可同学2021-05-02 20:05:01

可同学2021-05-02 20:05:01

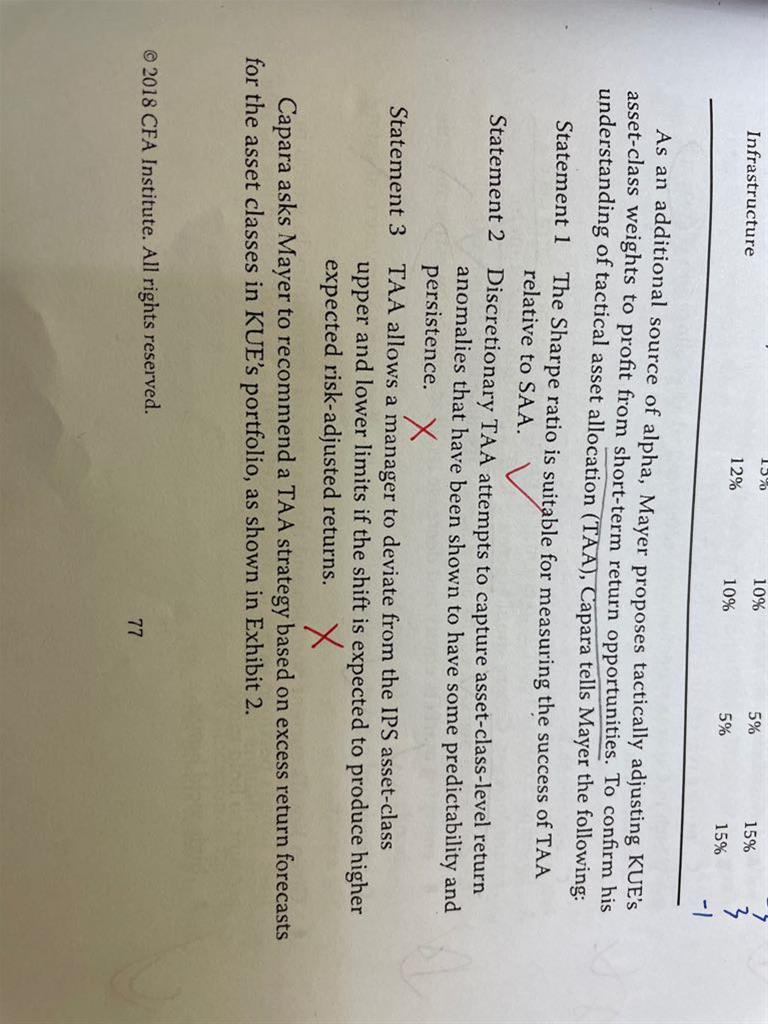

老师,statement 2和3为啥错?

回答(1)

Johnny2021-05-03 23:15:15

Johnny2021-05-03 23:15:15

同学你好。Statement 2如果把discretionary TAA改成systematic TAA的话那么statement 2就对了。以下两句话需要记住:

1.Discretionary TAA is predicated on the existence of manager skill in predicting and timing short-term market moves away from the expected outcome for each asset class that is embedded in the SAA policy portfolio

2.Systematic TAA attempts to capture asset class level return anomalies that have been shown to have some predictability and persistence.

Statement 3错是因为TAA是不可以超出upper and lower limits的。

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片