Yuzuru2024-04-14 17:08:51

Yuzuru2024-04-14 17:08:51

官网固收题,请问这题为什么C不对?记得课上老师说首先看direction 是否匹配benchmark。这题组合3和基准更符合,更像pure indexing

回答(1)

Simon2024-04-15 10:50:44

Simon2024-04-15 10:50:44

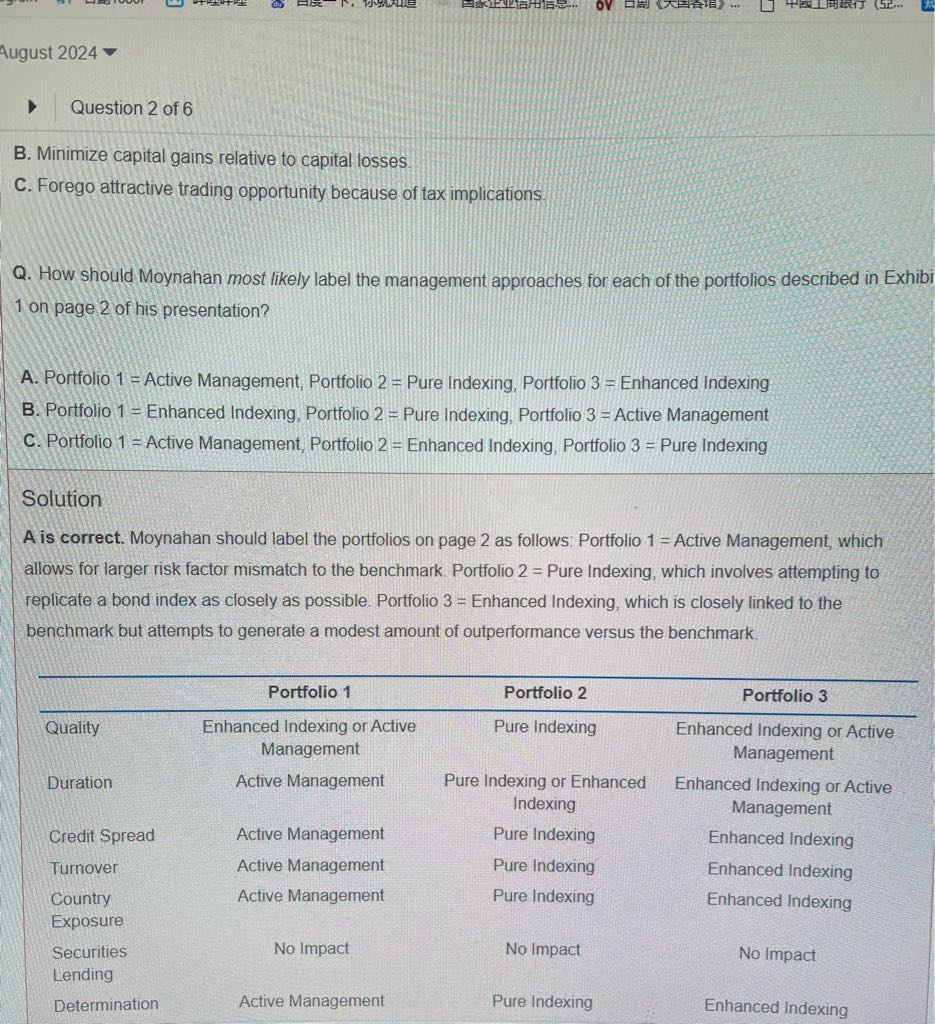

同学,上午好。exhibit 1好像没显示完整。可以补全下吗?然后,关于pure,enhanced,active,其判断标准参见截图知识点。

- 评论(0)

- 追问(2)

