139****17192022-08-17 14:17:48

139****17192022-08-17 14:17:48

When valuing a call option using the binomial model, an increase in the probability that the underlying will go up most likely implies that the current price of the call option: increases. remains unchanged. decreases.为什么这道题答案说option price和probability of underlying 没有关系呢?我们用二叉树对期权定价不就是要用股票价格来做出来二叉树吗?

回答(1)

最佳

Evian, CFA2022-08-18 10:01:01

Evian, CFA2022-08-18 10:01:01

ヾ(◍°∇°◍)ノ゙你好同学,

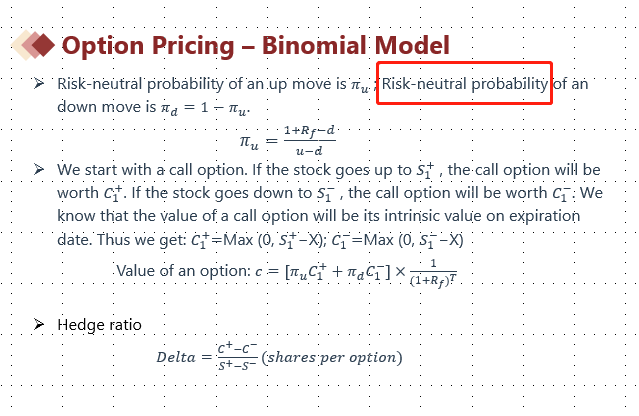

1.二叉树定价计算过程中,用到的概率是“风险中性概率”,不是股票真正上涨和下跌的概率

2.二叉树定价计算过程中,如你所说,先用股票价格算每一个时间节点的数值,然后求期权定价

----------------------

学而时习之,不亦说乎👍【点赞】鼓励自己更加优秀,您的声音是我们前进的源动力,祝您生活与学习愉快!~

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片