蛋同学2025-10-12 18:54:43

蛋同学2025-10-12 18:54:43

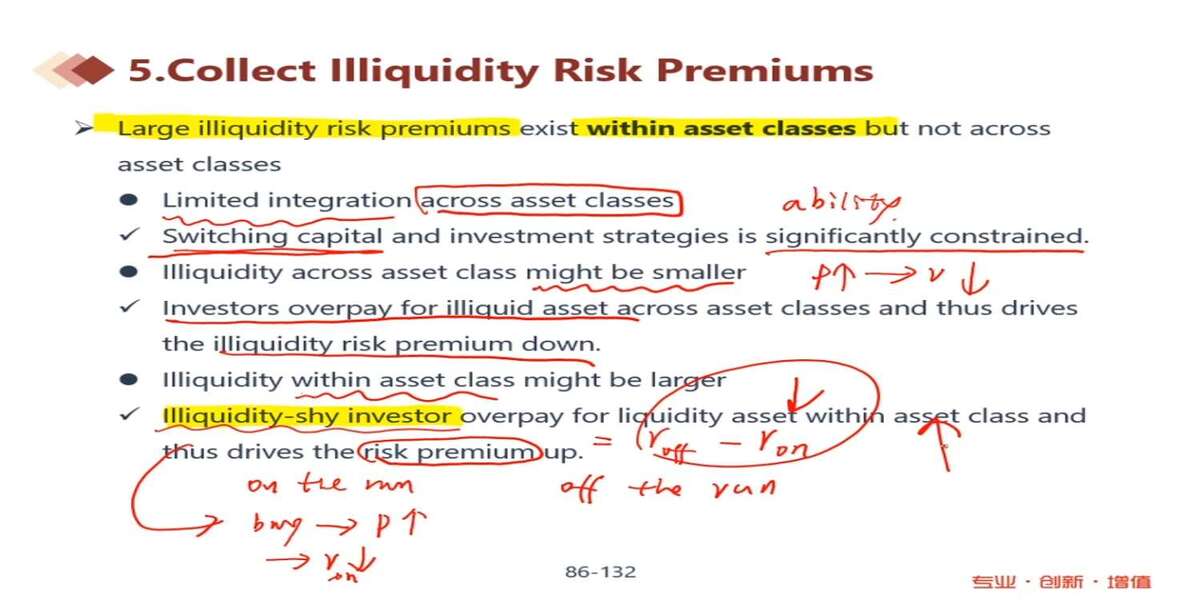

最后一段premium的计算公式是R(off)-R(on) ,但on the run的bond的R总归是比off的高吧,那这个premium是个负值吗?

回答(1)

苏学科2025-10-13 17:34:27

苏学科2025-10-13 17:34:27

on-the-run债券是最新发行的债券,通常流动性更高,因此投资者要求的收益率较低(即价格较高)。off-the-run债券是较旧发行的债券,流动性较差,因此投资者要求更高的收益率(即价格较低)。“Illiquidity within asset class might be larger” 和 “Illiquidity shy investor overpay for liquidity asset within asset class and thus drives the risk premium up。” 这意味着在资产类别内部,流动性差的资产风险溢价被推高,因此溢价应为正。所以,计算公式应为 Roff−Ron R off−Ron,结果为正。

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片