614****46392024-03-03 12:49:22

614****46392024-03-03 12:49:22

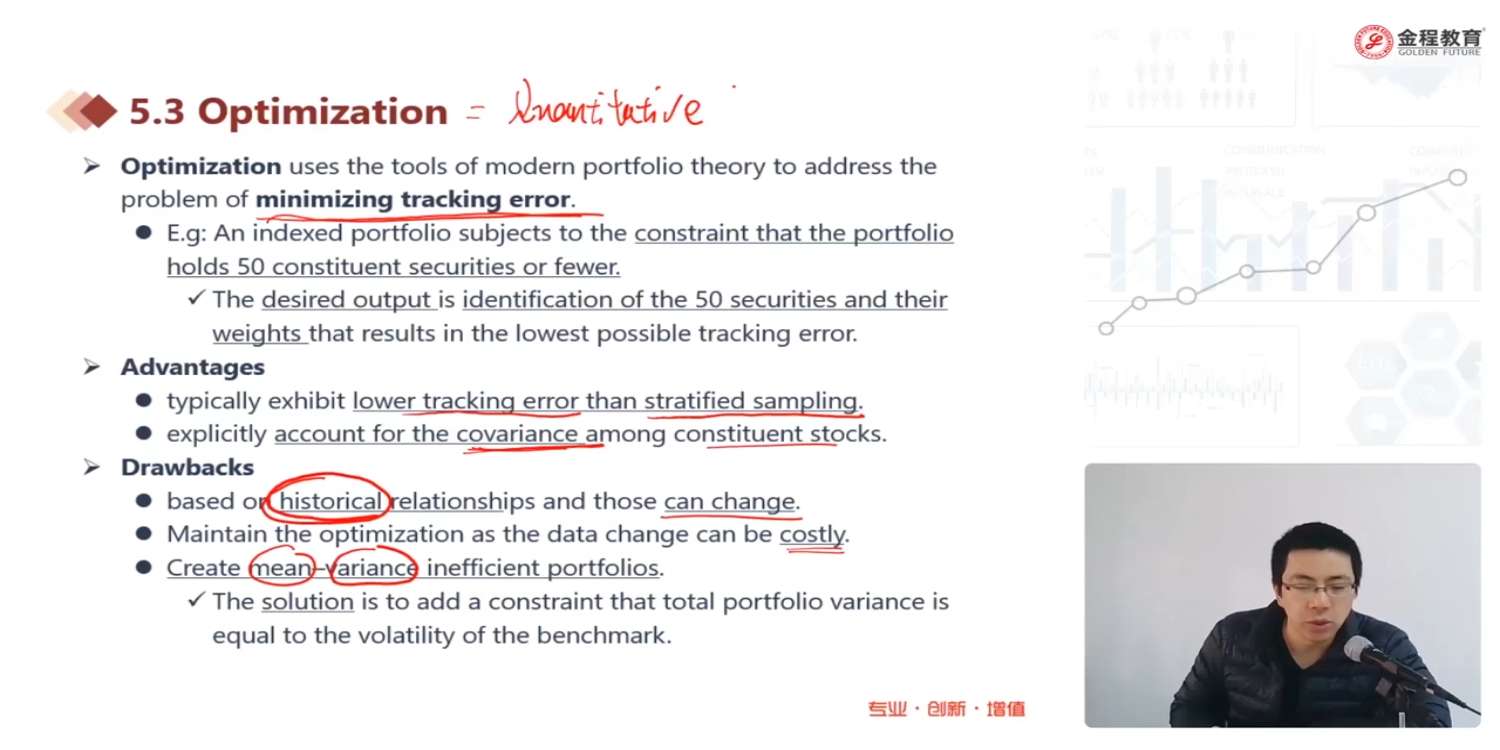

The solution is to add a constraint that total portfolio variance is equal to the volatility of the benchmark. 能不能解释一下这句话

回答(1)

Simon2024-03-04 13:08:38

Simon2024-03-04 13:08:38

同学,上午好。这是指,在构建组合时,加入限制,要求组合的σ=benchmark的σ。

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片