袁同学2021-03-06 20:31:56

袁同学2021-03-06 20:31:56

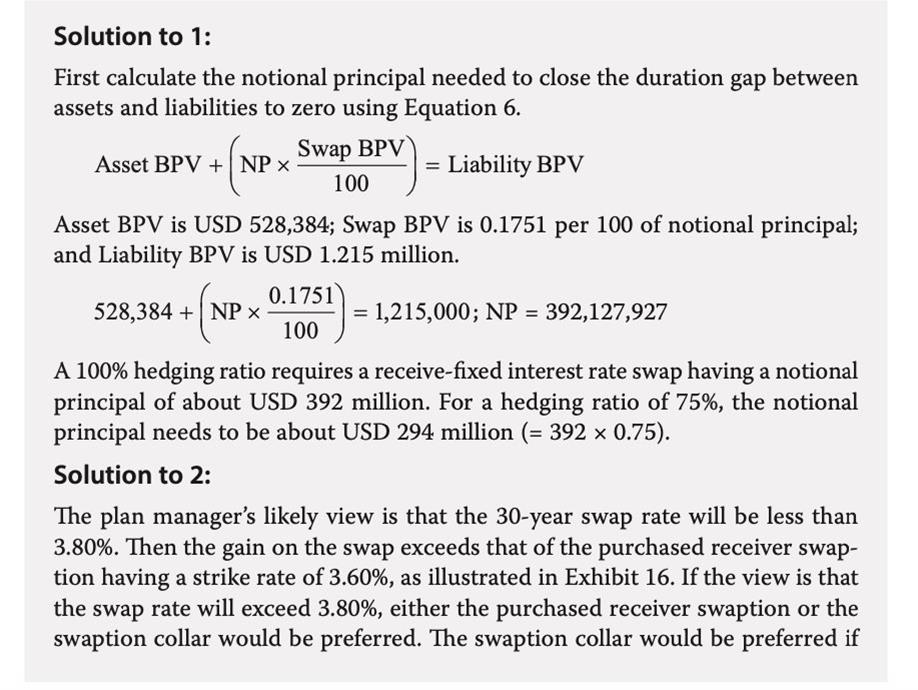

原版书课后题的85页的example 7的第二问,怎么理解?

回答(1)

Nicholas2021-03-08 11:57:10

Nicholas2021-03-08 11:57:10

同学,早上好。

这里有勘误,勘误如下,

“The plan manager’s likely view is that the 30-year swap rate will be less than 3.80%. Then the gains on the receive-fixed interest rate swap exceed those on the swaption collar (i.e., not profitable until the swap rate falls below 3.60%) and on the purchased receiver swaption (i.e., not profitable until the swap rate falls sufficiently below 3.60% to recover the premium paid) as illustrated in Exhibit 16. Note that if the 30-year swap rate exceeds 3.80%, then the receive-fixed interest rate swap will begin losing immediately. Losses on the swaption collar will not begin until the rate rises above 4.25%, while losses on the purchased receiver swaption (at any swap rate above 3.60%) are limited to the premium paid. Notice that this rate view is also consistent with the concern about lower corporate bond yields and the relatively high hedging ratio.

- 评论(0)

- 追问(1)

- 追答

-

这里担心利率下降导致负债端的价值升高,而让股票的收益抵消使得净负债仍然很大,因此需要考虑利率下降的问题。相较而言,利率上升的影响较小。

那么在这里,在观点是利率下降小于3.8%的前提下,purchased receiver小于3.6%才能行权,并且需要支付期权费;Swaption collar小于3.6%才能行权。那么有两个问题,第一个是3.6%到3.8%这段利率下降期没有保护,第二个是如果在利率下降小于3.8%的前提下3.80% receive-fixed swap是不用支付费用而获益最大的。

因此,这里需要把握两个前提,一个是利率下降,一个是利率下降小于3.8%来考虑这三个策略的优劣。

致正在努力的你,望能解答你的疑惑~

如此次答疑能更好地帮助你理解该知识点,烦请【点赞】。你的反馈是我们进步的动力,祝你顺利通过考试~

评论

0/1000

追答

0/1000

+上传图片