Ashu2023-02-27 22:17:26

Ashu2023-02-27 22:17:26

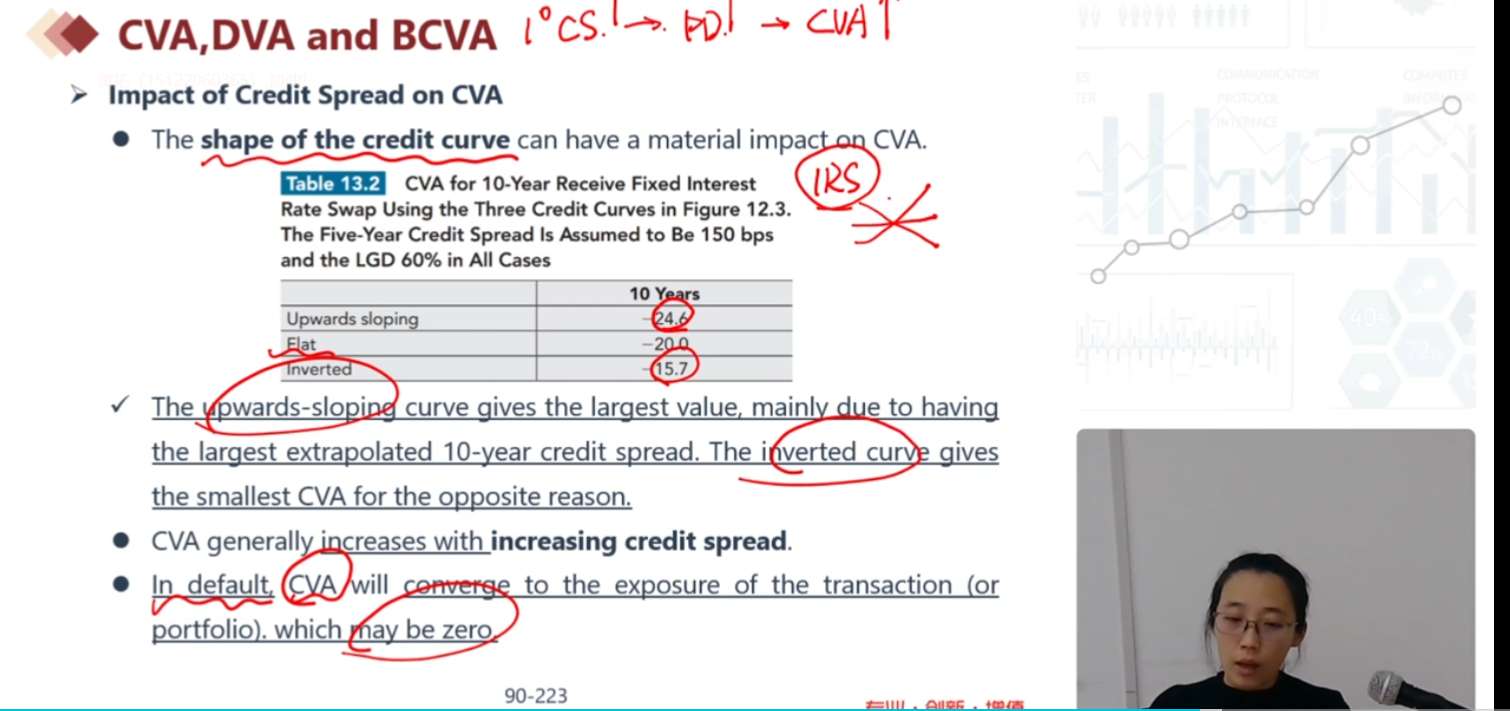

“When considering the shape of the credit spread curve, the CVA will be lower for an upward-sloping curve compared to a downward-sloping curve.”答案是这么描述的,对比课上的IRS,那么这种解释在哪种产品中成立呢?

回答(1)

最佳

Shawn2023-02-28 09:31:55

Shawn2023-02-28 09:31:55

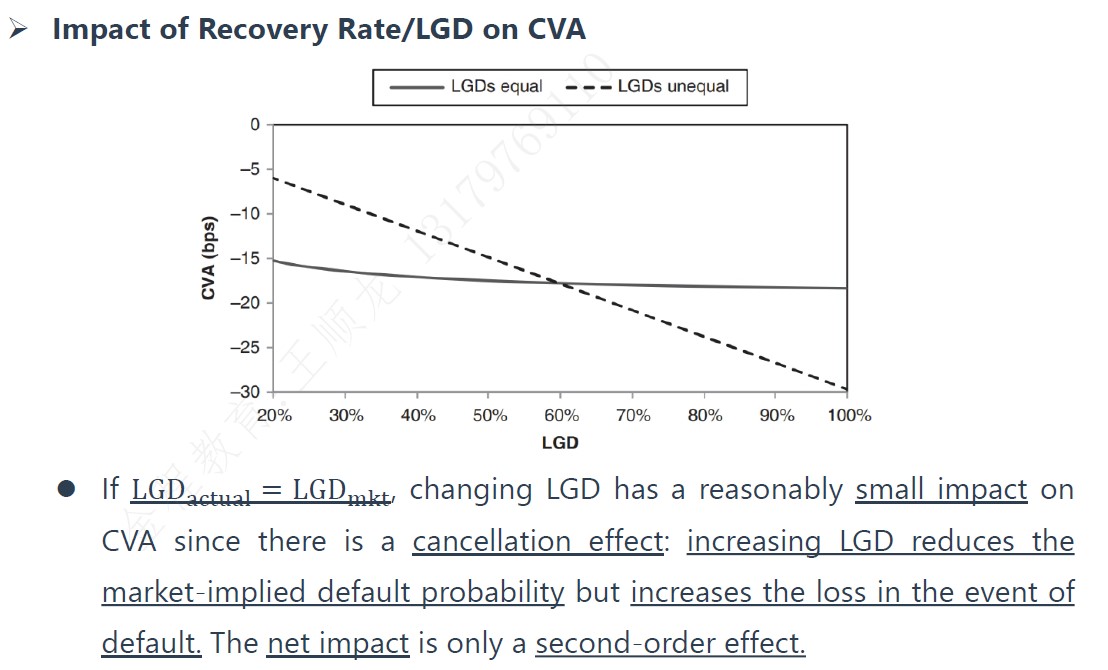

同学你好,我们注意一个问题,B选项错在它不严谨,因为credit spread和recovery rate对CVA的影响是不一样的。前者越大,CVA越大;后者越大,CVA越小。B选项这种说法只针对recovery rate。

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片