珊同学2022-05-11 20:20:58

珊同学2022-05-11 20:20:58

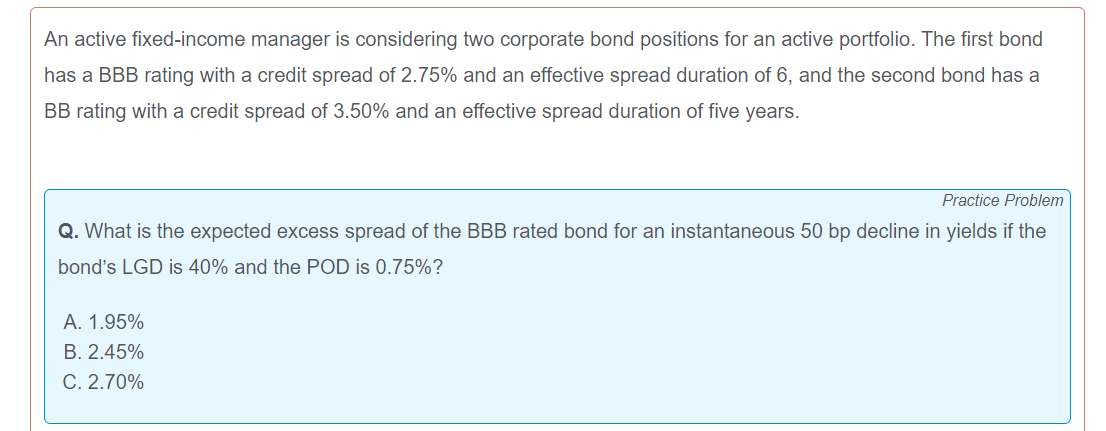

这道题2.75%- 6 × (-0.50%) − (0.75% × 40%)),为什么前面的2.75%没有?而且yield 降低0.5%,为什么答案中没有负号?给出的答案是 C is correct. The expected excess spread is equal to the change in spread multiplied by effective spread duration (–(EffSpreadDur × ΔSpread)) less the product of LGD and POD, which we can solve for to get 2.70% (=(–6 × 0.50%) − (0.75% × 40%)).

回答(1)

Nicholas2022-05-12 11:01:17

Nicholas2022-05-12 11:01:17

同学,早上好。

这里是计算Expected excess spread,那么要同时考虑期初Spread,Spread的变化以及预期违约损失。当发生瞬时变化,我们需要基于Spread0的基础上乘以0,也就是仅考虑后面两项。2.70% =(6 × 0.50%) – (0.75%× 40%)

利率下降导致债券价格上升,直接按照利率变动项为正处理即可。

努力的你请点击右下角的【点赞】哟~。加油,祝你顺利通过考试~

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片