Jophia2020-10-19 10:00:38

Jophia2020-10-19 10:00:38

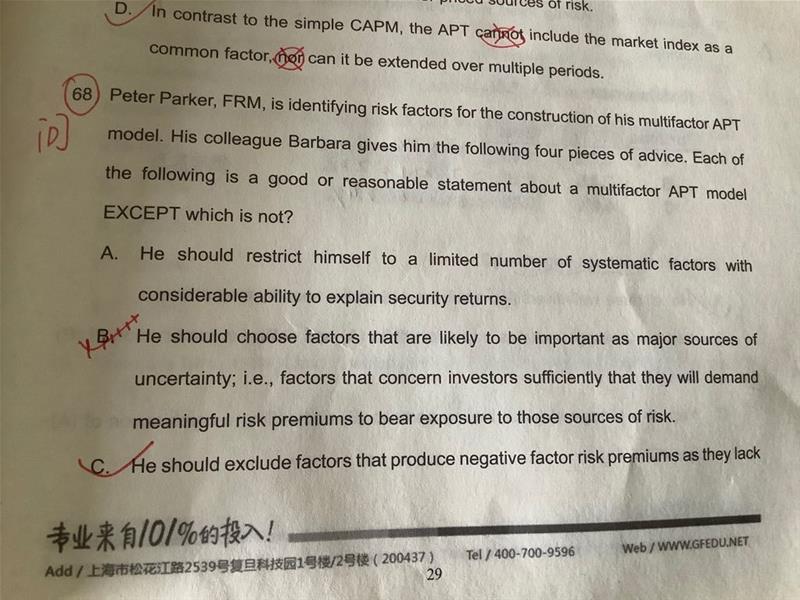

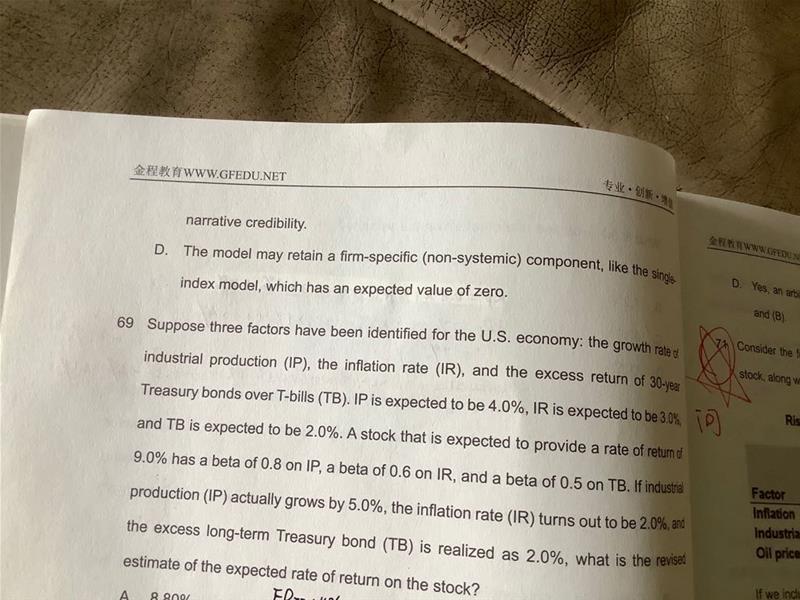

C错在哪里?以及apt假设有哪些

回答(1)

Jenny2020-10-22 13:36:46

Jenny2020-10-22 13:36:46

同学你好,

解释因子的系数是有可能为负的,只要她对收益有显著解释效力就应该包含进去。

apt 假设:

Asset returns can be explained by systemic factors.

By using diversification, investors can eliminate specific risk from their portfolios.

There are no arbitrage opportunities among well-diversified portfolios. If any arbitrage opportunities were to exist, investors would exploit them away.

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片