伍同学2022-04-19 20:43:45

伍同学2022-04-19 20:43:45

老师,辛苦二道题,谢谢

回答(1)

开开2022-04-20 16:01:47

开开2022-04-20 16:01:47

同学你好,

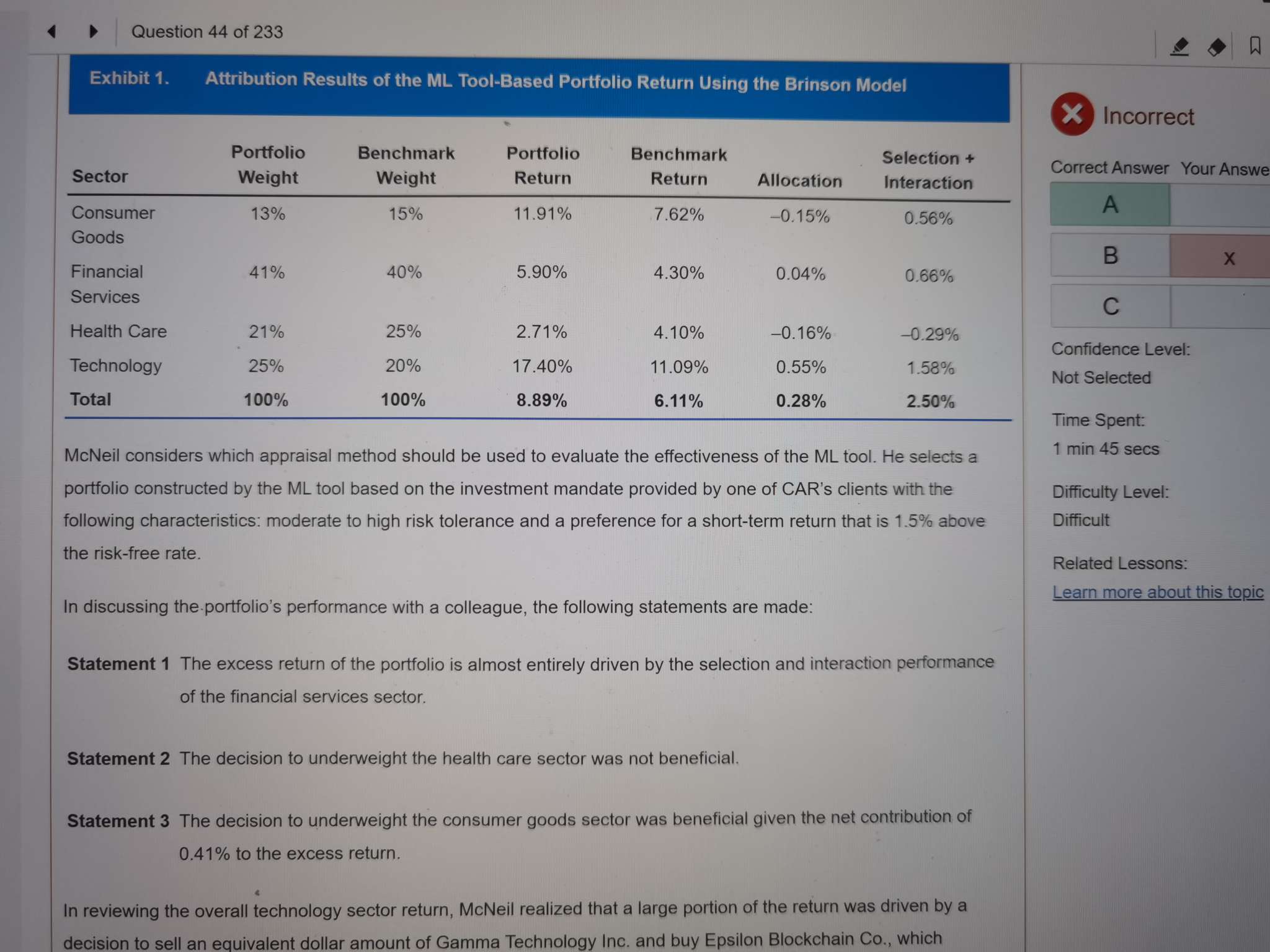

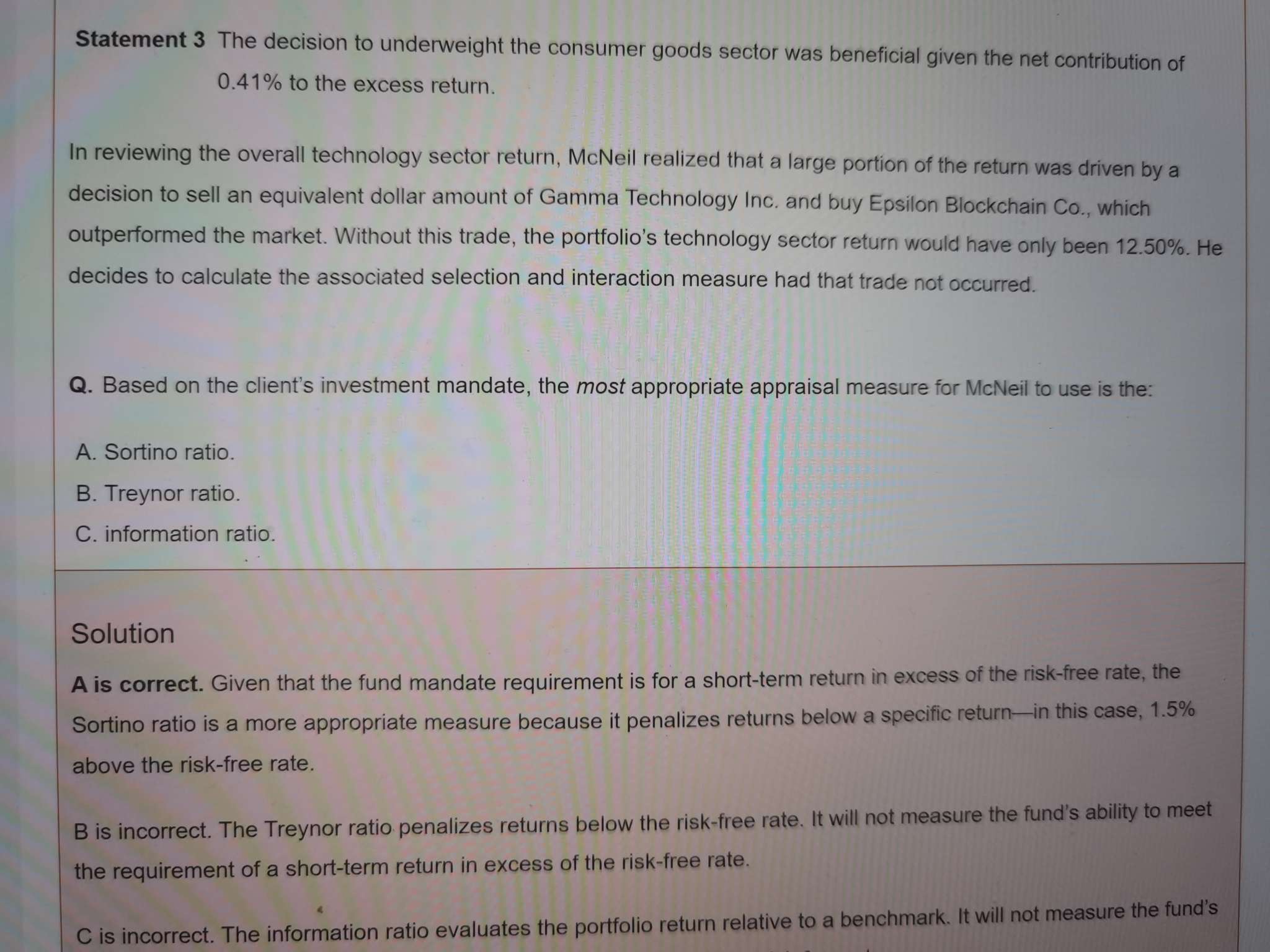

Q1: 这题根据客户的investment mandate,哪个appraisal measure最合适。

客户说他有 a preference for a short-term return that is 1.5% above the risk-free rate. 因此可以理解为rf+1.5%就是客户可以接受的最低收益率即MAR。而sortino ratio分子上的收益就是Rp-MAR,而分母上算的是低于MAR的半标准差,即该指标只惩罚低于MAR的收益的波动。因此,根据客户的要求,sortino ratio是最合适的。

- 评论(0)

- 追问(1)

