 实际就是让求的future price? 我不太明白这个问题 第二,文中第一段说是在看forward和futures两个市场间是否有利可套,这和第一个问题(我理解第一问题在问期货市场下bond套利)矛盾么?2. 第5题,无风险利率为什么用0.3%,我如果第一次遇到这题,我会纠结下无缝利率用哪个?3. 第6题,实际在让我求valuation,我签这份合约赚不赚钱,对么?所以,我要用valuation公示去做一个判断 4. 第6题 C这个选项是什么意思?5. 第7题,怎么读出来是t=3这个时点在求估值?是题目中么?为什么利率折现要折到3/12这个时点?文章中最后一句话 市场价等于无套利的forwardprice 这是什么意思?6. 第三图,rf= ln(1+rf)是告诉如何从risk free rate 转到 continuous compounded risk free rate 么?

精品问答

- Q6,为啥要少抽失败的,少抽不就不能真实反应情况了吗?

- Q3:解析里面Team Purple’s conclusion (the externalities associated with human capital is the most important determinant in predicting the occurence of convergence) implies that the production function is a straight line, and is compatible with non-convergence.这段话中 externalities associated with human capital具体是什么?怎么得到the production function is a straight line这个结论呢?

- Risk Budget and risk parity 第二道思考题,里面的Variance是不是完全是个冗余信息,给来误导的呀?

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- Growth due to capital deepening 是αΔK/K还是ΔK/K

- 为什么TC 的切点对应是AVC的最低点?

- 老师,给最新的信息更高权重为什么不是availability bias呢?

- BG检验就是T检验吗?如果理解错误的话 T检验是什么?