赵同学2024-03-24 17:16:29

赵同学2024-03-24 17:16:29

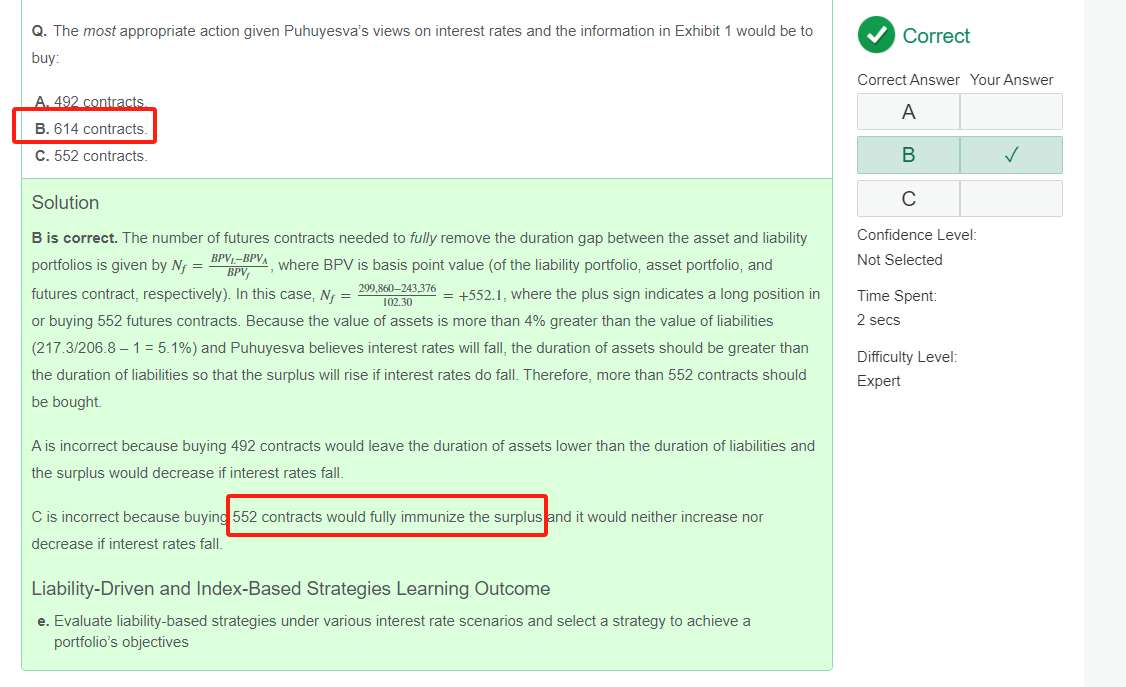

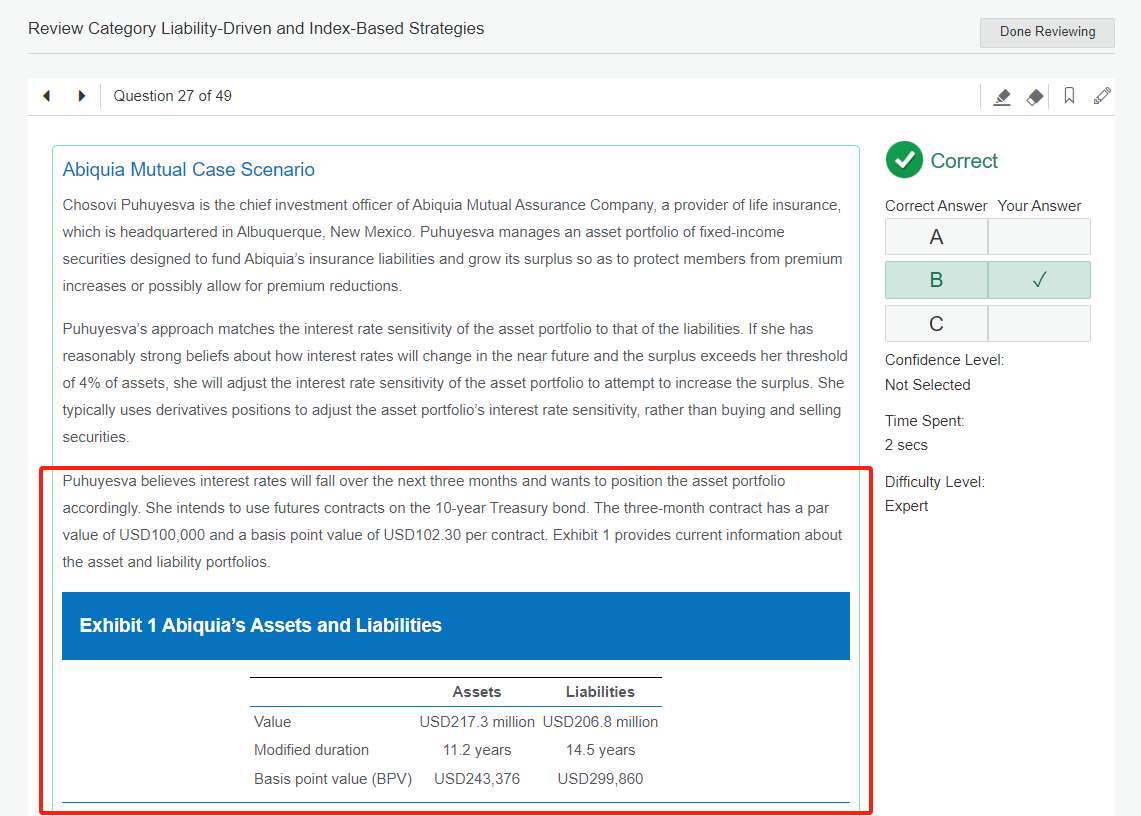

老师您好,请问官网题这里算出来是552 contracts,但选项却因为利率预期会下降,所以要买高于552contracts,我有些疑问,552已经fully immunization了,不论利率上涨还是下降都会刚好match上,为什么要因为利率预期下降而多配置一些futures?答案提到:Because the value of assets is more than 4% greater than the value of liabilities (217.3/206.8 – 1 = 5.1%) and Puhuyesva believes interest rates will fall, the duration of assets should be greater than the duration of liabilities so that the surplus will rise if interest rates do fall. 为什么资产价值高于负债价值,duration就应该要greater than the duration of liabilities呢?

回答(1)

Simon2024-03-25 09:22:25

Simon2024-03-25 09:22:25

同学,上午好。

负债和资产的BPV不匹配,为了匹配确实是需要long 552份期货合约(计算过程: (299,860-243,376)/102.3=552)。

但是,问题里有这么一句话 given P‘s views on interest rates,所以我们还要考虑利率观点。

他认为未来利率会下跌,所以债券价格会涨,同样bond futures价格也会涨,所以会买更多的futures contract(这里观点和买卖股票一样,认为未来会涨,那就多买或少卖;如果认为未来会跌,那就多卖或少买),选B。考的是截图中的知识点(截图)。

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片