刘同学2024-07-29 14:22:31

刘同学2024-07-29 14:22:31

I Spread 优点这两条怎么理解?

回答(1)

Evian, CFA2024-08-08 16:57:43

Evian, CFA2024-08-08 16:57:43

ヾ(◍°∇°◍)ノ゙你好同学,

提前总结一下:

1.Advantage的第一个黑点,因为I-spread是YTM和swap rate轧差,YTM代表固定利率融资成本,swap rate代表浮动利率融资成本,两个轧差就是个对比谁高谁低谁更划算。

2.第二个黑点,I-spread具有期限匹配的特点,于是对久期和持有收益率衡量起来都有帮助。

具体原版书内容理解:

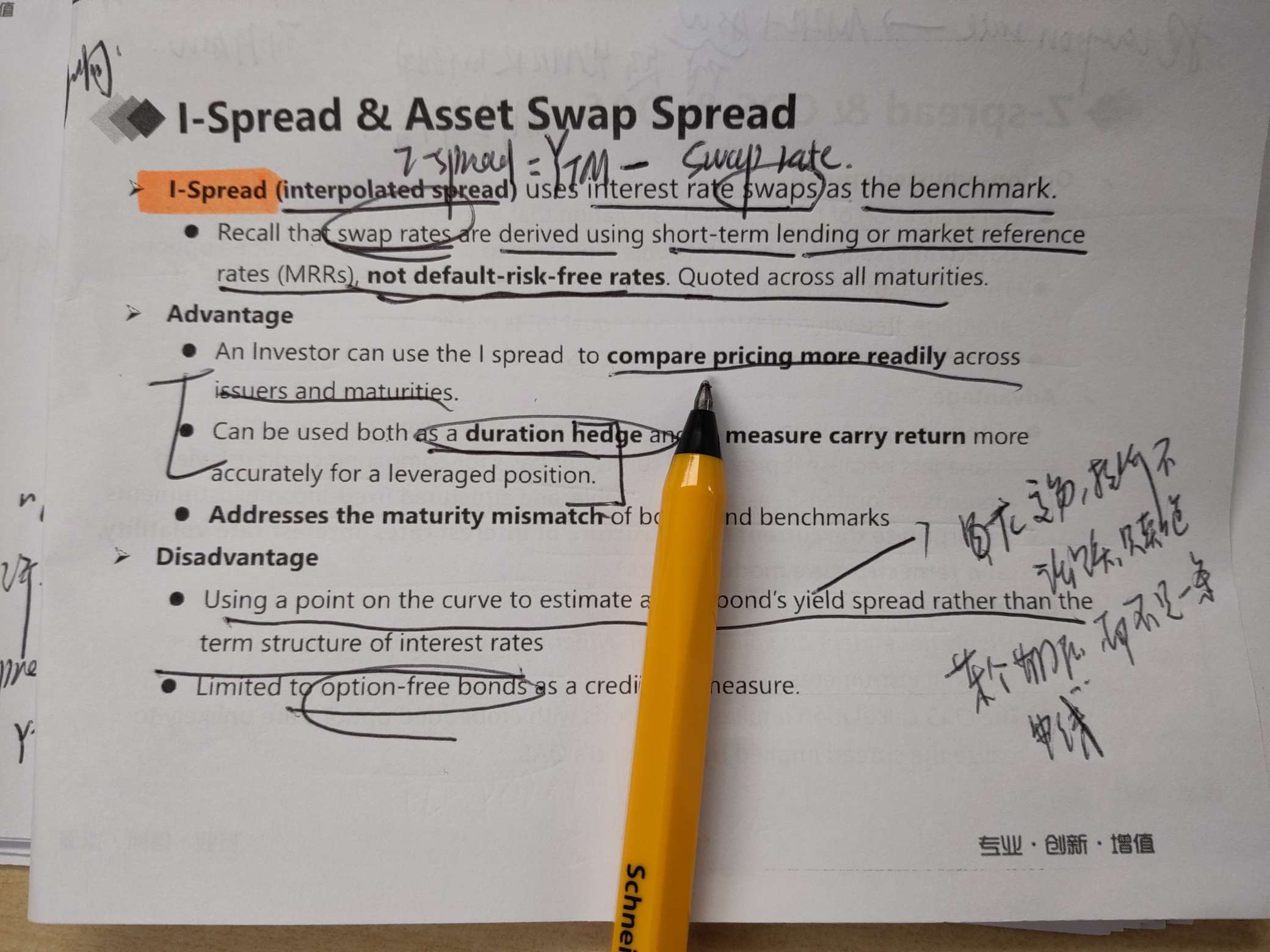

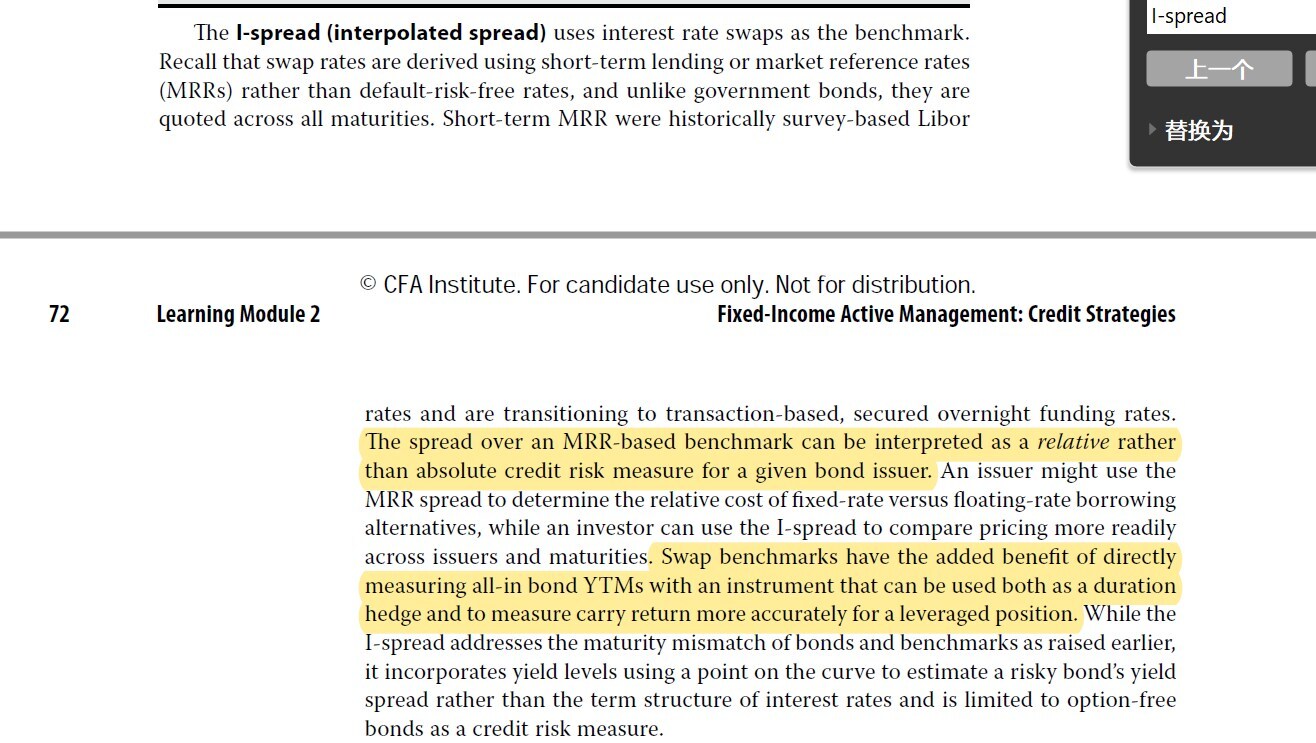

The I-spread (interpolated spread) uses interest rate swaps as the benchmark.

Recall that swap rates are derived using short-term lending or market reference rates (MRRs) rather than default-risk-free rates, and unlike government bonds, they are quoted across all maturities.

Short-term MRR were historically survey-based Libor rates and are transitioning to transaction-based, secured overnight funding rates.

I-spread 使用利率互换(interest rate swaps)作为基准。

回想一下,互换利率是使用短期贷款或市场参考利率(MRR)而不是无违约风险利率得出的,与政府债券不同(例如0-3年的3年期债券),互换合约对应的多个时间段的利率,所有到期日都有报价,例如0-1,0-2,0-3,0-4时间段。

短期MRR,它是基于调查的伦敦银行同业拆借利率Libor过度,然后到目前正在向基于交易的有担保隔夜融资利率。

- 评论(0)

- 追问(2)

- 追答

-

The spread over an MRR-based benchmark can be interpreted as a relative rather than absolute credit risk measure for a given bond issuer. An issuer might use the MRR spread to determine the relative cost of fixed-rate versus floating-rate borrowing alternatives, while an investor can use the I-spread to compare pricing more readily across issuers and maturities