- 追答

-

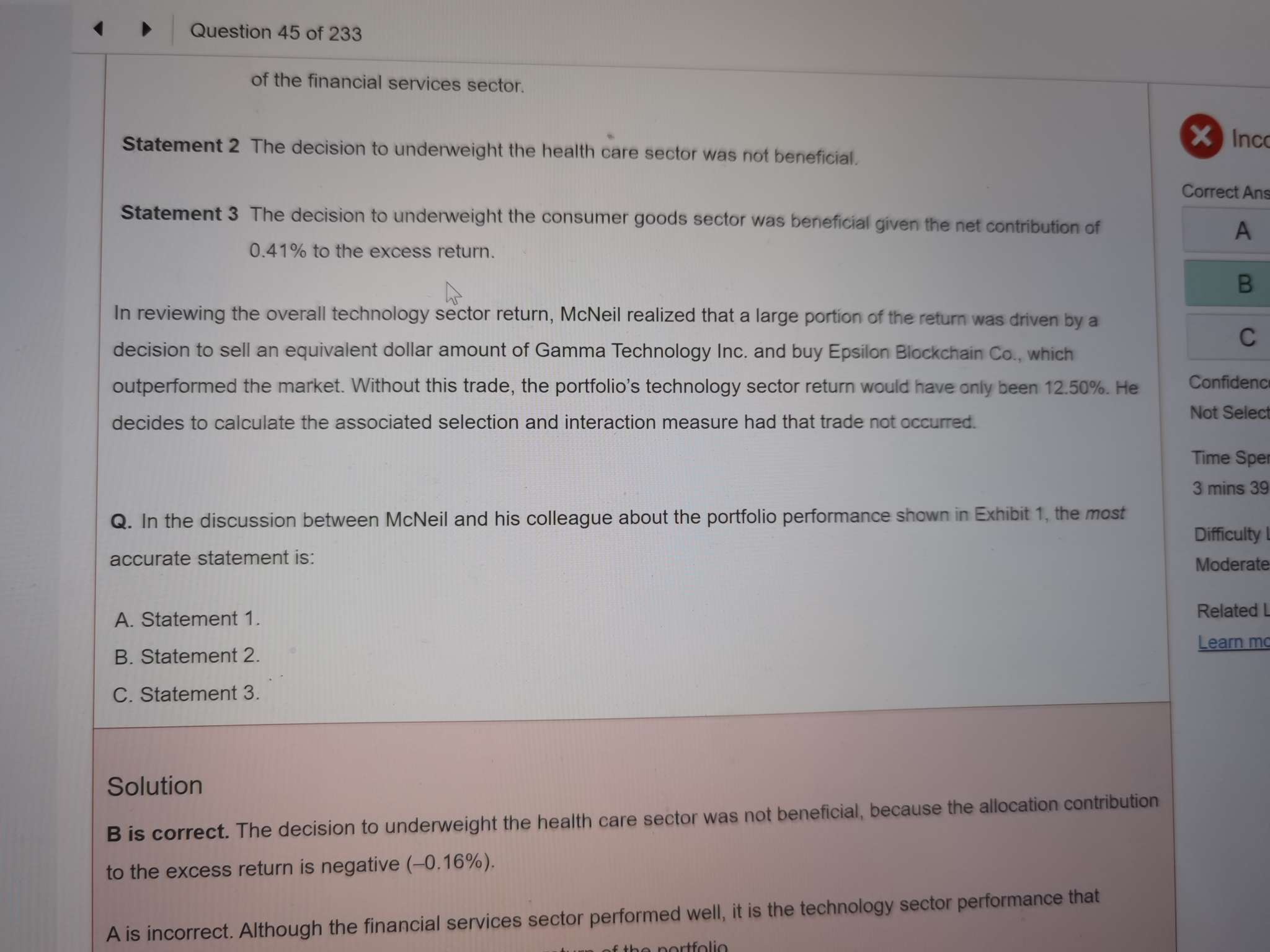

Q2: 这题问哪个statement是对的,这三个statement 都是和表一相关的。

第一个statement 说,组合的超额收益几乎全部是由 financial services sector的selection and interaction带来的。错,组合总的超额收益为8.89%-6.11%=2.78%,但financial services sector的selection and interaction只贡献率0.66%的超额收益,technology板块的selection and interaction带来1.58%的超额收益,因此这个表述是错的。

第二个statement 说,低配health care sector 的决策是没有好处的。低配板块的决策就是allocation effect,health care sector 的allocation effect是–0.16%,是负的贡献,因此这个表述是对的。

第三个statement 说,低配 consumer goods sector 的决策是有好处的,因为对超额收益的净贡献是0.41%。那么还是看 consumer goods sector的allocation,它的allocation是–0.15%,净贡献0.41%是算上了selection and interaction的,而这个statement说的是allocation的决策(贡献了负超额收益),因此说这个决策是有好处的是错的。

这题选B

【点赞】哟~。加油,祝你顺利通过考试~

评论

0/1000

追答

0/1000

+上传图片