彪同学2024-06-05 11:22:47

彪同学2024-06-05 11:22:47

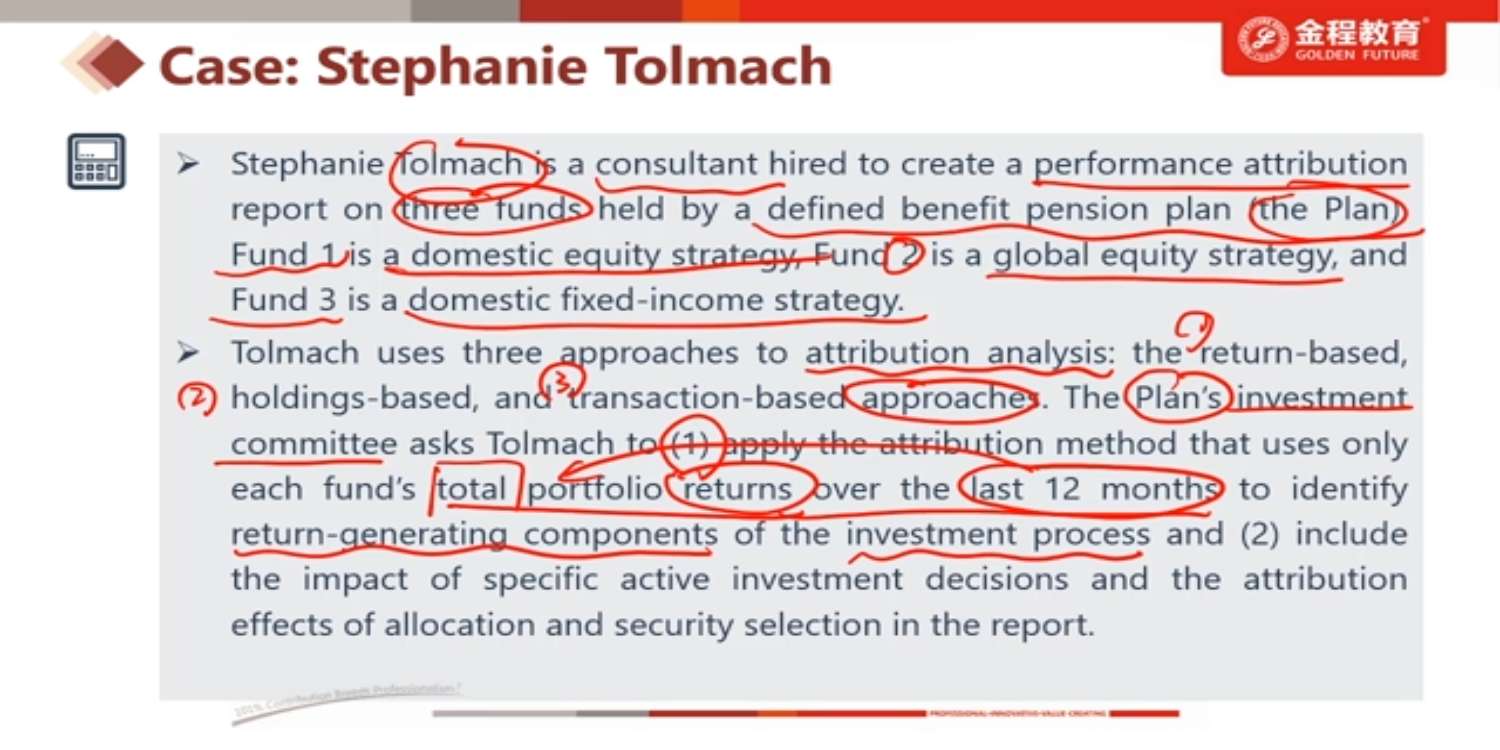

第二个条件不是在说holding-based attribution吗?return-based业绩归因是看总收益的,没法得到每个资产的权重,怎么考量allocation effect呢?

回答(1)

最佳

开开2024-06-11 09:39:04

开开2024-06-11 09:39:04

同学你好,return based也可以include the impact of specific active investment decisions and the attribution effects of allocation and security selection in the report.

其中,factor tilt return体现的就是allocation,是通过回归得到在因子上的beta,即因子的权重,从而计算出allocation的。

如果答疑对你有帮助,【请采纳】哟~。加油,祝你顺利通过考试~

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片