I-spread=YTM-Swap rate,期限匹配

Swap rate是用MRR(设为一个基准)算出来的,用债券的YTM减去Swap rate(也是一个基准)

那么I-spread可以看成是基于MRR基准的利差,是相对而言的,和benchmark比较,不是自己和自己比较absolute credit risk measure,这个是站在bond issuer 发行人角度思考的

由于YTM对应的固定利率发行债券的成本,I-spread对应的是浮动利率发行债券的成本

所以发行人可以使用I-spread来确定固定利率与浮动利率借款相对而言哪个更划算

同样的逻辑,投资者考虑的收益,而不是发行成本,投资者可以使用I-spread更容易地去比较发行人它发行(不同到期时间)债券的定价

- 追答

-

Swap benchmarks have the added benefit of directly measuring all-in bond YTMs with an instrument that can be used both as a duration hedge and to measure carry return more accurately for a leveraged position. While the I-spread addresses the maturity mismatch of bonds and benchmarks as raised earlier, it incorporates yield levels using a point on the curve to estimate a risky bond’s yield spread rather than the term structure of interest rates and is limited to option-free bonds as a credit risk measure.

Swap benchmark还有额外的好处,是针对加杠杆的头寸,在久期对冲和持有收益方面,可以更加准确且直接衡量债券的YTM。

原因是久期涉及到了时间,持有收益也涉及到了时间。I-spread它是期限匹配的一个利差,YTM和Swap rate期限匹配,这种情况下更准确。这个是相对而言,相对的是利率的期限结构term structure,term structure是期限不匹配的,也就是在I-spread之前学过的yield spread,期限不匹配。

I-spread有个缺点,那就是在衡量信用风险时,仅限于衡量无内嵌期权的债券。

---------------------

投资更加优秀的自己👍 ~如果满意答疑可【采纳】,仍有疑问可【追问】,您的声音是我们前进的源动力,祝您生活与学习愉快!~

评论

0/1000

追答

0/1000

+上传图片