岳同学2020-11-05 17:36:38

岳同学2020-11-05 17:36:38

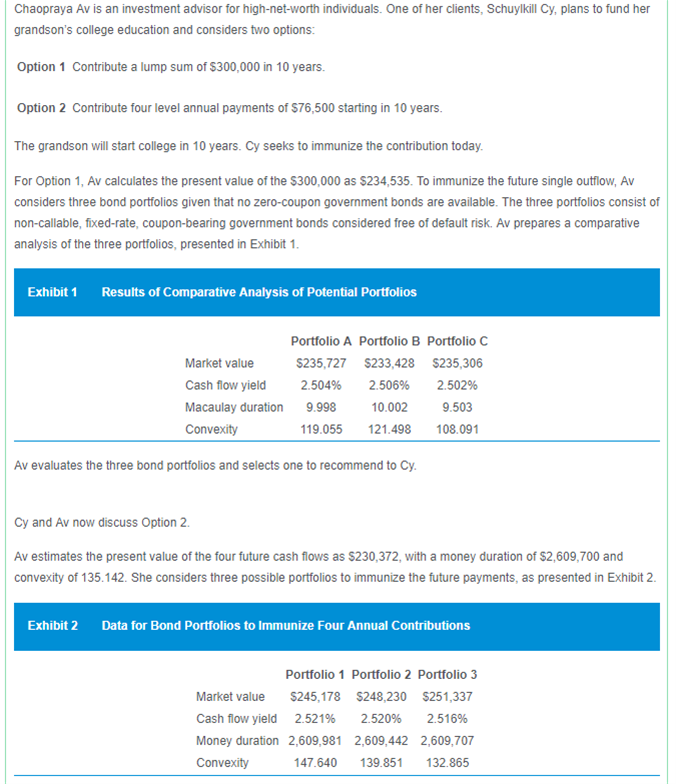

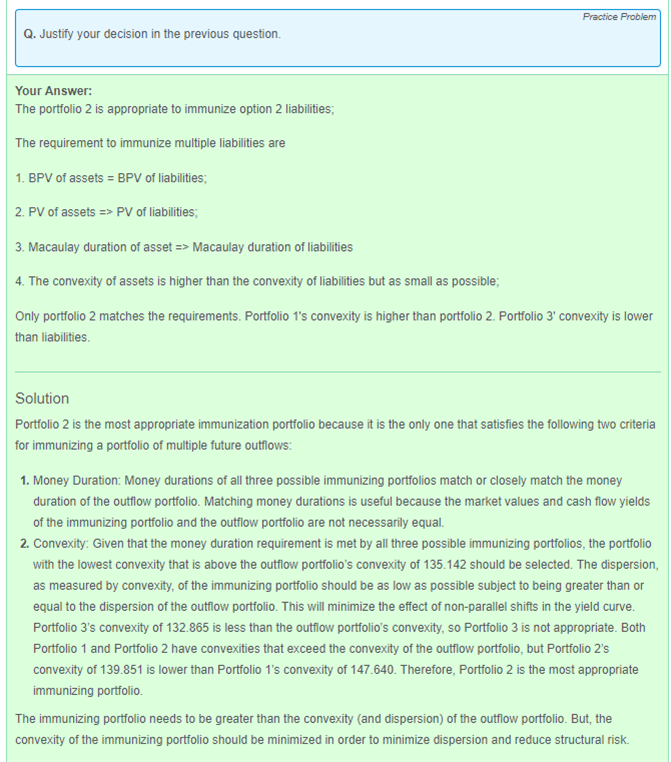

請問關於multiple liabilities immunization strategy,這樣寫有哪裡需要加強的嗎? he portfolio 2 is appropriate to immunize option 2 liabilities; The requirement to immunize multiple liabilities are 1. BPV of assets = BPV of liabilities; 2. PV of assets => PV of liabilities; 3. Macaulay duration of asset => Macaulay duration of liabilities 4. The convexity of assets is higher than the convexity of liabilities but as small as possible; Only portfolio 2 matches the requirements. Portfolio 1's convexity is higher than portfolio 2. Portfolio 3' convexity is lower than the liabilities.

回答(1)

Nicholas2020-11-09 09:17:27

Nicholas2020-11-09 09:17:27

同学,早上好。

以下仅代表个人建议:

1.如果写PV、Mac Dur、Convexity,就不用写BPV;

2.将等号换为Match可能更好,因为有时候组合久期并不相等或大于负债久期;

3.资产换为组合,PV of Portfolio match (or exceed) PV of liabilities,这里能最好加个匹配或超过;

4.个人建议4中的but可以改为and。

致正在努力的你,望能解答你的疑惑~

如此次答疑能更好地帮助你理解该知识点,烦请【点赞】。你的反馈是我们进步的动力,祝你顺利通过考试~

- 评论(0)

- 追问(3)

- 追问

-

那請問有必要寫出為什麼另外幾個portfolio不適合嗎?

- 追答

-

同学,早上好。

同学描述的最后一段的简单总结个人认为足够了,没有必要像答案中写的那么详细。

- 追答

-

同学,早上好。

同学描述的最后一段的简单总结个人认为足够了,没有必要像答案中写的那么详细。

评论

0/1000

追答

0/1000

+上传图片