-

CFA一级

包含CFA一级传统在线课程、通关课程及试题相关提问答疑;

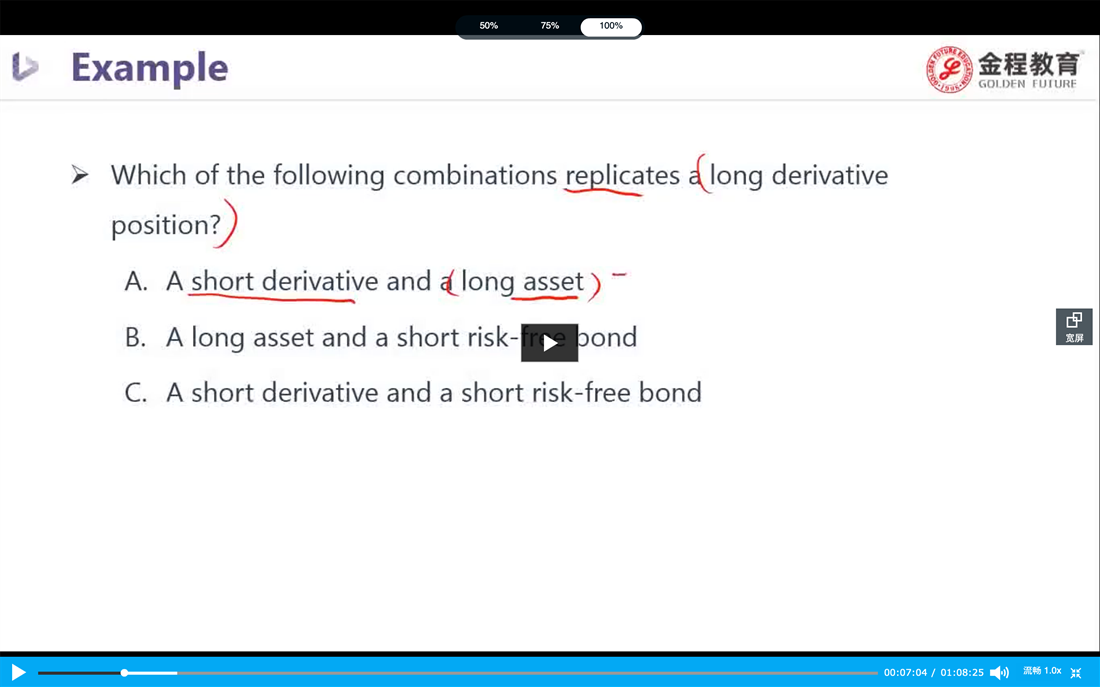

老师,这道题我感觉哪个选项都不对。您看我的理解哪里有问题: 以下是我的解题思路: 这道题主要考察的说Asset+Derivative=Risk-free asset这个公式,用这个公式的变形得出+Derivative。 选项A -Derivative+Asset,与公式不符,不能选; 选项B Asset- Risk-free asset=-Derivative,是short了一个Derivative,也不选; 选项C -Derivative- Risk-free asset,与公式不符,不能选。

老师好!题目如下: A consultant starts a project today that will last for three years. Her compensation package includes the following: If she expects to invest these amounts at an annual interest rate of 3%, compounded annually until her retirement 10 years from now, the value at the end of 10 years is closest to. 题目中的annual interest rate和EAR的区别是什么呢?为什么计算中使用的是EAR而不是annual interest rate呢?感觉有点混乱。

已回答精品问答

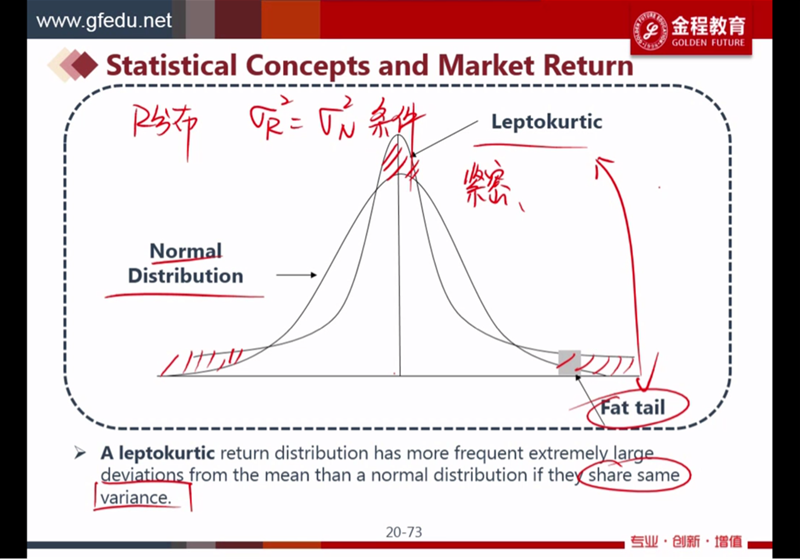

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- 为什么长期垄断竞争中 D和ATC相切

- m上升 EAR为什么上升 以及为什么又不变

- 为什么TC 的切点对应是AVC的最低点?

- 前面在讲Aggregate demand curve的时候说,价格上涨使消费下降,而这里又说价格下降消费变少,为什么存在矛盾?

- 为什么可以把TR TC同时体现在纵轴?

- 对于老师讲的这部分,1. 我理解FRA的Payoff始终等于利率期货的Payoff部分进行折现(除以1个大于1的数),也就是说,FRA的Payoff的变动幅度 应该 始终小于利率期货的变动幅度。2. 至于是涨多跌少,还是涨少跌多,其实MRR在分母上,可以根据1/x的曲线特点来理解,无非就是MRR上升时1/(1+MRR)的变动幅度 小于 MRR下降时1/(1+MRR)的变动幅度,所以如果MRR上升时,Payoff是上升的,那么就是涨少跌多,如果MRR上升时,Payoff是下降的,那就是涨多跌少。以上2点,我理解的对吗?