-

CFA一级

包含CFA一级传统在线课程、通关课程及试题相关提问答疑;

专场人数:6085提问数量:109940

Using the above data, an analyst is trying to test the null hypothesis that the population variances are equal() against the alternative hypothesis that the variances are not equal ()at the 5% level of significance. The following table provides the F-distribution. Which of the following statements is most appropriate? The critical value is: A 9.60 and do not reject the null. B 7.15 and do not reject the null. C 6.39 and reject the null. 老师这种题是否需要掌握?

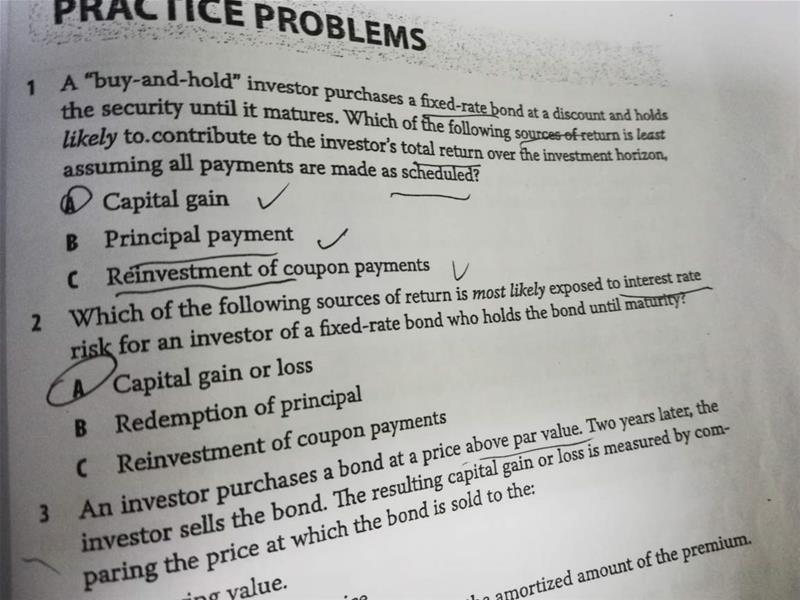

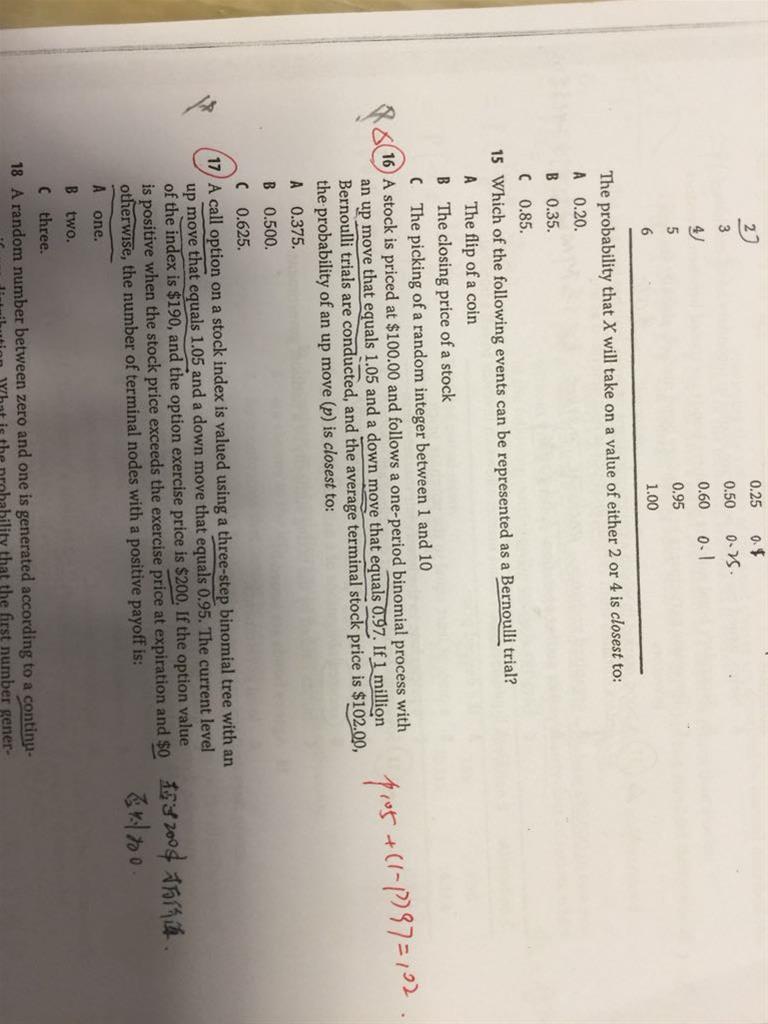

查看试题 已回答原版书后题第259页第2题,主要是A和C我认为都是一样的,因为是持有到期,那资本到期是固定PAR VALUE ,但是每期的COUPON 也是固定收到的,根据发行说好的COUPON RATE计算,这有什么风险? 所有东西都是固定的,没有提前赎回。

Which of the following statements about hypothesis testing is least accurate? A A type I error is to reject the null when it is actually true. B The significance level equals the probability of a Type I error. C A two-tailed test with a significance level of 5% has z-critical values of ±1.65. b有点不明吧,significance level 指的是两边的区域吧,可以定义为type1吗?

查看试题 已回答

精品问答

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- 为什么半年付息 算ytm是乘以2 而年化的麦考利久期是除以2

- 为什么长期垄断竞争中 D和ATC相切

- m上升 EAR为什么上升 以及为什么又不变

- 为什么TC 的切点对应是AVC的最低点?

- 前面在讲Aggregate demand curve的时候说,价格上涨使消费下降,而这里又说价格下降消费变少,为什么存在矛盾?

- 为什么可以把TR TC同时体现在纵轴?

- 对于老师讲的这部分,1. 我理解FRA的Payoff始终等于利率期货的Payoff部分进行折现(除以1个大于1的数),也就是说,FRA的Payoff的变动幅度 应该 始终小于利率期货的变动幅度。2. 至于是涨多跌少,还是涨少跌多,其实MRR在分母上,可以根据1/x的曲线特点来理解,无非就是MRR上升时1/(1+MRR)的变动幅度 小于 MRR下降时1/(1+MRR)的变动幅度,所以如果MRR上升时,Payoff是上升的,那么就是涨少跌多,如果MRR上升时,Payoff是下降的,那就是涨多跌少。以上2点,我理解的对吗?