187****25992024-05-09 15:41:52

187****25992024-05-09 15:41:52

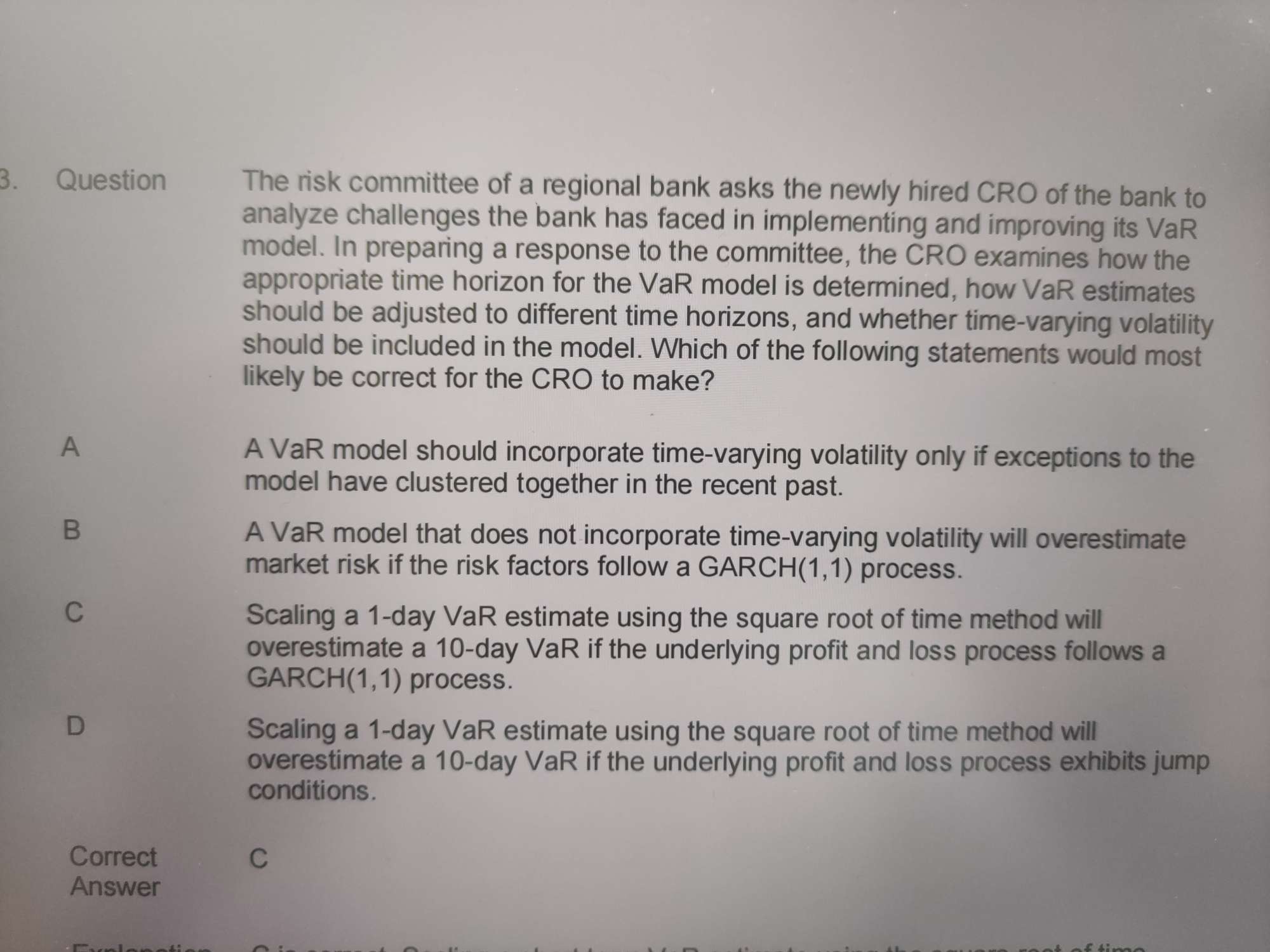

老师这道题每个选项是什么意思,怎么理解?毫无头绪。

回答(1)

黄石2024-05-10 11:13:46

黄石2024-05-10 11:13:46

同学你好。这道题主要考查的是原版书中一篇文献综述里的内容,这些都是文献里的结论,我的建议是有时间的话稍微记一下这些结论就可以了,至于这些论文用了哪些数据、用了什么方法就不需要去了解了。同时,对于这些实证研究,其实换个方法换组数据完全可能有不同的结果。原文如下:

The accuracy of square-root of time scaling depends on the statistical properties of the data generating process of the risk factors. Diebold et. al. (1998) show that, if risk factors follow a GARCH(1, 1) process, scaling by the square-root of time overestimates long horizon volatility and consequently VaR is overestimated. Similar conclusions are drawn by Provizionatou, Markose and Men kens (2005). In contrast to the results that assume that risk factors exhibit time-varying volatility, Danielsson and Zigrand (2006) find that, when the underlying risk factor follows a jump d iffusion process, scaling by the square root of time systematically underestimates risk and the downward bias tends to increase with the time horizon.

- 评论(0)

- 追问(1)

- 追答

-

对于A选项的话,这个相当于是做法上的错误。我们不应该在出了问题之后才去找解决方案,而是防患于未然。更高阶的VaR模型一般都会摒弃volatility是恒定不变的假设,转而使用某些方法去建模时变波动率。

评论

0/1000

追答

0/1000

+上传图片