139****17192022-08-09 15:03:13

139****17192022-08-09 15:03:13

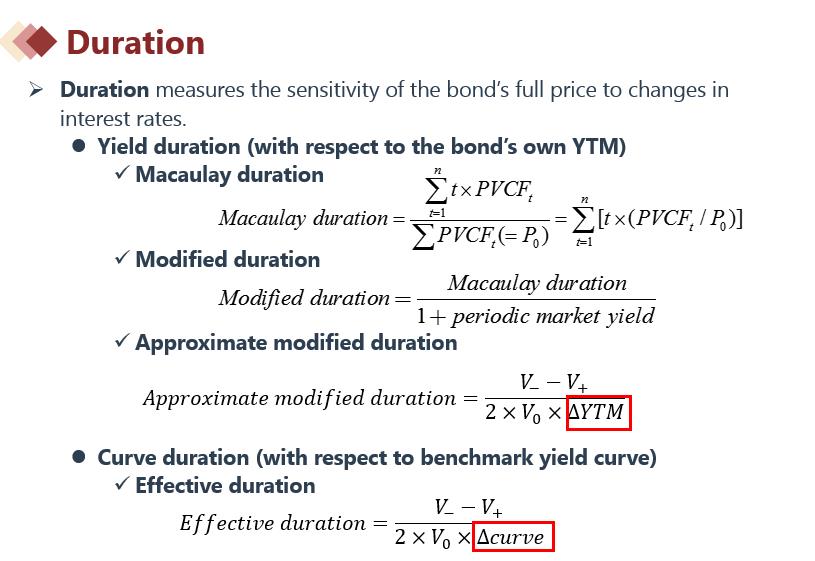

For an option-free bond, effective duration: a.will be equal to modified duration if the yield curve is absolutely flat. b.measures interest rate risk for both parallel and non-parallel benchmark yield curve shifts. c.is an estimate of the percentage change in bond price given a change in the bond’s yield to maturity. 老师好,能帮忙讲解一下这道题吗为什么只有当yield curve是平行于x轴的时候effective duration才等于modified duration呢?

回答(1)

最佳

Danyi2022-08-09 16:02:48

Danyi2022-08-09 16:02:48

同学你好,

effective duration和modified duration公式很相似,区别就在于收益率的变动率这里,因为YTM是一条水平线,那么curve也是水平的时候,此时两者是相同的。

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片