周同学2020-07-01 06:04:49

周同学2020-07-01 06:04:49

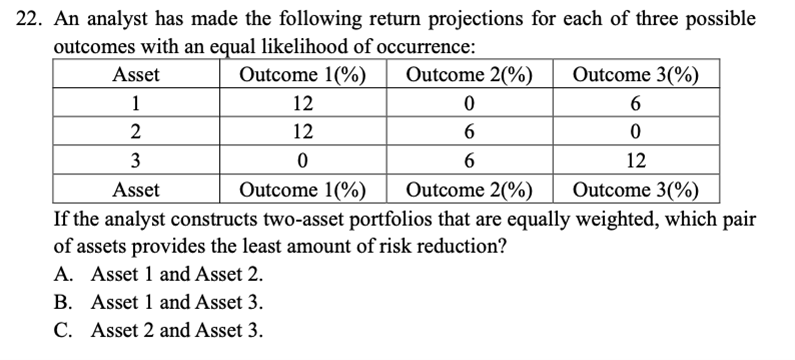

麻烦老师讲解一下具体计算过程

回答(1)

Irene2020-07-01 16:44:18

Irene2020-07-01 16:44:18

同学你好

这题不需要进行计算。本道case建议把三个资产的收益用图像进行表示。如下图

- 评论(0)

- 追问(3)

- 追答

-

本题问哪两个资产做组合的标准差最小。

本题选择C。资产收益率的相关系数越小,做出的组合的标准差越小。资产2和资产3收益率变动完全负相关。

- 追问

-

老师答案写的是A,说risk reduction 是risk 减少量的意思,所以least of risk reduction找的应该 correlation 接近1的一组吧? 看了老师这个图我大概懂了

22. Solution:A.

An equally weighted portfolio of Asset 1 and Asset 2 has the highest level of volatility of the three pairs. All three pairs have the same expected return; however, the portfolio of Asset 1 and Asset 2 provides the least amount of risk reduction.

- 追答

-

同学你好,嗯嗯是的。感谢你的指正。

评论

0/1000

追答

0/1000

+上传图片