-

CFA一级

包含CFA一级传统在线课程、通关课程及试题相关提问答疑;

专场人数:6099提问数量:110221

你好,原版书后题第247页,15题,关于这里的疑问,我看了题目给的SPOT RATE,分别是三个债券的各自对应的SPOT RATE,为什么如15题,算债券X的定价,用2年期,3年期SPOT RATE,用对应Y和Z的呢,是不是题目没有给X两年期,三年期 就用另外Y,Z的SPOT RATE 呢

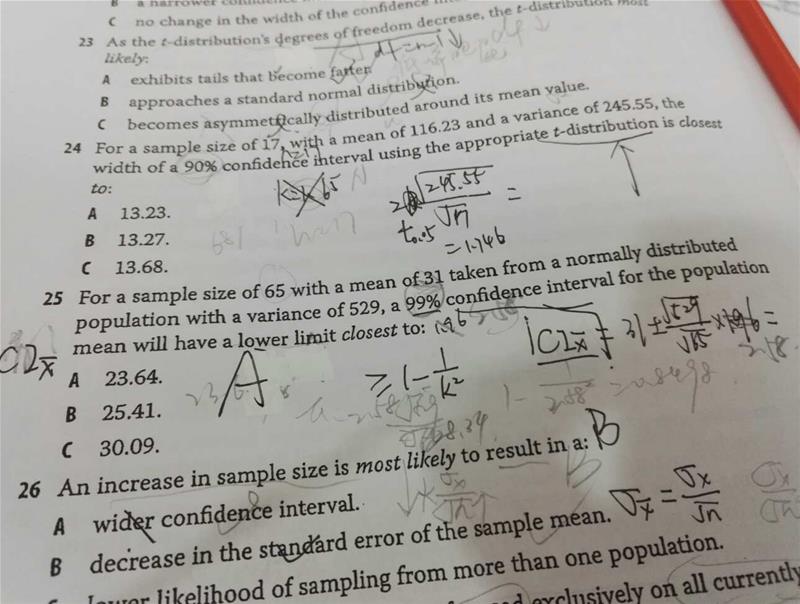

31. Ash Lawn Partners, a fund of hedge funds, has the following fee structure: • 2/20 underlying fund fees with incentive fees calculated independently • Ash Lawn fees are calculated net of all underlying fund fees • 1% management fee (based on year-end market value) • 10% incentive fee calculated net of management fee • The fund and all underlying funds have no hurdle rate or high-water mark fee conditions In the latest year, Ash Lawn’s fund value increased from $100 million to $133 million before deduction of management and incentive fees of the fund or underlying funds. Based on the information provided, the total fee earned by all funds in the aggregate is closest to: A. $11.85 million. B. $12.75 million. C. $12.87 million. 麻烦老师讲解一下这道题,重点帮忙区分一下2/20 underlying fund fees with incentive fees calculated independently,此题用independently来计算,如果是dependently这种如何计算?

已解决

精品问答

- Effective duration和Effective convexiy的公式为什么不用modified duration和convexity的原本公式,而是和他们的近似的久期和突性的公式一致?

- 为什么长期垄断竞争中 D和ATC相切

- 为什么TC 的切点对应是AVC的最低点?

- 为什么可以把TR TC同时体现在纵轴?

- 为什么B选项要考虑借股还股?而A选项没有考虑借钱买然后还钱?可以都不考虑吗?还是借股还股一定要在这个流程中体现?

- 老师好,官网这道题我有点没太懂,麻烦讲解

- 老师您好!这个需要掌握吗?谢谢

- 是不是只有在市场均衡点,才是社会总福利不损失的点? 偏离市场均衡点,社会总福利都会损失? 因为要么生产过剩,要么就是总供给不足. 另外,为什么只有在完全竞争市场中才能实现社会总福利最优,才能有市场均衡点? 在其他各类市场中,不是需求供给需求也是有的吗?他们的均衡点难道不是市场均衡点吗? 在那个点声场不是可以实现社会总福利最优吗? 这点不是很清楚,老师可以画图说明下. 另外, 对于一级价格歧视这种,它又是怎么实现社会总福利不损失的,这时候的需求曲线和供给曲线是什么样的?和完全竞争市场不同吗