赵同学2024-08-07 14:06:10

赵同学2024-08-07 14:06:10

第四问解析中说“the more the time to expiration, the higher the value of both call options and put options holding all other parameters constant.”它的意思是T越大value越大,可是课上讲的不是T和value呈负相关吗?

查看试题回答(2)

Bingo2024-08-13 17:42:08

Bingo2024-08-13 17:42:08

同学你好,

你说的对

“the more the time to expiration, the higher the value of both call options and put options holding all other parameters constant.”它的意思是T越大value越大

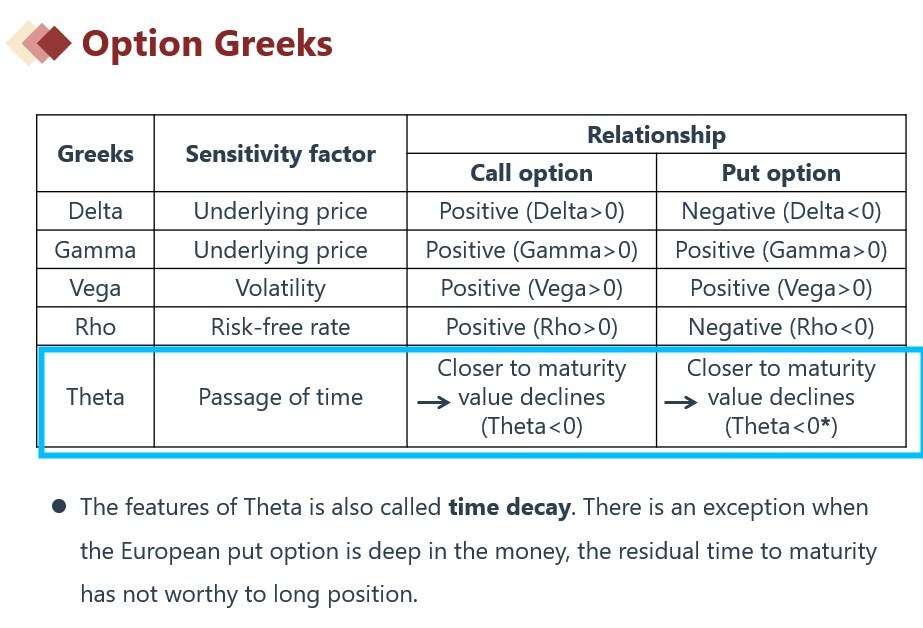

课上讲的是Theta,它是指时间流失对期权价值的影响

直白点理解theta就是Time value decay:long方不希望时间衰减,因为时间没了去哪里让S波动到深度价内ITM的状态;而short方希望时间衰减,因为到期了,short option这一方期权到手。

如果我们是买方(long方),期权它距离到期的时间越长,那么期权费越贵,因为标的资产价格波动至价内状态概率越大。

相反,期权到期的时间越短,那么期权费越便宜,因为标的资产价格波动至价内状态概率越小。

例如,T=3个月,option premium=5元,T=2个月,option premium变为3.5元

于是我们用Theta来衡量time value decay时间价值衰减,那这个5元衰减到3.5元,就是因为Theta,有5元-theta=3元这个关系式,于是theta=-1.5。

那么,对于long方而言,theta是个负值。

那么,对于short方而言,theta是个正值。这个也简单,因为衍生品是个零和游戏,long 和short方相反。

- 评论(0)

- 追问(5)

- 追问

-

所以Theta和call、put到底是正向还是负向关系? Theta不等于time to expiration?? time to expiration和time decay是一个意思吗?

- 追答

-

同学你好,

Passage of time 和期权是负相关

Theta是个指标,对于long Option,Theta为负

- 追答

-

The value of both call options and put options have a positive relationship with respect to theta

Theta和期权具有正相关性

the more the time to expiration, the higher the value of both call options and put options holding all other parameters constant.

解析的表述,T-t 越大, the more the time to expiration, 期权价值越大

- 追答

-

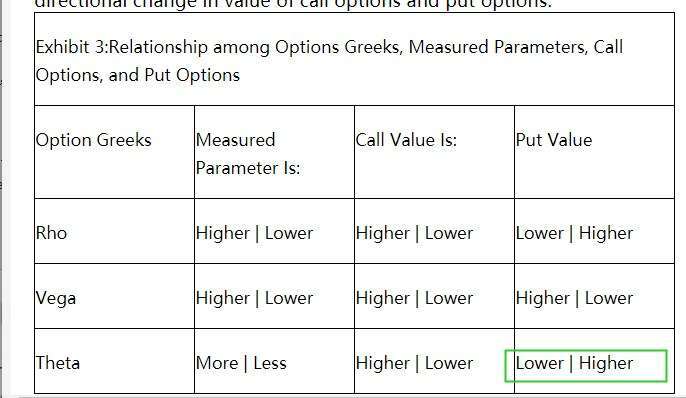

所以C选项正确的结果put value写反了

- 追答

-

绿色方框应该是 higher/lower

Evian, CFA2024-08-15 12:14:20

Evian, CFA2024-08-15 12:14:20

ヾ(◍°∇°◍)ノ゙你好同学,

Theta和call、put是正向是负向关系

Theta不等于time to expiration

time to expiration和time decay不是一个意思

time to expiration是“T-t”,是个时间段的概念

time decay是时间衰减,是在期权价值上蚕食的一个数值

上边的例子说明了蚕食期权价值的这个概念

用Theta来衡量time value decay时间价值衰减,那这个5元衰减到3.5元,就是因为Theta,有5元-theta=3元这个关系式,于是theta=-1.5

这个-1.5就是蚕食的数值

---------------------

投资更加优秀的自己👍 ~如果满意答疑可【采纳】,仍有疑问可【追问】,您的声音是我们前进的源动力,祝您生活与学习愉快!~

- 评论(0)

- 追问(2)

- 追问

-

所以theta与call、put都是负向关系吗?

- 追问

-

所以C选项正确的结果是什么?对于call和put来说哪个是higher哪个是lower?还是都是lower?

评论

0/1000

追答

0/1000

+上传图片