紫同学2018-03-25 22:44:32

紫同学2018-03-25 22:44:32

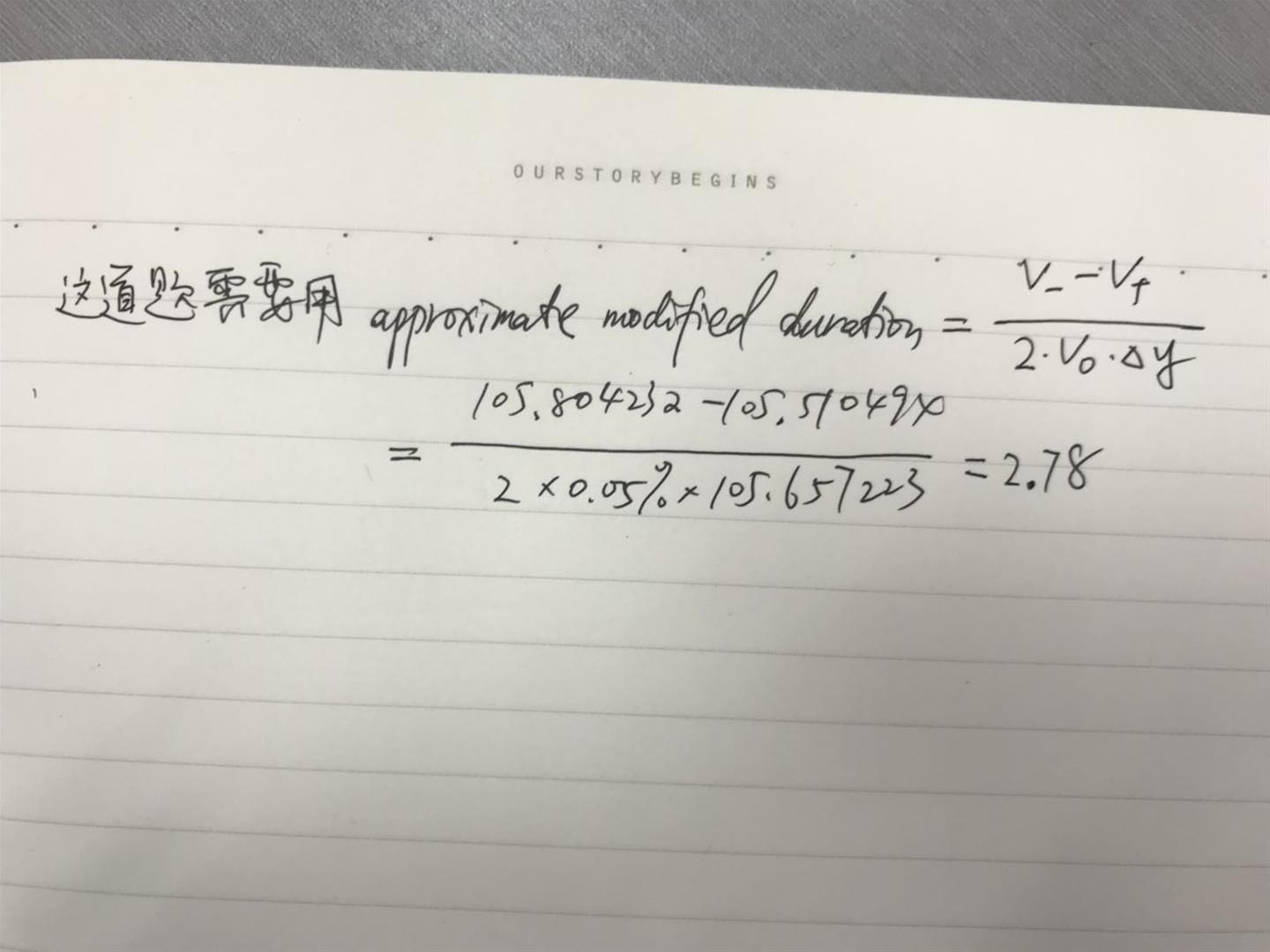

7. An investor buys a three-year bond with a 5% coupon rate paid annually. The bond, with a yield-to-maturity of 3%, is purchased at a price of 105.657223 per 100 of par value. Assuming a 5-basis point change in yield-to-maturity, the bond’s approximate modified duration is closest to: A. 2.78. B. 2.86. C. 5.56. 麻烦老师讲解一下。谢谢。

回答(1)

最佳

Vito Chen2018-03-26 09:28:00

Vito Chen2018-03-26 09:28:00

同学,你好。这道题目解答请看下图:

