192****44722021-08-26 00:26:31

192****44722021-08-26 00:26:31

166题,Compared to an otherwise identical European put option, one that has a longer time to expiration may be worth less than the put that is nearer to expiration. 麻烦老师从英语阅读理解角度讲解下这个句子,尤其是请十分具体和详细地说一下它是拿一个什么东西和一个什么东西在作比较,谢谢!

回答(1)

Evian, CFA2021-08-26 19:59:32

Evian, CFA2021-08-26 19:59:32

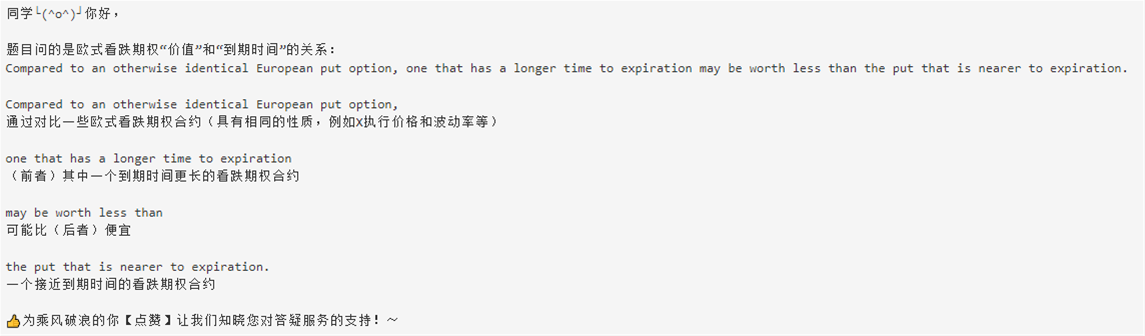

同学└(^o^)┘你好,

题目问的是欧式看跌期权“价值”和“到期时间”的关系:

Compared to an otherwise identical European put option, one that has a longer time to expiration may be worth less than the put that is nearer to expiration.

Compared to an otherwise identical European put option,

通过对比一些欧式看跌期权合约(具有相同的性质,例如X执行价格和波动率等)

one that has a longer time to expiration

(前者)其中一个到期时间更长的看跌期权合约

may be worth less than

可能比(后者)便宜

the put that is nearer to expiration.

一个接近到期时间的看跌期权合约

👍为乘风破浪的你【点赞】让我们知晓您对答疑服务的支持!~

- 评论(0)

- 追问(0)

评论

0/1000

追答

0/1000

+上传图片