-

CFA问答

CFA问答包含CFA在线课程、CFA通关课程、CFA试题等所有CFA相关问题,每个问题老师均会在24小时内给出答疑回复哦!

历年真题2012年Q9的C题,答题计算时hedged position value 是1332股票的价值减去call option 的价值,题目中short call为了对冲风险long了1332股票,那么对冲指的是long的equity,为什么计算hedged position 时需要减去call option 的价值

A company previously expensed the incremental costs of obtaining a contract.All else being equal, adopting the May 2014 IA SB and FA SB converged accounteing standards on revenue recognition makes the co mpany's profitability initilynappear:nA lower.nB unchanged.nC higher.n这道题该怎么解?

已回答Under IFRS, income included increases in economic benefits from:nA increases in liabilities not related to owners contributions.nB enhancements of assets not related to owners' contributions.n C increases in owners'equity related to owners' contributions.n这道题涉及的内容在ppt中有讲到吗

已回答

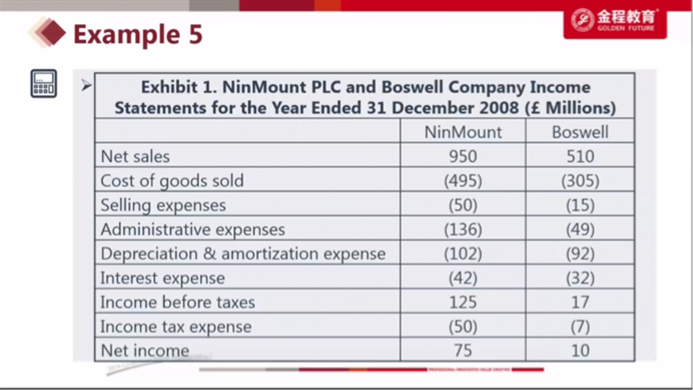

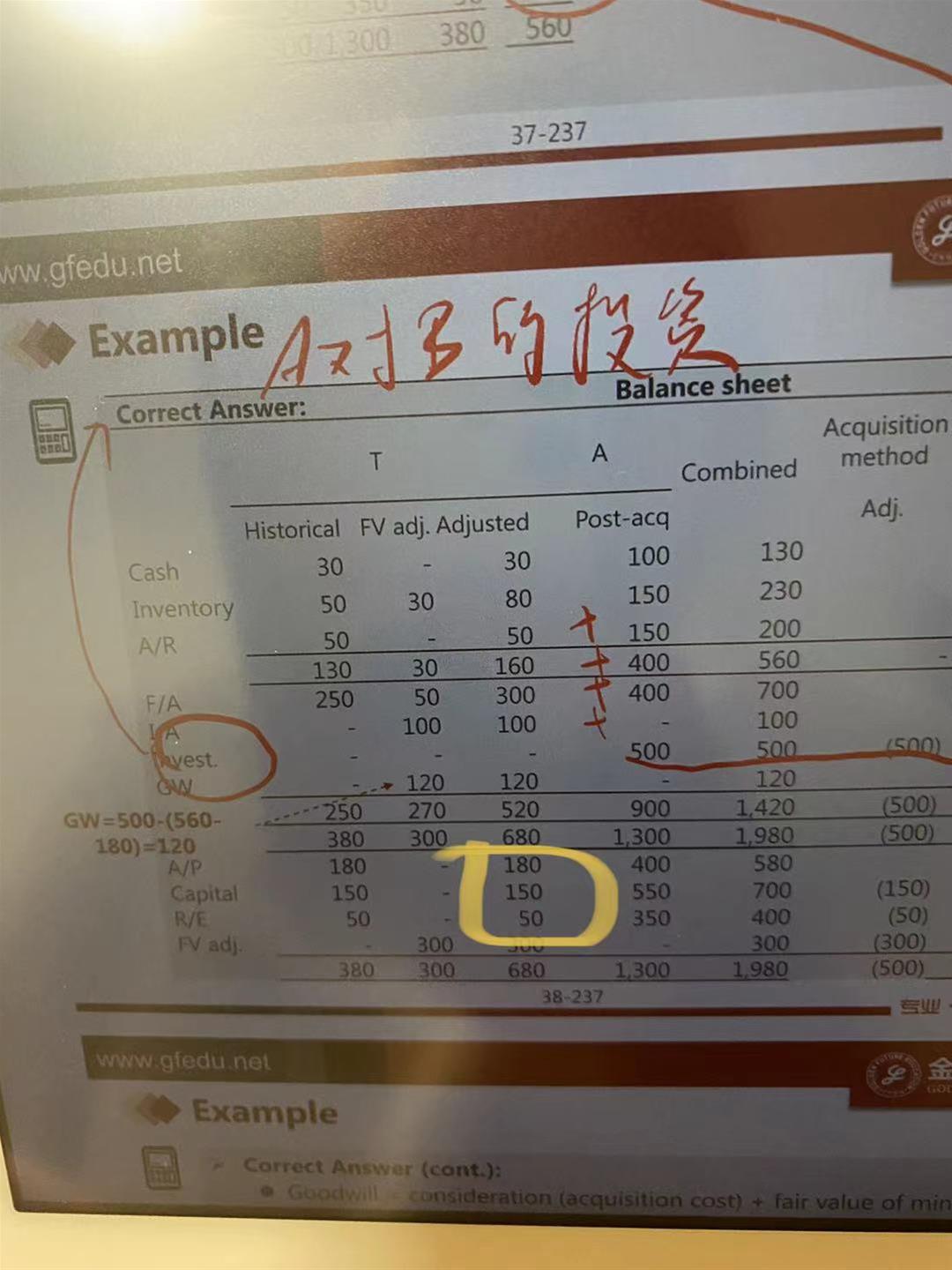

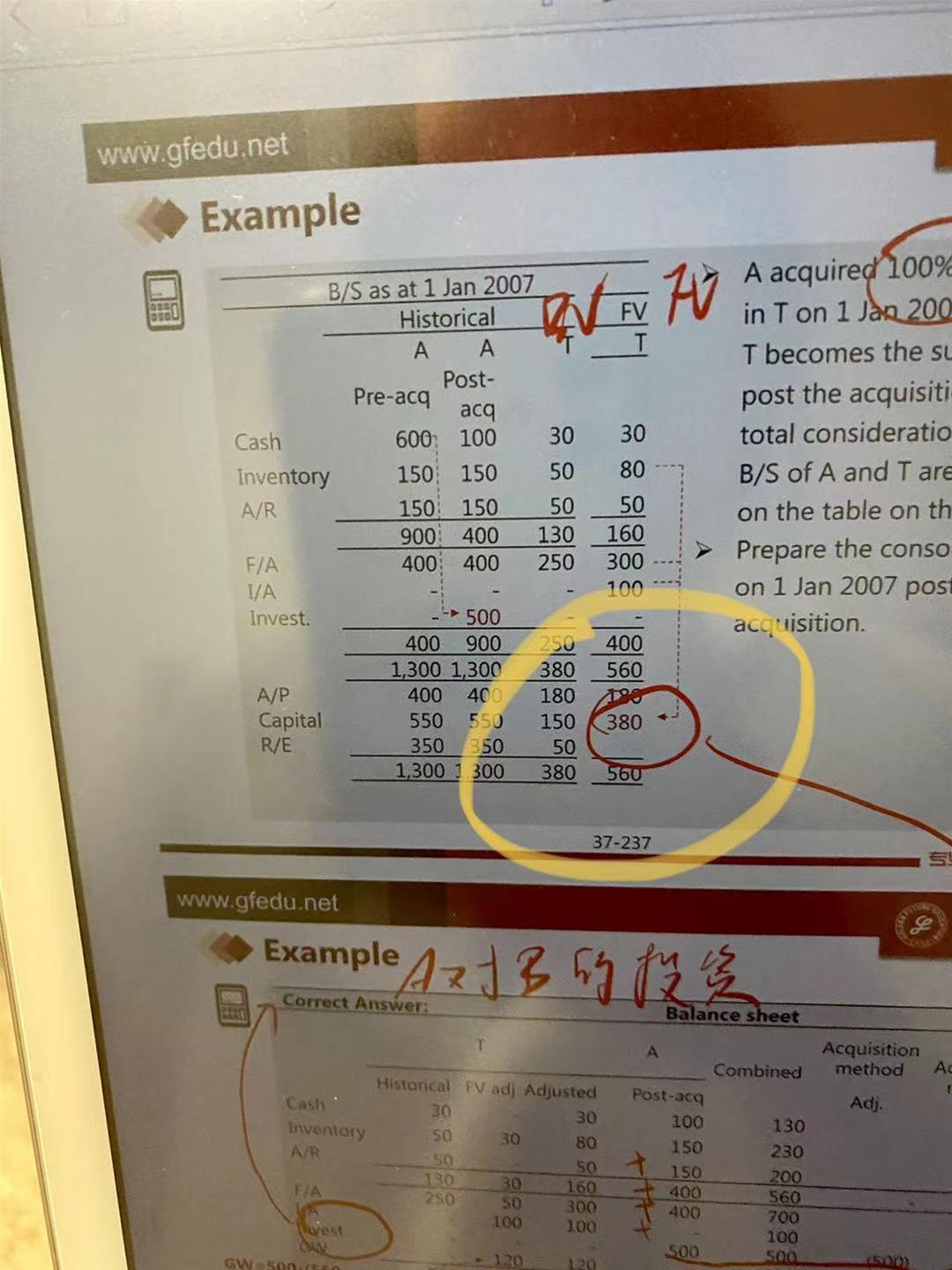

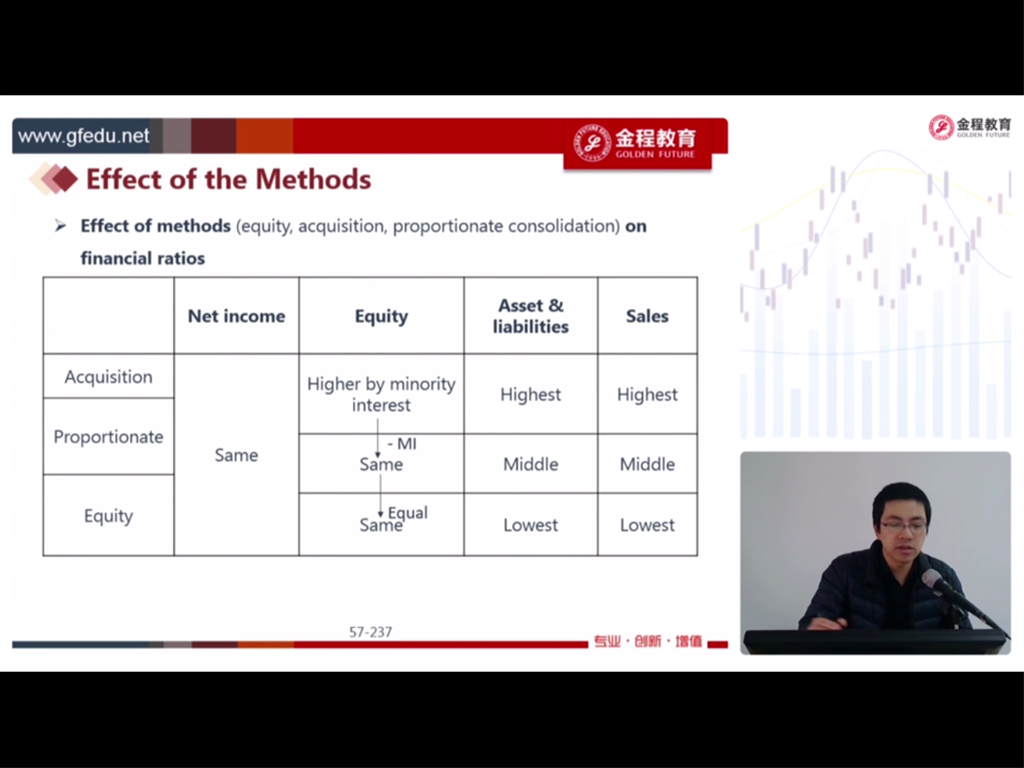

为什么proportionate和equity比 equity一样 但asset是proportionate高? equtiy method 下 asset怎么算?revenue又怎么算?谢谢

精品问答

- 倒数第二题,老师讲到,分析师预测的spot rate2年小于forward curve, 因此资产价格应该是被低估。但是在串讲课的时候,老师讲过5.1知识点,如图,如果吧spot rate2年带入讲义的S2,长期利率,forward curve带入f(1,1),那么当边际量f(1,1)小于平均量S2时,平均量应该下降,资产价格应该上升,为高估丫

- 想具体理解下打星号这个结论的推导过程 为什么收益率分布广了 cost低 为什么样本小 cost低 样本小不应该测不准吗?

- BG检验就是T检验吗?如果理解错误的话 T检验是什么?

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- liability relatibe asset allocation这三种方式的区别是什么呀 怎么区分

- 为什么长期垄断竞争中 D和ATC相切

- m上升 EAR为什么上升 以及为什么又不变

- 前面在讲Aggregate demand curve的时候说,价格上涨使消费下降,而这里又说价格下降消费变少,为什么存在矛盾?