150****43412022-10-04 22:24:13

150****43412022-10-04 22:24:13

老师,这道题如何理解?

回答(1)

最佳

Evian, CFA2022-10-04 22:53:26

Evian, CFA2022-10-04 22:53:26

ヾ(◍°∇°◍)ノ゙你好同学,

用一句话总结这个题目:

在标的资产价格S和执行价格X相同的条件下,具有相同标的资产、执行价格和到期时间的欧式看跌期权和欧式看涨期权的价值相同都为0

---------------------

学而时习之,不亦说乎👍【点赞】鼓励自己更加优秀,您的声音是我们前进的源动力,祝您生活与学习愉快!~

- 评论(1)

- 追问(3)

- 追问

-

嗯嗯,是的,请问为什么呢?

- 追答

-

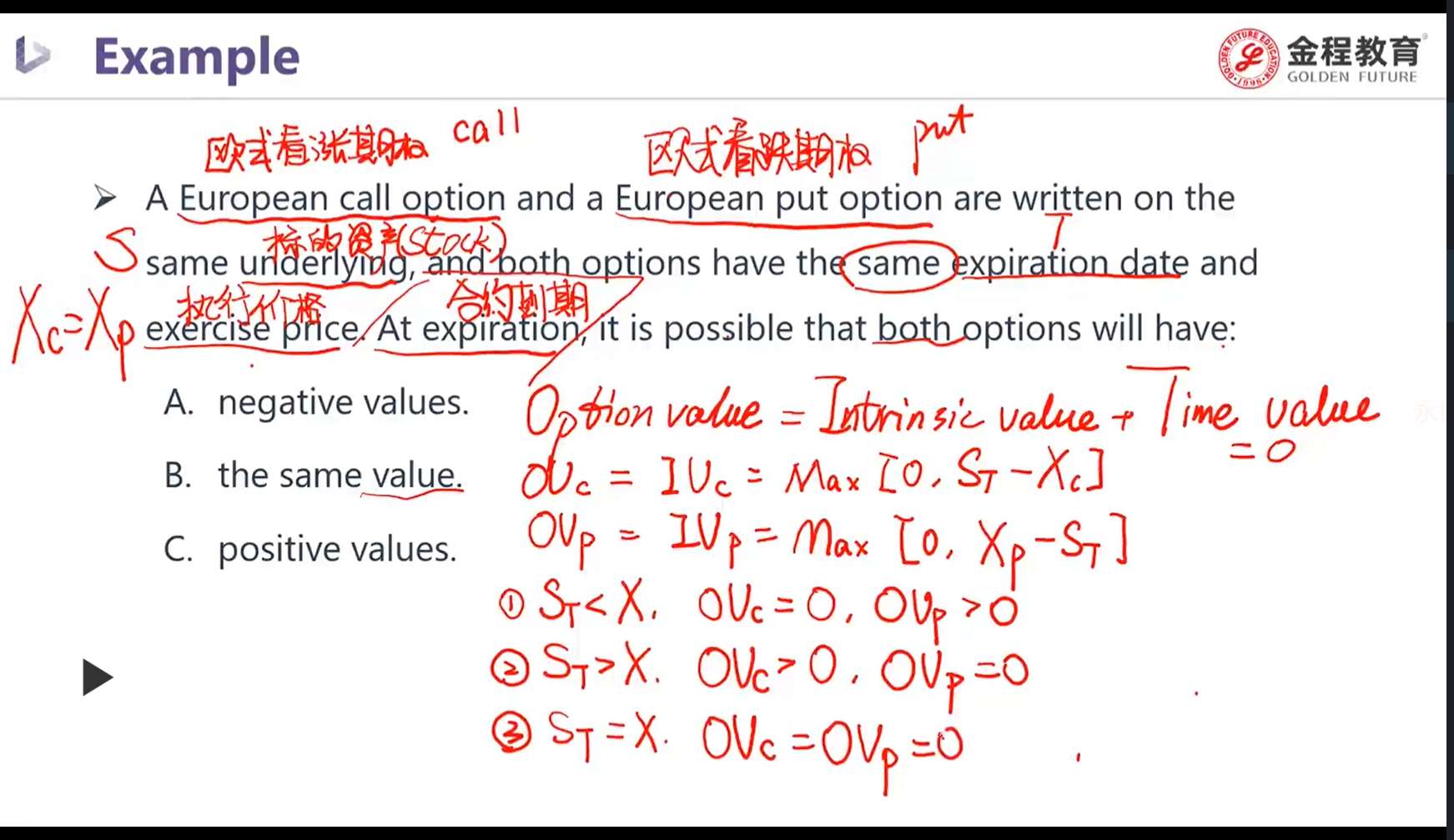

视频解析文字版:

期权到期,说明Time value=0

Option value (OV)=intrinsic value(TV) time value=intrinsic value (IV)

写出在T时刻,两个期权的内在价值:

call: OV=IV=Max[0, ST-X]

put: OV=IV=Max[0, X-ST]

假设ST>X,此时call的OV大于0,put的OV=0,两个value不相等

假设ST<X,此时call的OV=0,put的OV大于0,两个value不相等

假设ST=X,此时call的OV=0,put的OV=0,两个value相等

所以选B

- 追答

-

英文解析:

B是正确的。

If the underlying has a value equal to the exercise price at expiration, both options will have zero value since they both have the same exercise price.

如果到期时间点,标的资产价格与期权执行价格相等,那么这两种期权的合约价值都为零,因为它们都具有相同的行权价格。

For example, if the exercise price is $25 and at expiration the underlying price is $25, both the call option and the put option will have a value of zero.

例如,如果行权价格为25美元,到期时间点标的资产价格为25元,则看涨期权和看跌期权的价值都是为零。

The value of an option cannot fall below zero.

期权的价值不能低于零。

The holder of an option is not obligated to exercise the option; therefore, the options each have a minimum value of zero.

期权持有人没有义务行使期权(也就是期权价外时,理性投资者是不行权的);因此,两个期权的最小值都是零。

If the call has a positive value, the put, by definition, must have a zero value and vice versa. Both cannot have a positive value.

如果看涨期权的期权价值为正值,根据定义,看跌期权的价值为零。

如果看跌期权的期权价值为正值,根据定义,看涨期权的价值为零。

两者期权价值不能同时为正值。

评论

0/1000

追答

0/1000

+上传图片