- 追问

-

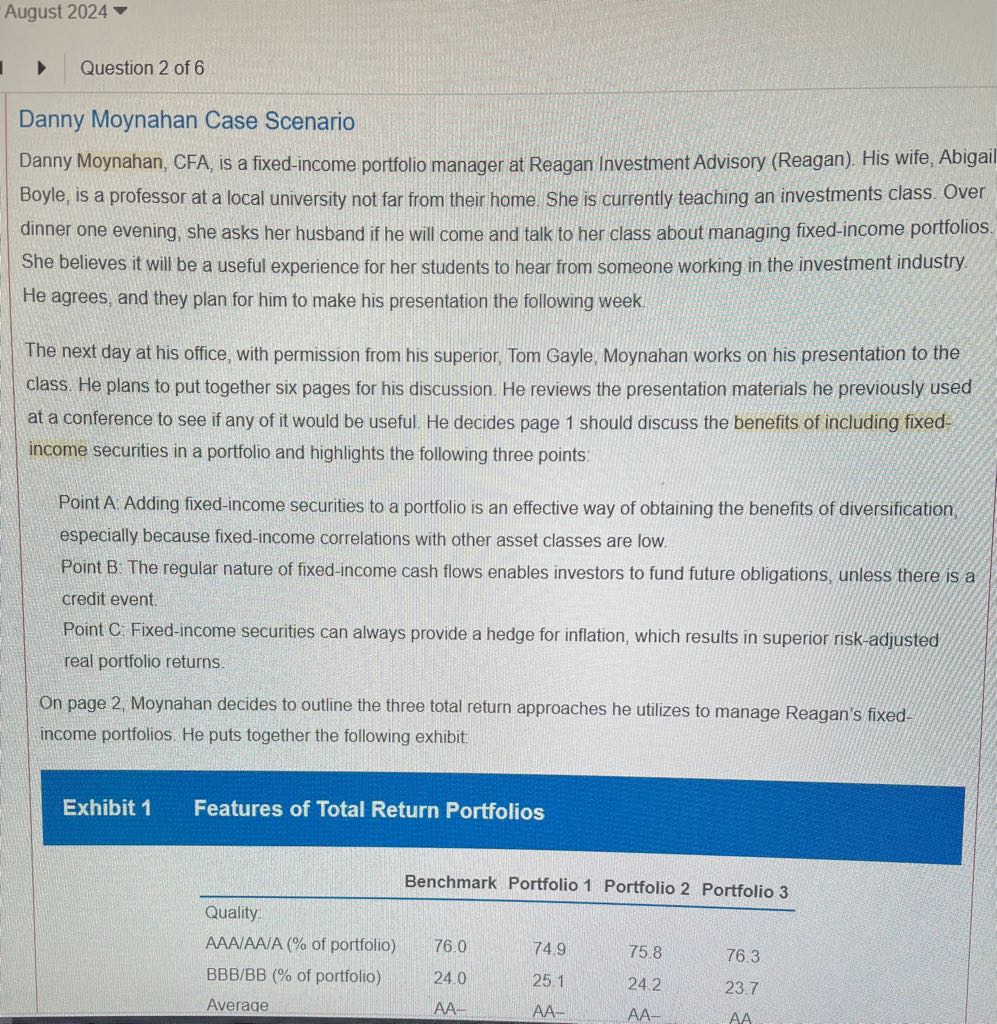

完整的表1,谢谢老师。

- 追答

-

同学,上午好。

这道题要表格里每一项数据都进行比较(securities lending不用看 ,因为benchmark没有信息)

pure index要求全部都closely match,所以portfolio 2 满足这个要求。基本上每一项都和benchmark出入都很小。

而enhanced要求duration closely match(主要是duration,KRD,spread duration),其他随意。所以可以看到表格里,portfolio 3,KRD这里还是匹配的,但是在credit和country exposure偏离就有些大了。

然后active,可以都不匹配,然后特点是Considerably higher turnover than the underlying benchmark,portfolio 1的 turnover是最高的。所以active。

评论

0/1000

追答

0/1000

+上传图片