秋同学2022-04-02 19:18:58

秋同学2022-04-02 19:18:58

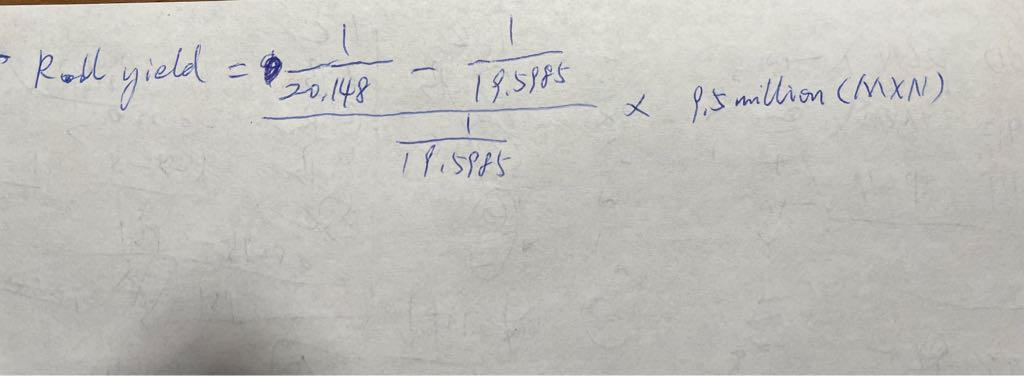

reading 10 example 5 请问下,第三题 具体计算的话,选用以下汇率和数据,老师看看对吗

回答(1)

Chris Lan2022-04-04 13:53:11

Chris Lan2022-04-04 13:53:11

同学你好

如果站在本币角度,那应该是F-S/S

应该是((1/20.148)-(1/20.058))/(1/20.058)

这里的S是你签订forward合约的时候的S而不是一个月之后的S。

在判断roll yield为正为负时,逻辑是这样的。

你要先看题目给的货币对是DC/FC还产FC/DC,进而决定你的对冲思路

如果是DC/FC,担心FC下跌,因此应该short DC/FC这个时候如果是升水,说明未来卖的更贵,roll yield是正的。

如果是FC/DC,担心DC上升,因此应该long FC/DC,这个时候如果是升水,说明未来买更贵了,roll yield是负的。

- 评论(0)

- 追问(2)

- 追问

-

同学你好

如果站在本币角度,那应该是F-S/S

应该是((1/20.148)-(1/20.058))/(1/20.058)

这里的S是你签订forward合约的时候的S而不是一个月之后的S。

老师你好,上面这句还是不太明白,签订了一个月后的远期合约,一个月后远期到期了,我要滚仓,不应该是用一个月后的现货来平仓吗,两个到期日一样才能offset吗,望解答,谢谢

- 追答

-

同学你好

在外汇管理中的roll yield的定义和二级另类中转仓是不太一样的。你看一下他的标准定义,就是我说的这样。

如果是DC/FC,将来卖的贵,roll yield就是正的。如果是FC/DC将来买的便宜,roll yield就是正的。

以下内容在原版书P178页。

The roll yield (also called the roll return) on a hedge results from the fact that forward contracts are priced at the spot rate adjusted for the number of forward points at that maturity (see the example shown in Exhibit 3). This forward point adjustment can either benefit or detract from portfolio returns (positive and negative roll yield, respectively) depending on whether the forward points are at a premium or discount, and what side of the market (buying or selling) the portfolio manager is on.

评论

0/1000

追答

0/1000

+上传图片