- 评论(0)

- 追问(4)

- 追问

-

陈老师,我就是V-和V+不懂算,麻烦再讲讲。谢啦。

- 追问

-

公式是知道用这个公式。

- 追答

-

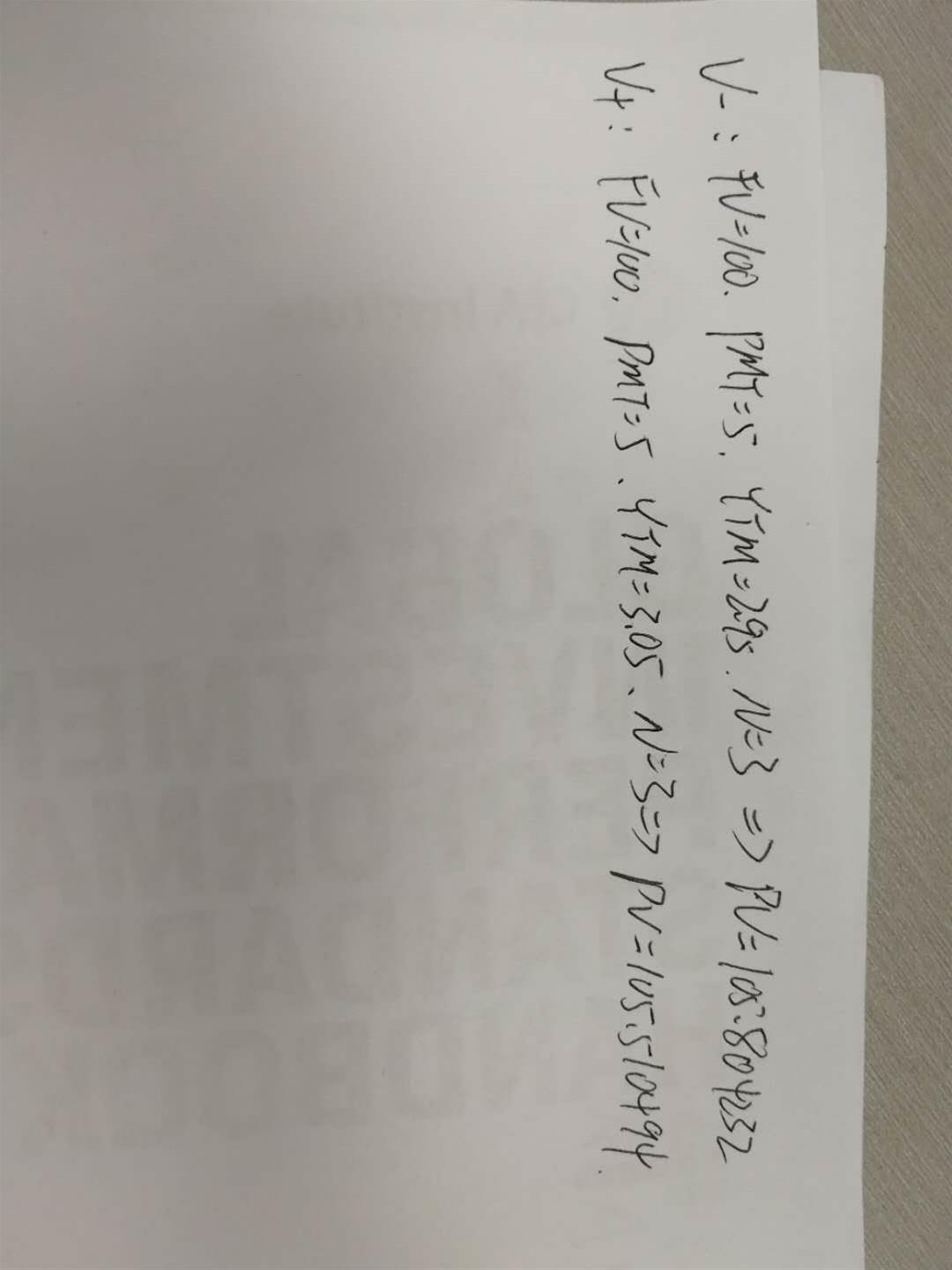

同学你好,V-是指利率下降时,债券价格上升后的值;同样V+是指利率上升时,债券价格下降后的值。计算方法如图

- 追问

-

哦,这下明白了,是要计算出每期PMT在利率上升后,下降后的折现现值之和。谢谢老师啦。

评论

0/1000

追答

0/1000

+上传图片